A Decade of Trying and Yuan Trading Has Barely Scratched Dollar

After a Decade of Drama, China’s Yuan Reform Has Far Way to Go

(Bloomberg) --

Out of the depths of a global credit crisis that showcased an outsized role for the U.S. dollar, Chinese policy makers forged a plan to raise the profile and influence of their own currency. That hasn’t panned out so well, and the coming decade may see yet new headwinds.

A botched mid-2015 move to let the market have a greater role in setting the yuan spooked global investors, eventually pushing Beijing to adopt its current framework. That’s one that welcomes inflows of overseas capital while limiting the outflow of domestic money and promoting the yuan’s role in commerce, if not in finance.

The model has helped limit the yuan’s depreciation even in face of the trade war with the U.S., with foreign ownership of China’s bond market hitting a fresh record in September. And some observers see a potential game changer ahead if a swathe of the world’s energy and commodity trade becomes priced in yuan. But key to the currency’s role in the 2020s will be the Communist Party’s stomach for easing control.

“The false narrative is the idea that a country running current-account surpluses and strict controls over capital outflows could have a truly internationalized currency in the first place,” said George Magnus, research associate at Oxford University’s China Centre. “It wasn’t true when the internationalization debate started several years ago, and it’s no more possible now.”

Magnus, author of “Red Flags: Why Xi’s China Is in Jeopardy,” argued that China’s financial system “would not be able to cope” with ending capital controls and allowing the currency to float, and that’s not likely to change “for some years to come.”

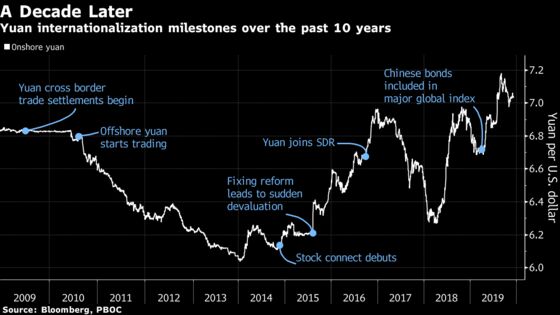

Things were quite different when China launched offshore trading in the renminbi, the official name for its currency, with the CNH ticker in August 2010. That came months after it ended a de facto peg to the dollar adopted during the global financial crisis, and amid widespread expectation for the yuan to see sustained appreciation.

Later, an offshore bond market denominated in yuan expanded in Hong Kong, known as Dim Sum securities. Yuan deposits in climbed in the city, and China signed agreements with counterparts setting up direct trading between its currency and others. Hong Kong now supplies around half of the world’s offshore yuan liquidity, the Hong Kong Monetary Authority said in an emailed response to questions.

Hong Kong serves as an ideal testing ground for yuan internationalization measures, said Darryl Chan, an executive director at the HKMA.

A half-decade of progress came to an abrupt end in 2015, when China, battling an economic slowdown and a burst bubble in its stock market, devalued the yuan and overhauled its exchange-rate calculation in a manner that unsettled international investors. An exodus of domestic money saw the nation’s foreign-exchange reserves tumble by about $650 billion, triggering a clampdown on capital outflows that continues today.

Depreciation remains a concern, all the more so with the U.S. tariff hikes that began on Chinese goods last year putting pressure on the currency. That leaves little likelihood of major regime changes for the yuan for now. The onshore yuan surged as much as 1% on Friday, the most in a year, as people familiar with the matter said President Donald Trump had signed off on a phase-one trade deal with China.

“The current environment may not be ideal to push for full convertibility,” as Wang Ju, director and senior foreign-exchange strategist at HSBC Holdings Plc in Hong Kong, puts it. Still, she says “the journey of yuan internationalization will continue and will never be reversed even though we may see some back and forth along the way.”

China continues to work on market-structure issues to encourage broader inclusion of its onshore stocks and bonds in global indexes -- things such as improving hedging tools. It launched oil-futures trading in yuan, open to foreign participation, last year and has followed up with iron-ore contracts.

Should Beijing go further and insist on oil imports being paid in yuan, that could help lead to a “turbocharging” of the currency in the global financial system, Mansoor Mohi-uddin, a Singapore-based senior macro strategist at NatWest, wrote in a note this month. While it could eventually allow the yuan to challenge the euro as the main alternative to the dollar, the move could also bring its own problems.

“The upward pressure on the exchange rate from capital inflows will not be countered by capital outflows,” if China doesn’t allow mainland investors to buy overseas assets, he said. Over time, that may strengthen the yuan so much that export competitiveness is undermined, he said.

The People’s Bank of China said in its annual yuan internationalization report for 2019 it will continue to remove obstacles for investors to use the currency and open up its financial markets. The central bank didn’t respond to a fax seeking comment for this story.

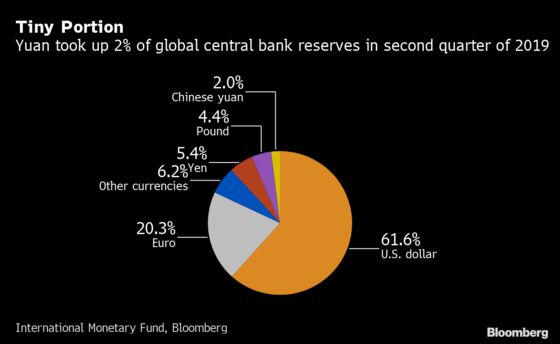

For now, the yuan’s share in global payments and in central bank reserves remains low, at about 2% or less on both counts. Total foreign holdings of domestic bonds and stocks stood at 3.95 trillion yuan ($566 billion) at latest count -- or the equivalent of Belgium’s and Brazil’s combined holding of U.S. Treasuries.

What’s becoming less negligible is overseas holdings of China’s stocks and bonds. Again, that carries potentially some vulnerability for the country. When foreign ownership was around 2% or less, as was the case just two years back, overseas investors were marginal to price moves in China’s markets -- and thus to policy makers. But as their role grows, the potential for a withdrawal of that money could pose a risk, and influence borrowing costs.

“If foreign ownership gets to 10% or more, China will get concerned about foreign dominance of the market, they won’t want that,” Michael Spencer, chief Asia Pacific economist at Deutsche Bank AG, said in reference to the bond market. The worry would be “we lose monetary-policy autonomy,” he said.

Spencer sees China shifting to become more comfortable with offshore use of the yuan in the case of “some kind of resolution” of the trade war with the U.S. If so, it augurs a fresh set of challenges for policy makers as China’s financial integration proceeds in the 2020s.

--With assistance from Ran Li and Selcuk Gokoluk.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Livia Yap in Shanghai at lyap14@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Christopher Anstey

©2019 Bloomberg L.P.