(Bloomberg Opinion) -- There’s a glitzy side of Singapore property: the cavernous shopping malls; the tall office buildings; the pricey condominiums; the luxury hotels; and the hospitals where rich Indonesians and Bangladeshis seek treatment and five-star customer service.

But there’s also a vibrant market at the non-sexy end of the spectrum: the warehouses, the factory sheds and, increasingly, the data centers. Their owners are industrial real estate investment trusts, which collect rent and pass it on to unitholders. It’s something that appeals to an aging population that values the certainty of dividends more than the headiness of growth.

Some landlords, like Mapletree Industrial Trust, command market prices twice their net asset values. Others, like Sabana Shari’ah Compliant Industrial REIT, or Sabana REIT, trade at a chronic discount. This column is about Sabana, and how it became a vehicle in a Swiss value investor’s campaign to make confrontational shareholder capitalism work in polite and obedient Singapore.

Sabana is among the smallest of Singapore REITs: Its 18 properties across the island-state add up to a little more than 4 million square feet. But it has historically had big problems of governance and performance. In 2017, Sabana scrapped a property purchase from its then sponsor under pressure from unitholders; the REIT manager’s chief executive officer quit.

Still, performance remained lackluster. In September 2018, Sabana agreed to sell a factory site for less than half its book value, but the buyer couldn’t secure regulatory approvals and abandoned the deal. The factory spent all last year earning nothing. A warehouse also became tenantless in the fourth quarter of 2019, shaving a few percentage points off the property owner’s low occupancy rate.

It was relief to unitholders when in June last year control passed to to ESR Cayman Ltd., a Hong Kong-based logistics firm that owned another industrial landlord in Singapore. ESR-REIT is nearly four times as big as Sabana. The change in ownership perked up the interest of Jan Moermann, a Swiss who's acquired a reputation as an activist investor in Singapore. Assisted by its Malaysian-born, Singapore-citizen research head Havard Chi, Moermann’s Quarz Capital Management Ltd. was already building a stake because it believed Sabana had good properties that could be managed better.

Toward the end of last year, Moermann called on ESR Cayman to merge its two Singapore real-estate trusts. Both Sabana and ESR-REIT were competing in the same market for industrial property. Conflict was a possibility, even though the managers of the two trusts say they don’t share information on strategy or operations.

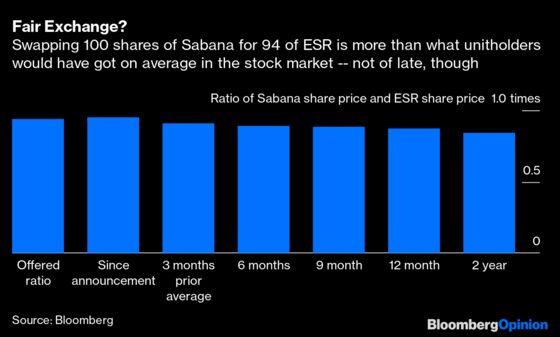

Moermann put a value of 54.5 Singapore cents ($0.4) apiece on Sabana shares in a cash-plus-stock deal. But when the all-stock merger with ESR-REIT was finally announced in July, each Sabana unit was implicitly judged to be worth less than 38 Singapore cents, way below the book value of 51 cents. “We’re not here to fight over who gets one more piece of salami on the pizza,” said Adrian Chui, chief executive officer of ESR-REIT. “We want the pizza to become bigger.”

The Sabana management has publicly said that swapping 100 units for 94 units of ESR is a fair deal. That’s nearly 12% more than what the trust’s investors would have got from the market on average in the two years prior to the announcement.

The question for unitholders isn’t so much whether ESR is a good home, but whether they can move in on better terms or aspire for a different sanctuary. Donald Han, the Sabana manager’s CEO, is right: Small in his business is unsexy. Even with low debt, the landlord can’t grow because most assets are already pledged. However, if ESR can secure cheaper refinancing for those properties, so can another strong owner. Now that Sabana is adding a 35,000-square-feet retail and F&B component to its flagship property, dropping the Shariah compliance tag to allow tenants that deal in alcohol or pork could also be of modest help.

Scouting for suitors from around the world after the Covid-19 travel restrictions end might throw up alternatives. Conversely, it’s also possible that the pandemic dislocation, combined with Singapore’s tightening restrictions on foreign workers, will erode the value of industrial properties, hurting Sabana unitholders if they hold out. Their portfolio is too small to afford the downtime involved in costly redevelopment.

Quarz and Hong Kong-based Black Crane Capital, which own 11% of the Sabana stock between them, are prepared to vote against the current offer when a shareholders’ meeting is called. They’re also asking the current Sabana management to leave if the merger fails.

In Singapore’s West-meets-East culture, people in positions of authority are rarely challenged so openly. Yet someone needs to do it. The chief of city’s Securities Investors Association invited the managers of the two merging entities and an analyst to discuss the deal. The moderation was courteous, and the participants agreed on everything.

How can there be a market without disagreement? Thanks to Moermann’s activism, the Monetary Authority of Singapore got involved to give its views on resolving conflict in situations where competing REITs are under single control. Mak Yuen Teen, a Singapore business professor, questioned the independence of a director on the Sabana manager’s board, drawing a reply.

“We try to make our criticism as constructive as possible,” says Moermann. “From the point of view of unitholders, this merger is not a necessity at all.”

The pandemic will leave a long shadow on rents and interest rates. This matters for Singapore, where every third dollar changing hands on the local exchange is because of buying or selling in a REIT. With all the uncertainties of the post-Covid economy, the least investors expect is that someone shine a light on their behalf, not just in gleaming storefronts and condominiums, but in gloomy warehouses and factory yards. For now, that job has gone to a foreigner.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2020 Bloomberg L.P.