Asian Central Banks Are in for a Quieter Year in 2019

For most of Asia’s central banks, things should be a whole lot less exciting next year, and that’s a good thing.

(Bloomberg) -- For most of Asia’s central banks, things should be a whole lot less exciting next year, and that’s a good thing.

As the U.S. Federal Reserve looks toward topping off its interest-rate hike cycle, even those policy makers in the region who haven’t followed the tightening path should be in position to keep policy steady, according to Deyi Tan, an Asia economist with Morgan Stanley.

“For most of the central banks in Asia, we don’t have very aggressive rate-hike cycles, except for maybe in the Philippines,” she said in an interview in Singapore. “We don’t actually think that central banks really need to keep in tandem with what the Fed does or doesn’t do. Outside of India or Indonesia, we actually have a very shallow rate-hike cycle or no rate hikes at all.”

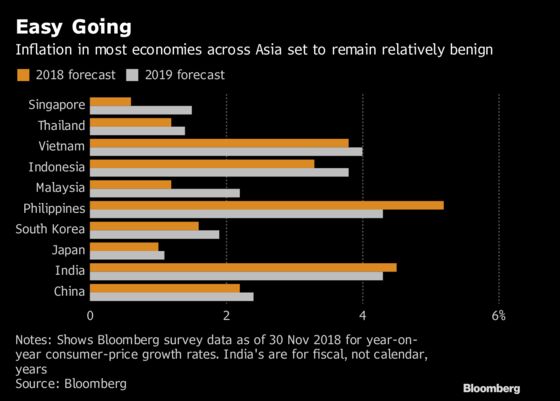

Morgan Stanley economists are penciling in a weaker dollar next year and U.S. 10-year yields declining to 2.75 percent -- providing less stress on emerging markets that had to worry this year about capital outflows and volatile currencies. Current accounts that are broadly in good shape and benign inflation risks for much of the region will keep Asian central bankers in a comfortable position, Tan said.

Here’s more from the interview with Tan:

Troubled Two

The Indian rupee and Indonesian rupiah bore the brunt of U.S. dollar strength in Asia in 2018, and in turn should be big beneficiaries as dollar strength moderates. India probably has a bit more tightening to do: Morgan Stanley sees one interest-rate increase in each of the second and third quarters. After 175 basis points’ worth of increases, Bank Indonesia’s tightening work should be done for now, they estimate.

“For most of the other central banks in Asia, most of them run current-account surpluses so they don’t have this funding squeeze whenever the U.S. dollar strengthens,” Tan said. “And macro fundamentals in Asia are generally quite controlled -- actually quite favorable.”

Discount Environment

Domestic inflation could complicate things, but in most parts of Asia inflation has surprised to the downside, Tan said. South Korea has only recently met its 2 percent inflation target, and the likes of Singapore, Taiwan, and Thailand show contained price growth.

Exception Economy

The exception to the steady-as-she-goes outlook in Asia: the Philippines.

Tan sees the problems as more domestic than external in the Philippines, suggesting an easing in external pressures won’t take its struggles away. She sees a significant buildup in debt and credit growth that’s running roughly twice the pace of GDP. Perhaps most importantly, inflation is still a huge problem.

“Even with oil prices falling, the peso appreciating, the reality is that’s not going to resolve all the inflationary pressures that the Philippines is facing,” she said.

A boost to inflation this year from tax changes will fade in early 2019, and legislation around the rice supply should help damp price growth. But Tan sees policy makers at Bangko Sentral ng Pilipinas underestimating the durability of faster inflation, particularly as core CPI also has been rising.

Morgan Stanley sees another two increases of 25 basis points each in the first and second quarters.

Elsewhere in the Toolbox

One X-factor for Asia’s central banks in 2019: They might find more use in macro-prudential tightening that’s more targeted to their specific needs, said Tan.

“For Asia, maybe macro-prudential tightening is the better way to go about dealing with financial stability risks if policy makers still feel like these risks exist -- more so than interest rates,” which are a blunt tool, she said.

South Korea, Singapore and Thailand each have shown success in using a more “pointed” macro-prudential approach to perceived financial instabilities, in Tan’s view.

To contact the reporter on this story: Michelle Jamrisko in Singapore at mjamrisko@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Henry Hoenig

©2018 Bloomberg L.P.