A U.S.-China Trade Deal May Disappoint Investors

A U.S.-China Trade Deal May Disappoint Investors

(Bloomberg Opinion) -- When data showed China’s industrial production and retail sales slowed significantly in the final months of 2018, U.S. President Donald Trump took credit, telling Fox News that “China’s economy, if it’s in trouble, it’s only in trouble because of me.” The implication is that global trade is a zero-sum game, and losses in China resulting from U.S. tariffs translate to gains for the U.S.

For investors, that may turn out to be a Pyrrhic victory. The U.S. accounted for 24 percent of the world’s economy at the end of 2017, down from 31 percent in 2000, according to World Bank data. The share will continue to shrink over coming decades. According to a study by PricewaterhouseCoopers Global using a somewhat different methodology, the U.S. will be only the third-largest world economy by 2050, accounting for 12 percent of gross domestic product.

The largest American companies have been highly dependent on foreign sales, suggesting that weakness abroad will translate into downward guidance to investors. Foreign revenue for the members of the S&P 500 has consistently accounted for between 43 percent and 48 percent of total sales in the decade ending 2017.

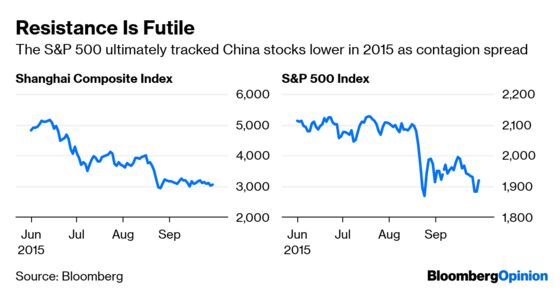

What this means is that developments in the rest of the world will increasingly have an impact on U.S. financial markets. Global markets got a taste of this in mid-2015 when the Shanghai Stock Exchange index fell by 43 percent between June and August. While the S&P 500 initially seemed immune to the slump, it eventually dropped by 12 percent over five weeks in July and August.

Corrections in Chinese equities and weakness in the yuan were cited as important factors in the Federal Reserve’s decision to postpone the first interest-rate increase since the financial crisis that had been planned for September 2015.

Among U.S. companies with substantial business in China, Apple Inc. started the ball rolling this year by warning in early January that it was slashing its sales forecast for 2019 amid an “economic deterioration” in China. Kevin Hassett, Chairman of the White House Council of Economic Advisors, said in an interview that “a heck of a lot of U.S. companies that have a lot of sales in China” are “basically going to be watching their earnings be downgraded.”

A few days after Hassett’s comment, Nvidia Corp., a maker of graphics processing units for gaming and professional markets, and Caterpillar Inc., the world’s largest construction equipment producer, saw their shares fall after blaming different segments of the Chinese economy for the deterioration in their prospects this year.

Fed Chairman Jerome Powell recognized the growing importance of the rest of the world on the U.S. economy when he pointed last week to the continuation of the trade war and a global economic slowdown as factors explaining the central bank’s 180-degree shift in policy from a December forecast of at least two rate hikes in 2019 to suggesting a pause in the tightening cycle may be warranted.

The problem for U.S. markets is that a dovish Fed may not have the same firepower that it had in the past. Even though equities reacted positively to the Fed’s pivot, the outlook may eventually depend more on the forthcoming summit involving Trump and Chinese President Xi Jinping before the current standstill on tariffs ends on March 1.

If the talks end badly and Trump increases tariffs on a range of Chinese products from the current 10 percent to 25 percent, expect China’s economy to slow further and for more U.S. companies to join Apple, Nvidia and Caterpillar in lowering expectations. For investors, it would be a prescription to allocate investments away from equities toward higher grade fixed-income instruments.

Chinese developments are not the only ones behind the gathering storm clouds. The European Union economy is buffeted by two major forces damping activity. Germany, the region’s largest economy, is also the world’s most export-dependent. U.S. tariffs on steel, aluminum and cars resulted in German gross domestic product contracting in the third quarter, and barely growing in the fourth quarter. With the German slowdown likely to persist in 2019, the impact will be felt all over Europe, and U.S. exporters may find their sales affected as well.

The second development Europeans have to contend with is the uncertainty over Brexit that is set to occur March 29. With the U.K. and the EU unable to agree on the terms of a divorce, the probability of a “hard” Brexit has risen. Unless the two sides agree to postpone the scheduled date for the separation and keep negotiating, it could be chaotic with no rules governing trade, capital flows or transportation. Under these circumstances, expect U.S. equities to experience a correction, and yields on Treasury securities to fall even lower.

The conclusion is not that domestic U.S. developments such as another government shutdown or a “Fed Put” do not matter. They do in the short run. For investors with a longer time horizon, negative global developments — continued subpar economic growth in Europe or a prolonged the trade war — are likely to be a lose-lose situation with few hiding places either in the U.S. or abroad.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.