Argentina's Policy Shift Pays Dividends as Peso Stabilizes

Argentina’s central bank is taking no prisoners in its fight to save the peso -- and the policy is working.

(Bloomberg) -- Argentina’s central bank is taking no prisoners in its fight to save the peso -- and the policy is working.

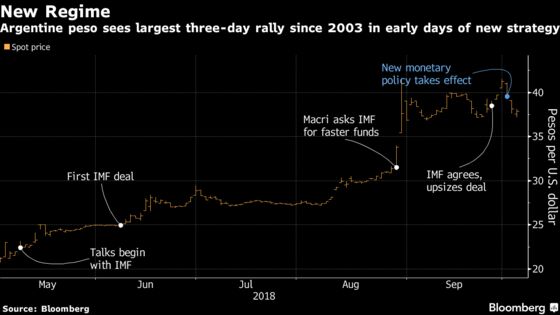

The bank is draining almost every peso it can find from the financial system in a new approach that has triggered the biggest three-day rally in the currency in 15 years. The peso trimmed some of the gains Thursday as U.S. Treasuries sink, curbing demand for emerging market assets. Still, the currency has gained 7 percent this week, after losing as much as 55 percent this year.

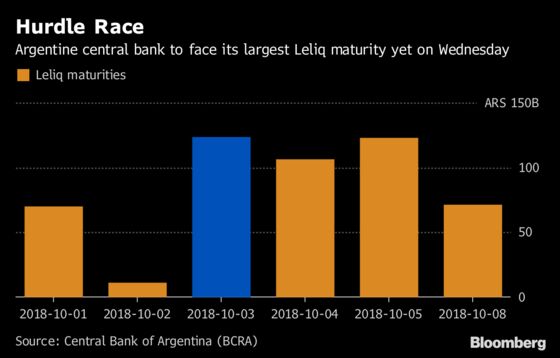

As of Oct. 1, the central bank ditched its inflation target and focused instead on stalling the growth in the money supply. It’s a kind of quantitative easing in reverse. The bank sold $6.2 billion of one-week peso notes, known as Leliqs, so far this week at an interest rate as high as 71.3 percent.

"With close to zero peso liquidity onshore, there’s not much left to convert into dollars,” said Delphine Arrighi, a money manager at Old Mutual Global Investors in London, who’s overweight on the nation’s local and hard-currency bonds. “Some portfolio inflows have helped as well in the last few days as the carry trade is now becoming compelling again."

New central bank Chairman Guido Sandleris, a former deputy at the Economy Ministry, is dedicated to keeping interest rates at a minimum of 60 percent, the highest in the world, as he attempts to slow inflation from 34 percent in August. Under his leadership, the bank has also hiked reserve requirements for banks, which limits their holdings in foreign currency. The policy is designed to keep the peso within a band from 34 to 44 pesos per dollar. The band adjusts 3 percent monthly. The peso traded at 38.4 per dollar, near the midpoint of the band, at 11:21 a.m. in Buenos Aires.

The new approach to monetary policy is part of a revised agreement with the International Monetary Fund that boosted its credit line to $57 billion. The central bank had been criticized by IMF Managing Director Christine Lagarde for not being sufficiently transparent with the market.

Policy makers will have to steel their resolve as increasing numbers of Leliqs mature. Inflation will reach 44.8 percent this year, according to the central bank’s monthly survey of economists published Oct. 2, up from the 40.3 percent forecast in August, and more than double the 19 percent predicted at the beginning of the year.

"The central bank is going to have to keep rates high for the foreseeable future," said Edwin Gutierrez, the head of emerging-market sovereign debt at Aberdeen Asset Management in London. "They cannot lower the rates until the rollover risk dissipates."

Some analysts have even started speculating whether the peso will strengthen too much. If the exchange rate moves to the lower limit of the band, the central bank will have the option of buying dollars.

"The debate has shifted to when the peso breaks the floor as opposed to the ceiling of the trading band," said Siobhan Morden, head of Latin American fixed income strategy at Nomura in New York, who recommends Argentina’s sovereign notes due in 2021. "Based on the past few days, that could happen sooner rather than later."

Here’s what other investors and analysts are saying:

Kathryn Rooney Vera, head of global research at Bulltick Capital Markets in Miami, who recommends peso-denominated bonds, the 2028 dollar bonds and Argentine stocks.

- "The peso was massively and clearly oversold at the low 40s," Rooney Vera said. "We’ve always said when risk appetite turns in favor of EM, high-beta Argentina will disproportionately outperform."

Alejandro Cuadrado, global head of foreign exchange at BBVA, who sees the peso ending the year at 42 per dollar, the midpoint of the currency band.

- Performance so far "is a positive indication."

- "It’s just been three days of the new policy and two without institutional help to the FX, so the ARS is still on crutches and sensitive to volatility. There’s indications of local portfolio returns to peso instruments. Offshore investors are more timid, it will be hard for them to return in full force."

Daniel Artana, chief economist at the Latin American Economic Research Institute

- "The new agreement with the IMF has an impact, it clears away sovereign risk until the end of 2019."

- "The demand for dollars for tourism is falling very sharply."

--With assistance from Ignacio Olivera Doll.

To contact the reporters on this story: Carolina Millan in Buenos Aires at cmillanronch@bloomberg.net;Ben Bartenstein in New York at bbartenstei3@bloomberg.net;Patrick Gillespie in Buenos Aires at pgillespie29@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, ;Vivianne Rodrigues at vrodrigues3@bloomberg.net, Philip Sanders

©2018 Bloomberg L.P.