Why Metals Traders Shrugged Off Rusal’s Jailbreak

(Bloomberg Opinion) -- Aluminum doesn’t care about your political machinations.

That’s certainly the impression the market has given to news that the Trump administration is preparing to remove sanctions on United Co. Rusal. The Russian company accounts for about 40 percent of ingots in London Metal Exchange-registered warehouses. Yet far from losing their mind at the prospect of one of the world’s biggest producers being back in business early next year, three-month forwards on the metal fell a scant 1.1 percent. (Rusal, meanwhile, jumped as much as 25 percent when its shares opened in Hong Kong.)

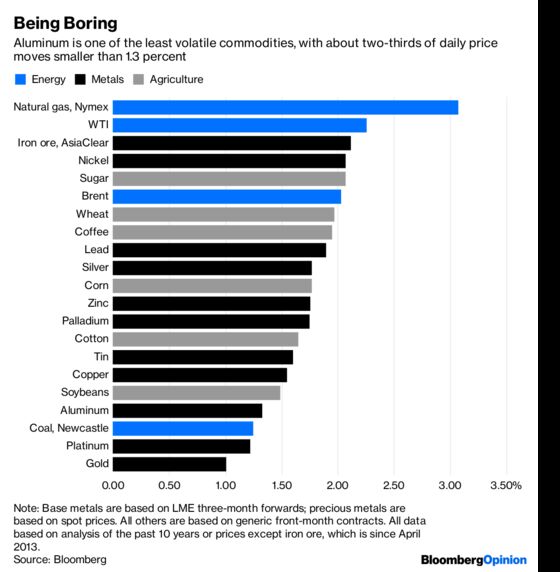

There’s one obvious reason for this relatively muted reaction: Aluminum is one of the most somnolent commodities out there. Its sigma, or standard deviation – the plus or minus band within which about two-thirds of daily moves fall – is 1.3 percentage points, compared with levels above two percentage points for most energy contracts. Among major commodities, only platinum and gold are more stable, according to our analysis of the past 10 years of trading data:

Why should this be? It ultimately comes down to warehousing. One reason natural gas is so, er, volatile is that it’s relatively costly to stockpile or throttle back on supply, while demand shows a marked seasonal pattern that makes storage essential to the functioning of the market.

The U.S. typically has between about 15 days and 45 days’ worth of gas in tanks and underground caverns. As a result, any small miscalculation can see the market suddenly looking dangerously tight, as happened last month when futures surged almost 50 percent in a fortnight. That was the result of a short squeeze triggered by fears that storage levels were too low to cope with a cold winter.

It’s a different picture with aluminum, which has only recently managed to eliminate the enormous mountain of stored metal built up after the 2008 financial crisis. LME stockpiles, which normally average around 10 months’ worth of deliveries, rose to more than a year this week as fresh deliveries pushed the volume available to an eight-month high. All that inventory provides a formidable shock absorber when there are sudden turns in the market. The 10 percent import tariff imposed by the Trump administration earlier this year had a far more decisive impact.

The market reaction is also likely to be particularly mild given the longstanding lack of clarity around the administration’s sanctions on Rusal.

Its controlling shareholder Oleg Deripaska has had a well-documented murky relationship with President Donald Trump’s former campaign manager, Paul Manafort, and this year its U.S. unit received (and then lost) an exemption from import tariffs – an unusual concession given that the parent company itself is under sanctions. A crucial element of the restructuring that’s allowing Rusal to be spared is a plan to transfer some of Deripaska’s shares to VTB Bank OAO, a state-owned Russian lender that is itself on the U.S. Treasury’s sanctions list.

While all that probably represents cock-up as much as conspiracy (putting sanctions on Rusal in the first place is the opposite of what you’d expect if the administration was in cahoots with Deripaska), it’s left a residual sense that the company would escape the full force of the law. As a result, traders have for months been discounting the risk of Rusal’s product being withdrawn from the market.

That focuses attention on the bigger risks emerging in China. State-owned giant Aluminum Corp. of China Ltd. could be headed for a loss next year because of the country’s slowing economy, according to Goldman Sachs Group Inc. About 40 percent of smelters globally are cash-flow negative at current prices, Kathrine Fog, head of corporate strategy and analysis at Norsk Hydro ASA, told an investor call last month.

The Caixin China Manufacturing Purchasing Managers’ Index has been edging close to levels indicating a contraction in activity over the past three months. The economic hub of Guangdong province has been told to stop producing a local PMI index altogether, according to the South China Morning Post.

That points to a situation where aluminum’s perpetual oversupply starts reasserting itself. The LME metal was already at a 16-month low on Tuesday, before the Rusal news. Bullish traders should be glad this metal has so little sigma. Matters could be a whole lot worse if it was more volatile.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.