Americans Will Soon Need Extra Money They Saved in Lockdown

Americans Will Soon Need Extra Money They Saved in Lockdown

(Bloomberg) -- During the worst economic collapse in generations, U.S. households actually managed to put aside more money. It may not be enough to get them through the aftermath.

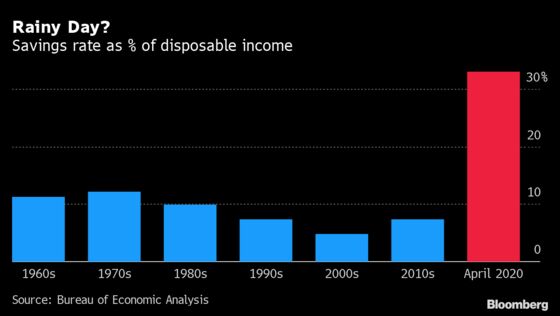

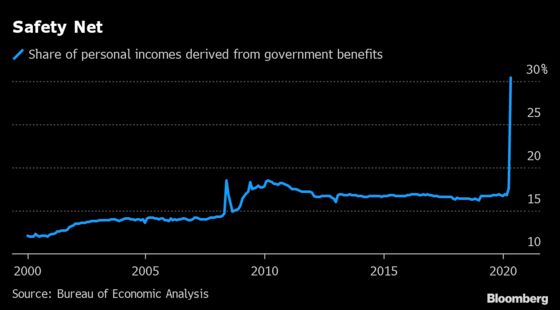

Savings rates soared to an unprecedented one-third of disposable income during the pandemic lockdown. Still-employed Americans found there weren’t many places to spend their paychecks, and expanded government benefits helped paper over the financial cracks for the tens of millions who lost their jobs.

But the fiscal lifeline is a temporary one. When it’s withdrawn -– and Congress is already discussing the timetable –- fragile household finances may come under growing strain.

Some 37% of adults told the Federal Reserve last year that they didn’t have enough cash to handle an unexpected expense of $400. That’s down from about 50% in 2013, as households bolstered their savings during the long U.S. expansion.

‘Not Very Liquid’

Still, it raises the question: if almost 2 in 5 Americans can’t handle a surprise car-repair bill, how will they cope in a drawn-out downturn? Hardly any economist expects the U.S. to return to 2019 levels of employment in the foreseeable future. The jobless rate, which fell as low as 3.5% last year, soared into the double digits by April.

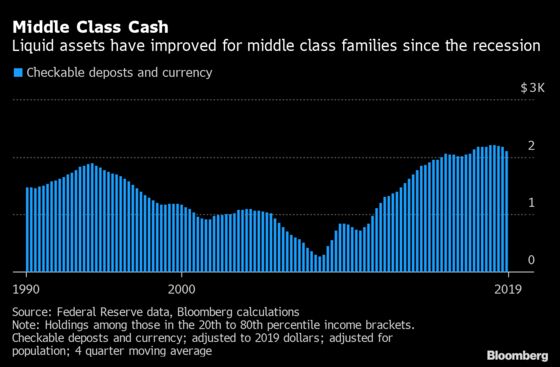

It’s not just the poor who are vulnerable, data suggest. Even well-off middle-class families may struggle to come up with the cash to endure an economic drought of more than a couple months –- because they tend to hold savings in assets that are difficult and costly to access in an emergency.

“A lot of the actual wealth people have is tied into forms of assets that are not very liquid,” said Princeton University economics professor Gianluca Violante. “It’s very hard to monetize in the short run.”

The prospect of having to do that can be wrenching.

Linda Chesky had what she describes as a “perfect little niche business” walking and boarding her neighbors’ dogs just outside Milwaukee. The 59-year-old was earning more than she’d made as a college teacher. But by mid-March, almost all her customers were stuck home with their dogs, and her income evaporated.

‘It’s Hard’

Now, instead of paying down her mortgage, she’s wondering if she’ll have to tap the equity stored up in her home. “It’s hard -- at almost 60, do I want to sell my house?” she said. “The plan really got changed significantly.”

Chesky said she’s filed for unemployment and an emergency small-business loan, but bureaucratic hurdles and delays have kept her from the cash. Many of those who lost jobs experienced similar glitches -- and even for those who haven’t, the pandemic-era payouts may not be available for much longer. Several Republicans in Congress oppose extending the additional jobless benefits after they expire next month.

That’s set to throw many Americans back on nest eggs that are illiquid. Tax breaks for mortgage interest and matching employer contributions to retirement accounts means it’s “smart and convenient” to save that way, says Princeton’s Violante. It just leaves households exposed to sudden shocks like unemployment.

In a paper co-written with two other economists, Violante coined the phrase “wealthy hand-to-mouth” to describe the phenomenon of mostly middle-class, cash-poor savers. He found that at age 40, they held a median illiquid wealth of around $50,000.

Credit Lines

When a crisis hits, hand-to-mouth households typically have to take on more debt -- assuming someone will lend to them -- or make premature withdrawals from retirement accounts. The latter course often involves selling investments at the worst possible time, after they’ve dropped in value.

In the U.S. right now, it’s getting tougher for recession-hit homeowners to borrow against their property. Lenders have tightened their standards, with Wells Fargo & Co. and JPMorgan Chase & Co. announcing in April that they’ve suspended new home-equity lines of credit.

When it comes to tapping retirement accounts, policy makers have been easing the path. Under the CARES Act, a pandemic relief plan approved by Congress in March, Americans have the option to withdraw as much as $100,000 this year without the usual penalties.

At least in the early weeks, it looks like not many opted to do so. Fidelity Investments said that 1.2% of its retirement-plan customers, or about 295,000 people, had taken a CARES Act distribution in May (the median sum was $5,000). Vanguard Group cited an April figure of “slightly less than 1%.”

‘Stay Afloat’

There’s a good reason for that reluctance, especially for older workers who are short of time to replenish any funds they withdraw, said Teresa Ghilarducci, an economics professor at the New School for Social Research in New York.

As an alternative, “debt is going to look very attractive to people,” she said – whether on credit cards or against homes. “If you don’t have liquidity, you have to borrow liquidity.”

In an extended downturn, even many of those who did have liquid savings may find themselves living hand-to-mouth and thinking of ways to access illiquid wealth. That’s one reason why so many Americans are glued to the economic numbers -- and cheering the ones that suggest the country may pull off a rapid V-shaped rebound.

In Wisconsin, the official re-opening happened in mid-May. But most of Chesky’s former customers are still working from home and her boarding business, usually a huge source of revenue over the summer, is on track to net her less than $1,000 next month.

For the present, she’s waiting on government help – and for the future, she does see one glimmer of hope: the huge number of people who seem to have adopted dogs while in quarantine. Eventually, she figures, their owners will be back at work.

“I see potential opportunity coming,” she said. “If I can stay afloat until then.”

©2020 Bloomberg L.P.