After Hike, Fed Minutes May Flesh Out Thinking on Path Ahead

Meeting minutes set for release are unlikely to offer answers, but may drop a few hints about how officials are thinking.

(Bloomberg) -- Market participants have a burning question for the Federal Reserve: How high will policy makers hike interest rates before pausing for a breather?

Meeting minutes set for release at 2 p.m. Wednesday in Washington are unlikely to offer answers, but they may drop a few hints about how officials are thinking.

At its Sept. 25-26 gathering, the policy-setting Federal Open Market Committee raised interest rates and scrapped its description of the monetary stance as “accommodative.” Since then, Chairman Jerome Powell and New York Fed President John Williams have each delivered public remarks multiple times, and their colleagues have popped up to speak from Michigan to Massachusetts.

The flurry of Fed-speak has made it clear that officials still think policy is easy and are comfortable with continued gradual increases, but have yet to decide how high rates will ultimately climb. Now the minutes could flesh out what factors are informing their debate on the location of the neutral rate -- a highly-uncertain dividing line between easy and tight money -- and whether they should go above it.

“Do they give you any insight yet on what they think is neutral?” said Stan Shipley, an economist with broker and researcher Evercore ISI. “That’s still going to be a debate, do they think that they should move away from tightening to neutral rates, and what is neutral.”

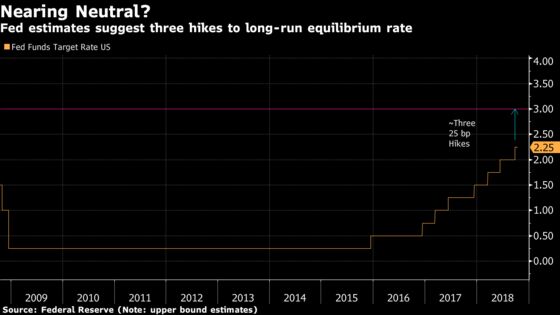

Neutral or Not?

It’s been an eventful couple of weeks since the Fed last met: rates on longer-dated Treasury securities have risen, stock prices have taken a hit, a deal to update the North American Free Trade Agreement has been announced, and President Donald Trump unleashed a rash of comments criticizing the central bank’s rate increases. All of that activity, paired with the bevy of recent Fed speeches, could leave these minutes slightly out of date.

Still, the notes could help to cut through some of the noise surrounding neutral rates. Powell and Williams, one of his key lieutenants, have been de-emphasizing the equilibrium rate, commonly called r-star. That’s because it’s difficult to estimate with precision.

But abandoning some sort of long-run equilibrium estimate altogether is akin to hiking without a destination: officials regularly invoke r-star to give guidance on how high rates might rise and whether they’ll cool off the economy. Chicago Fed President Charles Evans said last week that policy may exceed his estimate of neutral -- currently three rate hikes away -- by 50 basis points, for example.

“What we’re looking for some clarity on is even how much the whole concept of r-star is guiding them here,” said Priya Misra, head of global rates strategy at TD Securities in New York. “If you really don’t believe in neutral because it’s such a wide uncertainty band, then how can you say you’ll go above that level?”

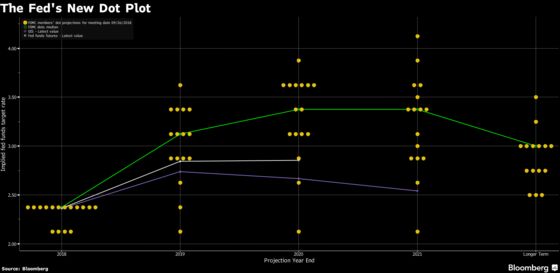

Overshoot Plans

Evans isn’t alone. The central bank’s September economic projections suggest the median Fed official expects to exceed the long-run equilibrium rate by one quarter-point hike next year and another in 2020.

That didn’t mark much of a change from the prior dot-plot released in June, but minutes could shed light on officials’ reasons for favoring a slightly-restrictive stance.

On a related note, Fed Governor Lael Brainard suggested in mid-September that fiscal stimulus could boost the near-term neutral rate, requiring higher rates to keep the economy on an even keel. Her logic might get some air time in the minutes.

Trade Troubles

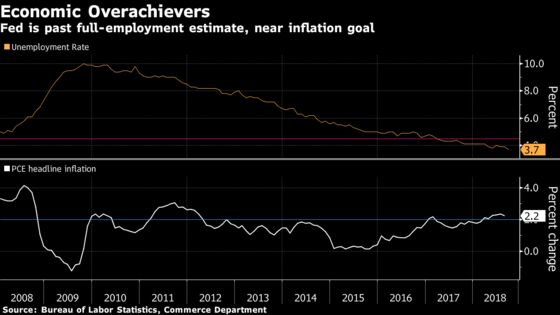

Fed officials have sounded pleased in recent speeches about getting close to their twin goals of maximum unemployment and low and stable inflation.

They are more worried about America’s ongoing trade spats.

It’s important to watch “how much they talk about trade as a potential dark side, potential sign of impending weakness,” said Alan Detmeister, an economist at UBS Group AG who formerly headed the Fed’s research and analysis of prices and wages.

Trump said Sept. 17 that the U.S. would impose tariffs on $200 billion of Chinese goods, escalating America’s trade spat just ahead of the Fed meeting. While the ongoing tiff isn’t yet showing up in economic data -- a fact Powell and his colleagues have pointed out -- it could feed through to inflation later in the year, Detmeister said.

That could matter for markets. Equity prices fell after a bump-up in wages at the start of this year. If inflation moves higher and stocks swoon, the Fed could face tough choices.

Already, the central bank may grapple with a miniature version of that problem as analysts blame impending interest-rate hikes for the recent stock dip. Minutes will offer little insight into how the Fed will react -- the selloff came post-meeting -- but regional Fed speakers have taken it in stride.

“Tighter policy should mean tighter financial conditions, and we should see some of those tighter financial conditions in lower equity valuations, higher yields,” said Laura Rosner, senior economist and partner at MacroPolicy Perspectives LLC in New York, who formerly worked at the New York Fed. “I think it’s a healthy thing, from the Fed’s view.”

--With assistance from Christopher Condon.

To contact the reporters on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net;Ivan Levingston in New York at ilevingston@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Scott Lanman

©2018 Bloomberg L.P.