Abenomics Virtuous Cycle Lacks Traction as Milestone Looms

Since Abe returned as premier in December 2012, Abenomics has aimed to secure solid growth and generate stable inflation.

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Apple Podcast, Spotify or Pocket Cast.

As Shinzo Abe approaches the milestone of becoming Japan’s longest-serving premier later this week, his namesake economic strategy still lacks traction despite progress in supporting growth.

Since Abe returned as premier in December 2012, Abenomics has aimed to secure solid growth, generate stable inflation and reinvigorate Japan’s companies. Most of the heavy lifting has been done by the Bank of Japan as the constraints of two sales tax increases effectively tightened the government’s purse strings.

Nearly seven years into the program, prices are rising, Japanese firms are making more money and the jobless rate is near a 27-year low. In 2019 the economy has continued to expand despite a global downturn that has battered exporters, suggesting that a domestic engine of growth is in place.

Yet a virtuous cycle of rising corporate profits that feed into higher wages, consumer spending and inflation still appears to be in low gear. Meanwhile, progress remains limited on structural reforms aimed at making Japanese firms more competitive and better utilizing the economic potential of women.

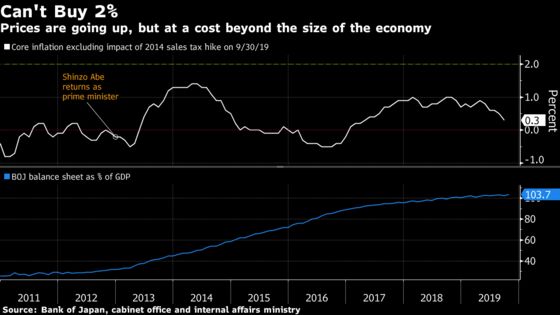

A huge push by the BOJ to generate 2% inflation in around two years has segued into a long-haul battle as price growth has stayed stubbornly low. That problem isn’t isolated to Japan, given the downward pressure on prices from globalization, e-commerce and cheaper commodities. But the reluctance among consumers and companies to accept higher prices after years of falling prices is specific to Japan.

The central bank’s massive bond buying campaign to fuel inflation has landed the BOJ with a pile of assets that’s bigger than the size of the world’s third-largest economy. In 2016 it changed tack to focus more on interest rates than asset purchases, but negative rates and low bond yields have squeezed banks and life insurers, adding to the impression that the central bank is running out of ammunition.

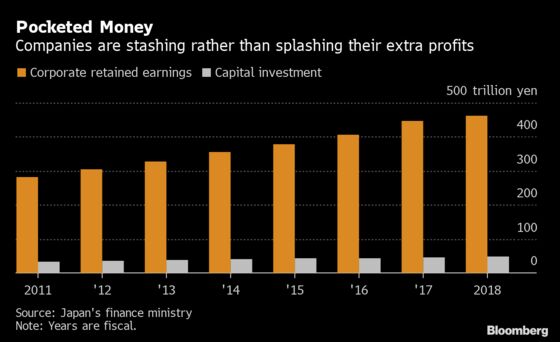

Still, the BOJ’s stimulus has contributed to one of the key successes of Abenomics: a weaker yen. The more favorable exchange rate has delivered record corporate profits and higher stock prices, leading to more capital spending, larger dividends and more share buybacks.

That’s progress, but companies are still hoarding cash that the government would rather see spent on investment and higher wages that can fuel the economy’s virtuous cycle.

While economists argue that pay gains of more than 2% are needed to reach the inflation target, average wage gains under Abenomics have averaged just 0.3% through September this year, according to a Bloomberg calculation based on labor ministry data. That means pay has been falling compared against inflation.

Increasingly, senior government officials, including Abe himself, have switched the benchmark of Abenomics’ success away from the inflation goal toward the economy’s generation of jobs. Japan’s jobless rate is lower than 37 other countries in a quarterly OECD survey, though a large factor behind the tightness of the labor market lies with Japan’s falling and aging population.

What Bloomberg’s Economist Says

“The political stability of Prime Minister Shinzo Abe’s administration has provided key support for economic growth under Abenomics amid a spread of political uncertainty around the world. Pending issues are the Bank of Japan’s balance sheet--now larger in size than Japan’s GDP--delays in putting the primary balance on track to reach a surplus, and a lack of labor market reform.”

--Yuki Masujima, economist

To contact the reporter on this story: Yoshiaki Nohara in Tokyo at ynohara1@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net, Paul Jackson, Karthikeyan Sundaram

©2019 Bloomberg L.P.