U.S. Stocks End a Volatile Day Where They Started: Markets Wrap

All you need to know about what’s moving markets today.

(Bloomberg) -- U.S. stocks ended little changed after a volatile session as investors weighed the prospects for a trade deal and an agreement to fund the American government.

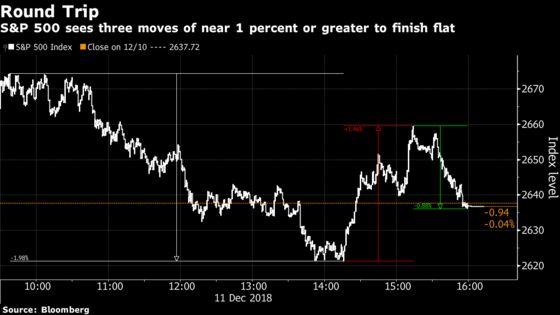

The S&P 500 Index started out strong, took a turn down, then recovered from the day’s lows as key Senate leaders signaled a desire to avoid a government shutdown hours after Donald Trump threatened to do so in a spat over funding for his border wall. Carmakers rose as China signaled it may cut tariffs on auto imports, but investors were cautious about a broader deal. The dollar climbed.

U.S. markets have been whipsawed in recent weeks as traders searched Trump’s tweets for clues about the outlook for trade talks, tried to decide if a stock selloff could prompt the Federal Reserve to pare back rate increases and evaluated economic data that signaled a slowdown may be coming. Monday’s session saw the S&P 500 Index’s biggest full reversal since Feb. 6 as it erased a 1.9 percent decline and ended 0.2 percent higher, while Tuesday saw gains as big as 1.4 percent and losses as deep as 0.6 percent.

“It went from headline excitement to cold reality challenges,” said Mike Bailey, the director of research at FBB Capital Partners. “You’ve got a pretty skeptical market out there.”

The news on car tariffs followed reports that Chinese Vice Premier Liu He discussed a timetable for trade talks with Treasury Secretary Steven Mnuchin. Yet investors also have an eye on the continuing flap over Canada’s arrest of the chief financial officer of Huawei Technologies Co., and the Washington Post reported that the Trump administration is preparing a series of actions this week to condemn China for efforts to steal U.S. technology. And among a plethora of political risks, the U.K. is struggling to put its Brexit deal back on track and fears linger over the possibility a French protest movement could escalate further.

Elsewhere, the Stoxx Europe 600 Index climbed the most in six weeks. India’s assets saw a choppy session, with stocks initially roiled by a surprise resignation of the central bank governor Monday, before posting a recovery. Emerging-market shares edged higher.

Terminal subscribers can read our Markets Live blog.

Here are some key events on the calendar this week:

- The European Central Bank is set to cap asset purchases at its final policy meeting of 2018 on Thursday.

- China industrial production, retail sales data for November is due Friday.

And these are the main moves in markets:

Stocks

- The S&P 500 was little changed at the close of trading in New York.

- The Stoxx Europe 600 Index rose 1.5 percent.

- The MSCI All-Country World Index added 0.1 percent

- The MSCI Emerging Market Index rose 0.2 percent.

- The Nikkei-225 Stock Average slipped 0.3 percent.

Currencies

- The Bloomberg Dollar Spot Index gained 0.1 percent.

- The euro fell 0.3 percent to $1.1323.

- The Japanese yen was little changed at 113.38 per dollar.

- The British pound fell 0.6 percent to $1.2491.

Bonds

- The yield on 10-year Treasuries rose two basis points to 2.87 percent.

- Germany’s 10-year yield fell one basis point to 0.23 percent.

- Britain’s 10-year yield fell one basis point to 1.18 percent.

Commodities

- The Bloomberg Commodity Index fell 0.1 percent.

- West Texas Intermediate crude rose 1.4 percent to $51.70 a barrel.

- Gold slipped 0.1 percent to $1,243.12 an ounce.

--With assistance from Andreea Papuc, Christopher Anstey, Todd White, Lu Wang and Eddie van der Walt.

To contact the reporters on this story: Brendan Walsh in Austin at bwalsh8@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh

©2018 Bloomberg L.P.