As Creditors Blast Argentina’s Offer, Bond Prices Start to Rise

Bondholders Pan Argentina Restructuring Offer, Gird for Battle

(Bloomberg) -- A three-year payment moratorium, a huge cut in interest rates and an across-the-board extension in maturities. The bond restructuring proposal that Argentina unveiled late last week was harsh by any standards.

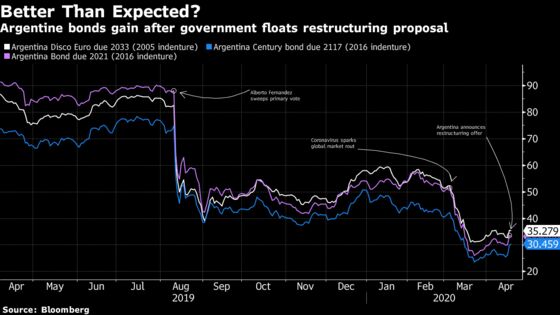

And yet, in a sign of just how low expectations were ahead of the announcement, investors are now actually bidding up prices on the country’s $66 billion of foreign bonds in the secondary market. Securities due in six years were trading around 33 cents on the dollar early Monday morning, up from 30 cents on Friday and 26 cents the day before.

The rally signals that for all the criticism that creditor groups have hurled at the offer, many investors were steeling for something a lot worse from a country that has earned a reputation as a serial defaulter with a hard-nosed negotiating style. And it suggests that the government, with just a few additional concessions, might have a decent chance at getting creditors to accept the deal.

“The upcoming negotiations carry a material probability of success,” Alberto Bernal, the chief strategist for XP Investments in Miami, wrote in a research note. “The options available to increase the terms of the offer are ample, and we believe that they are immaterial from the standpoint of ensuring the future sustainability of Argentina’s debt load.”

Bernal estimates the current offer would inflict a 60% loss in net present value terms for bondholders, and that the discount will need to be lowered to less than 50% for the proposal to win sufficient support.

Argentina’s plan calls for more than $40 billion in debt relief -- a $3.6 billion reduction in principal and $37.9 billion cut in interest payments. Current bondholders would get new securities with interest rates that start at zero and gradually increase, creating an average rate of 2.33% -- well below what’s typical for emerging-market debt.

Three groups of bondholders rejected the initial proposal, but didn’t give specifics of where the offer fell short or what they’d like to see instead.

The Argentina Creditor Committee -- made up of mutual funds, family offices, insurance firms and asset managers holding Argentine debt -- said in a statement that the offer has “fallen well short of bondholders’ expectations.” Members also cited a lack of clarity about changes to economic policy that would ensure creditors eventually get paid back.

A group holding $4 billion of bonds issued in 2005 and 2010 called the proposal “unilateral” and “unacceptable” as it doesn’t “represent the product of good faith negotiations.”

A third group of “ad hoc” creditors, including heavyweights such as BlackRock and Fidelity, said in a statement that the current offer puts a “disproportionate share” of the nation’s adjustment efforts on the shoulders of international bondholders.

The criticism from bondholders isn’t exactly surprising, of course, as they position themselves for negotiations. Economy Minister Martin Guzman, who took office in December with left-wing President Alberto Fernandez, also took a defiant stance in an interview with a local journalist published Sunday, insisting the nation needs massive debt relief to ensure social stability.

Argentina is in a difficult spot just a few years after creditors rushed to lend to the country amid a promise of rebirth in South America’s second-largest economy. Instead, the peso has lost more than half its value, inflation is running above 50% and gross domestic product is forecast to shrink for the third straight year in 2020.

In a filing with the U.S. Securities and Exchange Commission, Argentina warned that if the debt exchange doesn’t happen it “faces a significant risk of default.”

Roger Horn, a senior strategist at SMBC Nikko Securities America in New York, said Argentina will have to offer better terms on interest payments to win broad investor support.

“The government thinks it’s nice that the deal they’re offering doesn’t have a harsh haircut, but investors don’t buy a bond just because it has a high number on a piece of paper,” Horn said. “They buy bonds because they want a return.”

As part of the plan, no principal will be paid back before 2026, and just one-eighth of the bonds’ principal is due before 2030. That means the vast majority of the money won’t be repaid until the following decade, after Fernandez has left office.

Estimates on the losses being imposed by Argentina varied widely, partly because the net present value of this year’s offer can’t be precisely calculated without knowing exit yields. Local broker Allaria Ledesma estimates an average NPV of 43 cents assuming an exit yield of 11%, while TPCG sees the average NPV at 32 cents with an exit yield of 12% and including the swap ratio. In Argentina’s 2005 restructuring, it imposed losses of over 70%.

Argentina is no stranger to extended negotiations on sovereign debt after two defaults already this century, including a then-record $95 billion one in 2001. Its most recent default on foreign obligations, in 2014, came amid a drawn-out legal battle with creditors who held out of the 2001 restructuring, led by billionaire hedge-fund manager Paul Singer. Most of those claims were finally settled in 2016.

This time around, the government will face off with bondholders including BlackRock Inc., Pacific Investment Management Co., Ashmore Group Plc, Greylock Capital and Fintech Advisory Inc. Officials had been in preliminary talks with the creditors in the lead up to the offer.

“They propose what they always do: They want to collect more,” Guzman said in the interview with local journalist Horacio Verbitsky. “They ask that Argentina makes more fiscal adjustments, that it continues on the path it had been following, and that led to disastrous results. That’s not something we’re going to do.”

Some analysts, like SMBC Nikko’s Horn, warn that ownership of Argentina’s debt has recently shifted to distressed funds that are more concerned with wringing every penny they can out of Argentina, even if that means a lengthy court fight.

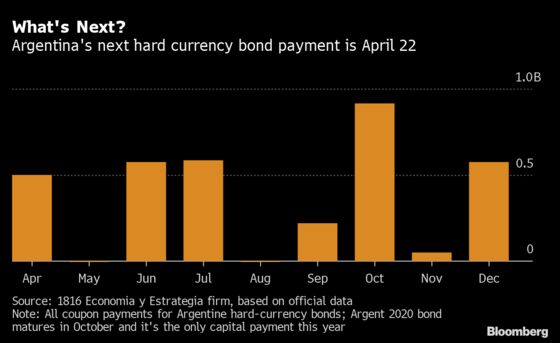

The country has $3.5 billion in payments on foreign-law bonds due the rest of 2020, according to Buenos Aires-based consulting firm 1816 Economia y Estrategia, including $500 million of interest due on April 22.

©2020 Bloomberg L.P.