Another Reason to Worry About Fed Ammunition: Eco Research Wrap

Another Reason to Worry About Fed Ammunition: Eco Research Wrap

(Bloomberg) -- The Federal Reserve is presiding over a solid economy right now. That’s good news, because it’s short on tools to deal with a downturn.

The central bank’s balance sheet remains swollen after years of quantitative easing and interest rates are nowhere near the levels they’ve reached in previous expansions, while fiscal policy is boosting the government’s debt load and potentially leaving less political will for future stimulus packages. As if that weren’t enough, new research suggests that rate cuts might work less effectively after a long period near zero.

That’s the lead item in this week’s economic research roundup. We also summarize a study on the racial marriage divide and a blog post on buyer power in the U.S. housing market. Check this column each Tuesday for the latest in new and interesting economic research.

Past Is Future

Mortgage Prepayment and Path-Dependent Effects of Monetary Policy

Published October 2018 on the National Bureau of Economic Research website

The Fed’s ability to boost the economy with interest-rate cuts today might depend on where borrowing costs stood yesterday, according to this NBER working paper by researchers at the University of Chicago, Copenhagen Business School and Northwestern University. The insight here is that a large share of U.S. household debt is tied up in fixed-rate mortgages. While many households might refinance if the Fed cuts rates to 2 percent after a long period at 3 percent, far fewer will react to a reduction if borrowing costs touched 3 percent briefly after a long period near rock-bottom.

“Looking only at the level of current rates provides an incomplete view of the Fed’s stimulative power,” the authors write. “It may take an extended period of time with elevated rates before the Fed regains ‘ammunition’ to stimulate the economy.” Even if the Fed can get rates substantially higher, that is, it’s likely to enter the next recession with less power than in the past.

It’s worth noting that Fed officials are acutely aware that they’re going to be short on traditional tools come the next downturn. Policy makers tend to focus on the fact that rates won’t rise as much as in the past this cycle, so they won’t have as far to fall. This added effect would only compound that concern.

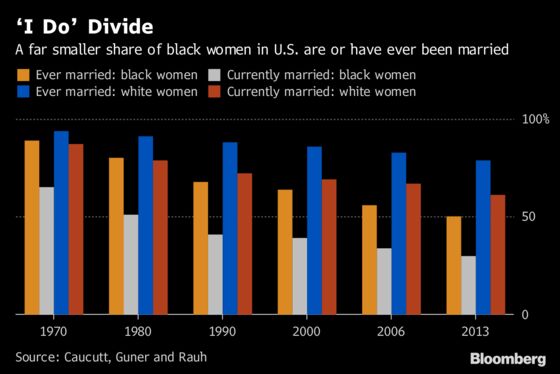

(Demo)Graphic: Race and Marriage

Is Marriage for White People? Incarceration, Unemployment, and the Racial Marriage Divide

Published October 2018 on the University of Chicago website

Young white women in the U.S. who have never married are about three times more likely to tie the knot than their black counterparts, and the racial marriage gap is growing, as the chart above illustrates. That is hugely important economically: marriage helps with wealth-building, and a large body of research suggests children living in married households generally have better access to economic resources and more stable lives at home.

This working paper by authors including the University of Western Ontario’s Elizabeth Caucutt suggests that there are two major developments disproportionately affecting the attractiveness of black men as spouses since the 1970s and 1980s (that matters because Americans tend to marry within their racial group). Technology-driven shifts to higher-skilled jobs and globalization have gutted major industries in inner cities, hitting black men hard. A dramatic increase in incarceration left almost 11 percent of black men between the ages of 25 and 54 in prison or jail as of 2010 -- more than five times as high as the rate for white men.

The researchers find that differences in employment and incarceration account for half of the racial marriage gap. The remainder owes to gender imbalances (there are more black women than men) and differences in educational attainment.

Buyer Power

20% of Recent Homebuyers Made an Offer Sight-Unseen, Down from 35% Late Last Year

Published Oct. 15 on Redfin Corp.’s blog

The share of U.S. buyers making offers before they’ve seen a house has fallen back to 2016 levels after a year of elevation -- and real-estate website Redfin’s economist Daryl Fairweather speculates that it might be an early indicator of a shift in power back toward buyers. The trend started to change earlier this year, when other housing indicators still looked red-hot. Since then, other data have confirmed that buyers are back in the driver’s seat.

--With assistance from Greg Quinn.

To contact the reporter on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Scott Lanman, Alister Bull

©2018 Bloomberg L.P.