(Bloomberg Opinion) -- Foreign firms eager for a $119 billion slice of China’s insurance market might just want to give Anbang Insurance Group Co.’s assets a closer look.

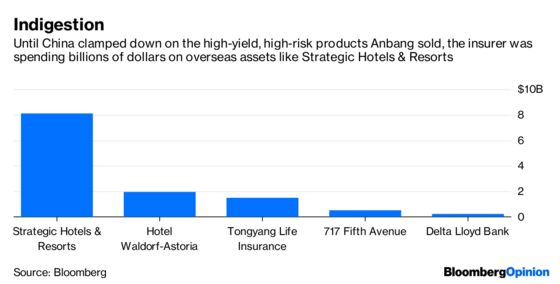

You’d be forgiven for wanting to steer clear of a firm that’s become the face of China’s toxic debt binge. But the timing could be right: It’s been almost a year since Beijing seized temporary control of Anbang as part of a broader crackdown on the high-yield products that funded its purchases of everything from the Waldorf Astoria hotel to its Chinese bank stakes. With the government looking for an exit soon, the insurer’s domestic-life business – with 800 billion yuan of assets ($119 billion) and 20 million customers – could be ripe for the picking.

Over the past year, Beijing has been busily cutting Anbang back down to size. The U.S. luxury hotels bought from Blackstone Group LP and the insurer’s Manhattan headquarters are now on the block. In China, a petrochemicals conglomerate from rust-belt Liaoning province is close to acquiring the firm’s health business, Bloomberg News reported Friday.

As far as we know, nothing’s been unloaded at fire sale prices. Still, the clock is ticking on the government’s initial goal to limit its takeover to at least a year, a time line that can be extended for another year if needed. Even without a discount, Anbang’s domestic-life businesses should pique some foreign interest.

In May, regulators issued draft rules that would grant foreign firms control of their Chinese insurance operations, setting the upper limit of ownership at 51 percent. Since then, France’s Axa SA has bought out its mainland partner while Germany’s Allianz SE is in the midst of setting up a wholly owned company.

For those foreign insurers struggling to buy out unwilling Chinese partners, or balking at the thought of building a mainland insurer from the ground up, buying assets makes sense. This is no easy market to break into: Some 93 percent of life insurance and 98 percent of non-life is dominated by local players. China’s Union Life Insurance, up for sale now, doesn’t have the baggage, but Anbang’s business could be more alluring.

In the 11 months through November 2018, Anbang Life had a total of 207 billion yuan in gross premiums and new investment funds, making it the fourth-biggest among Chinese life insurers, according to Bloomberg Intelligence analyst Steven Lam. While that's down from second place at one point in 2016, behind behemoth China Life Insurance Co., it remains a force.

Anbang still sells a lot of universal life policies – primarily savings products with a thin sliver of insurance. But it's stopped selling the problematic short-term ones whose maturities didn’t match up with the illiquid assets that backed them, like New York real estate. China imposed a ban on policies shorter than five years.

Another plus: Anbang still retains close relationships with many banks, which are key distributors of its products. (It owns around 5 percent of China Minsheng Banking Corp., the country’s 10th-largest bank by assets, according to data compiled by Bloomberg.) Taking even part of the insurer off Beijing’s hands should win some much-needed political goodwill for a foreign firm.

That’s not to say a buyer wouldn’t have its work cut out. Apart from the skeletons inevitably still lurking inside Anbang’s business, falling government bond yields are starting to hurt the investment income of many life insurers. Slumping auto sales are crimping demand for car insurance. The overall slowing economy doesn’t help matters. Still, having a foot in one of the world’s fastest-growing markets could be a wise insurance policy.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.