All Signs Point to Soft U.S. Jobs Report After Run of Weak Data

This time, Wall Street economists see a more persistent storm at play: The trade war and manufacturing recession.

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

Storm clouds developed quickly over the U.S. labor market this week.

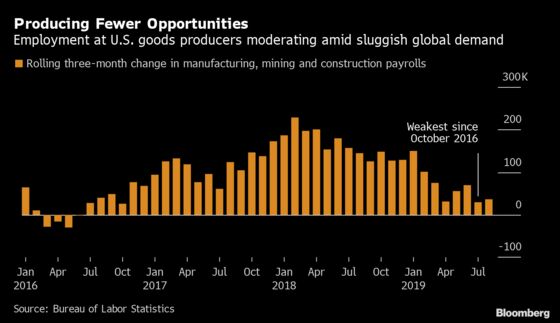

The lowest manufacturing jobs gauge since 2016. Slower private hiring. A sharp drop in small-business hiring plans. And the worst U.S. services-employment index in five years, or nine years, depending on which measure you prefer.

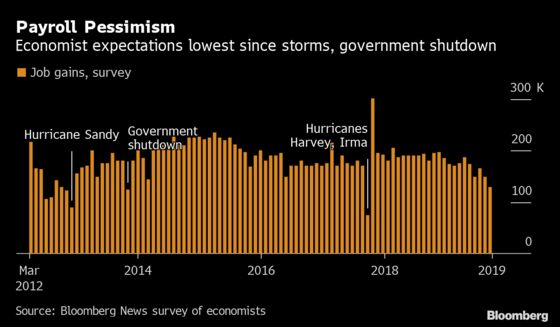

That’s the backdrop from three days of disappointing data heading into Friday’s September jobs report from the Labor Department. Analysts are bracing for more downbeat figures, with their pessimism for payrolls on par with times when hurricanes slammed the country in 2017 or when the federal government shut down in 2013.

This time, Wall Street economists see a more persistent storm at play: The trade war and manufacturing recession. Those factors are starting to permeate the economy at a time when companies are already struggling with a shrinking pool of qualified workers.

The combination of forces has pushed down the median estimate for private payrolls to a gain of just 130,000 last month. That’s the weakest projection heading into a jobs report in seven years, outside of months affected by events such as major storms or the shutdown. Estimates for total nonfarm payrolls are higher, at 145,000, because of an expected boost from temporary census hiring.

A reading that’s even weaker than predicted would probably all but lock in investor expectations that the Federal Reserve will cut interest rates Oct. 30 for a third straight meeting. It would also boost chances of another reduction in December, completing a reversal of all four hikes from 2018.

Traders already increased bets this week on Fed rate cuts after the run of weak reports led by surveys from the Institute for Supply Management covering manufacturing and non-manufacturing industries. Indicators from IHS Markit, the ADP Research Institute and the National Federation of Independent Business also showed some cooling.

“Leading up until this week’s ISM data, I think the question was how weak did the data need to be to get the Fed to cut rates later this month,” said Kevin Cummins, senior U.S. economist at NatWest Markets. Now the question has become, “how strong do payrolls need to be in order for the Fed not to cut rates?”

What Bloomberg’s Economists Say

“The economy is losing momentum in the back half of the year to a degree sufficient to meaningfully depress the pace of hiring. Job creation has already decelerated markedly, and diminished business confidence in recent months will exacerbate the defensive posturing among hiring managers.”

-- Carl Riccadonna and Yelena Shulyatyeva

Click here to read the full preview.

For President Donald Trump, who has repeatedly pinned any economic weakness on the central bank, a sluggish labor market could pose a threat to his reelection in 2020. Currently the U.S. is on track to add about 1.9 million jobs this year, which would be the smallest gain since 2010 and down from 2.7 million in 2018.

“It’s starting to roll into one big ball of negativity,” said Jennifer Lee, a senior economist at BMO Capital Markets in Toronto. “You just don’t have the supply of workers out there, but now it’s starting to become worse.”

Median Estimates for September Jobs Report:

|

“If the company’s dealing with the manufacturing slowdown, trade with China issues, weaker demand, it falls into your hiring expectations: ‘If we’re not going to get that many orders, we don’t need as many people,’” Lee said.

Other indicators already point to a slowing economy and weaker growth ahead. Companies are pulling back spending as tariffs weigh on business decisions and global demand slides. The August gain in consumer spending was the smallest in six months.

So far, manufacturing has been hit hardest, so investors and economists will be keenly watching the September report to show whether the pain has spread more broadly in the labor market -- whose relative strength has helped keep the record-long U.S. expansion from turning into a recession.

“There’s much more scrutiny on the nonfarm payrolls and looking to see: Is the U.S. economy slowing down with the rest of the world?” said Zhiwei Ren, a portfolio manager at Penn Mutual Asset Management, which oversees $28 billion. “In the last few months, it hasn’t been a great focus of the market because the U.S.-China trade talks, and Fed policy has been more important. But now people are starting to question the strength of the U.S. economy.”

The recent job numbers already suggest that employers are either having difficulty filling positions, are hiring fewer people due to weaker demand, or both.

The latest ISM manufacturing survey already delivered the economic evidence the Fed needs to continue cutting interest rates, which Friday’s numbers will likely confirm, according to Gene Tannuzzo, a deputy head of fixed income and portfolio manager at Columbia Threadneedle Investments.

“This certainly is incrementally worse data,” said Tannuzzo, who expects two more cuts this year.

--With assistance from Chris Middleton and Jeff Kearns.

To contact the reporters on this story: Katia Dmitrieva in Washington at edmitrieva1@bloomberg.net;Reade Pickert in Washington at epickert@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Vince Golle

©2019 Bloomberg L.P.