Ant’s Canceled China IPO Highlights Global Fintech Challenge

Ant’s Squashed IPO by China Highlights Global Fintech Challenge

(Bloomberg) -- China’s torpedoing of Ant Group Co.’s initial public offering is the most dramatic example yet of the financial frictions emerging globally as fintech upstarts invade the territory of central banks and closely-regulated traditional lenders.

While the eleventh hour suspension of Ant’s record-busting IPO has more than a hint of Chinese internal politics about it, it also reflects the global struggle by regulators to catch up with the pace of innovation. Wake-up calls from Facebook Inc.’s Libra currency project to the collapse of Germany’s Wirecard AG are forcing that urgency.

Agustin Carstens, general manager of the Bank for International Settlements, laid out that challenge this week, saying that while the industrial revolution took a century to create structural change in economies, advances in technology have done so in a matter of years.

“We have moved from big tech being too small to care, in a few years they moved to being too large to ignore, and now we’re at a point of them being too big to fail,” he told the Hong Kong Fintech Week forum on Nov. 2.

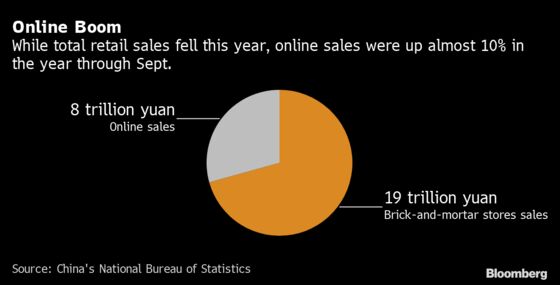

China has been a leader in the adoption of digital payments and financial services, which now pervade daily life in the world’s second-largest economy. Office workers scan QR codes to pay for their morning coffee or midday lunch, some 30% of all retail purchases are now done online, and digital payments are even replacing the red packets of cash given to family and friends during the Lunar New Year holidays.

Indeed, the nation is well on its way to becoming cashless through the use of private-sector led technology like Alipay and WeChat Pay. Jack Ma’s Ant, which leverages vast digital user bases to offer services from loans to payments, was set to raise $35 billion this week in what would have been the world’s biggest IPO and showcased China’s emerging leadership in financial innovation.

That growing role has won fintech firms praise. People’s Bank of China Governor Yi Gang has noted the “efficiency” they introduce into the financial system, while research published by the BIS has shown how they can provide funds for smaller firms in times of economic stress.

But the challenge -- and danger -- from independent payment providers and creators of digital currencies is a loss of regulatory control that’s now being met by a coordinated response from the state, and not just in China.

An extreme example of the risks involved is the high-profile collapse of Internet payments giant Wirecard earlier this year. The scandal exposed holes in Germany’s financial oversight system that officials are now working to close.

The former DAX-listed Wirecard collapsed in June when it said a quarter of its balance sheet didn’t exist, prompting a blame game among government agencies for the lapse in supervision. The debacle shone a light into what once had been a regulatory gray-area -- companies that aren’t banks providing international financial services on a large scale.

“These aren’t friendly little start-ups operating out of a garage somewhere, they’re global companies through which a lot of money flows,” said Raimund Roeseler, the head of banking supervision at German regulator BaFin. “You’ll only have a grip on the risks if you supervise them across borders.”

Crypto Currencies

With digital currencies, governments face a fundamental challenge to their once-exclusive privilege of creating money, and one that they’re responding to. Sweden and China have so far led the way to creating non-physical versions of their own fiat currency. The European Central Bank has accelerated its work on a digital euro, and even a wary U.S. Federal Reserve is researching in this direction.

Fed officials are investigating the costs and benefits of a digital currency, and have teamed up with researchers at Massachusetts Institute of Technology to build a “hypothetical digital currency oriented for central bank use.” They are also pursuing their own real-time payments system to compete with a separate one under development by private banks. What is clear from both initiatives is that the Fed has a strong interest in keeping a foot in dollar-based payment systems, no matter how they evolve.

The Bank of Japan is accelerating its study of financial innovation amid growing calls for digitalization after the pandemic highlighted the country’s continuing reliance on paperwork. It has also said it will start digital currency experiments next year. The Reserve Bank of India has created a “regulatory sandbox” for the fintech industry that allows the regulator, innovators, financial service providers and customers to test new products and services.

Pilot Scheme

After China’s government clamped down on digital currency exchanges, the PBOC is now trying to shore up the state’s primacy over currency and payments with a digital yuan of its own. In October, tens of thousands of Chinese were the first to spend digital yuan in a pilot scheme in the southern city of Shenzhen.

Part of the urgency among central banks to create digital currencies was prompted by the proposal by Facebook to create its own medium of exchange, Libra -- a so-called stablecoin that tracks an underlying asset. Couple that with Facebook’s two-billion-plus user base, and control of the financial system risks slipping from the grasp of its established guardians.

At the same time, the challenge for authorities is how to spur financial innovation that can be useful, without losing control. Just days before the Ant news, China’s central bank Governor Yi told the Hong Kong forum that fintech businesses have brought huge gains for consumers, increasing access to financial services in rural areas and spurring commercial banks to innovate. But the environment has also created risks, especially around data protection, he said.

‘Right Balance’

In the end, clearer regulation may end up benefiting fintech, rather than hampering its spread. In times when the difference between a traditional bank or currency and a fintech upstart for consumers is merely the color of an app on a smart-phone, what matters is which can be relied upon over the long term, according to Dutch central bank governor and Financial Stability Board member Klaas Knot.

“Regulation provides a level of trust,” he said.

But until regulators catch up with the pace of innovation, there’s likely to be more wobbles like Ant’s halted IPO or Wirecard’s scandal.

“The lesson for investors is that financial regulators still struggle to strike the right balance between promoting innovation, which won’t come from big banks, and clamping down on regulatory arbitrage and a build up of systemic risks,” according to David Loevinger, a former China specialist at the U.S. Treasury who’s now an analyst at TCW Group Inc. in Los Angeles. “Whenever they swing too far in one direction they eventually swing back.”

©2020 Bloomberg L.P.

With assistance from Bloomberg