A Star Franklin Manager Gets Burned in Market He Helped Create

Santosh Kamath’s appetite for high-yield Indian debt helped create the nation’s market for lower-rated corporate bonds.

(Bloomberg) -- Santosh Kamath’s appetite for high-yield Indian debt helped create the nation’s market for lower-rated corporate bonds and turned him into one of the country’s best-known investors.

Now the Franklin Templeton manager’s embrace of risk is backfiring in spectacular fashion.

In a surprise move that rippled through Indian markets on Friday, Franklin Templeton said it would wind up six fixed-income and credit-risk funds overseen by Kamath, freezing $4.1 billion of investor assets. Closing the funds is the “only viable option to preserve value for investors and to enable an orderly and equitable exit,” the asset manager said in a statement.

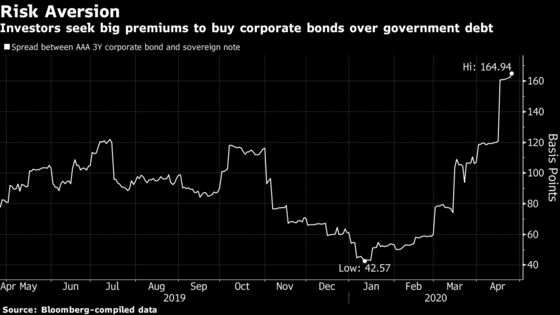

Analysts familiar with Kamath’s investments say the money manager was caught out by his preference for higher-yielding but less liquid debt. As in many credit markets around the world in recent weeks, demand for riskier Indian corporate bonds dried up after the coronavirus pandemic prompted authorities to put the country on lockdown.

“Kamath’s investment strategy is an outlier” in India, said Dhirendra Kumar, chief executive at Value Research Ltd., a mutual fund advisory firm. “His style of investment is aggressive and tends to invest in non-AAA corporate bonds. That did help Franklin pay higher returns to investors for years, but has hit them hard now because the coronavirus pandemic has frozen liquidity in the non-AAA corporate notes.”

Kamath, who’s been with Franklin Templeton since 2006 and is now chief investment officer for fixed-income, is widely acknowledged as having helped build the market for credit rated below AAA in India as a major buyer of those assets.

Almost 88% of Franklin’s India Credit Risk Fund was invested in rupee corporate bonds that were rated AA or below at the end of March, according to a Franklin fact sheet. The Franklin India Low Duration Fund had 64.7% assets in bonds rated below A+, with 40.8% in bonds rated AA and AA-.

Kamath’s bets on lower-rated credit have paid off in the past, helping him outperform peers. Franklin’s India Ultra-Short Bond Fund has delivered a 7.7% annual return over five years, beating 80% of rivals, according to Value Research data. The fund has declined 1.6% so far this year.

Signs of trouble had been brewing for months. In January, Franklin segregated investments of Vodafone Idea Ltd. into separate portfolios to protect value for existing holders in the asset manager’s various funds. Vodafone Idea, already under strain due to a tariff war in the telecom sector in India, has to pay $4 billion in dues it owes to the government.

Franklin Templeton did something similar with its exposure to Yes Bank’s bonds maturing in December 2021 last month after the lender was seized.

Kamath, who didn’t immediately respond to requests to comment on Friday, is far from alone in getting burned as debt markets globally were jolted by the pandemic. At his own firm, the flagship global bond fund run by Michael Hasenstab posted a $4.3 billion decline in assets in the first three months of the year, its worst quarter since 2016. At least 76 European mutual funds with $40 billion in assets suspended redemptions last month, according to Fitch Ratings.

Despite Kamath’s troubles, Morningstar Investment Adviser India Pvt. sounded a note of confidence in the money manager on Friday.

“Our conviction in these funds has stemmed from the experience of Santosh Kamath in the lower credit space, capability of the team in managing credit funds, and robust research infrastructure which has enabled them to shortlist investment worthy companies in the lower credit space for over a decade,” analysts at the company wrote in a report.

Indian debt markets still face significant headwinds. Liquidity levels are low even in good times and they have yet to recover from the collapse of a major infrastructure financier in 2018. The Reserve Bank of India recently moved to provide cheap cash to shadow bankers, but the offerings failed to elicit enough of a response from banks on Thursday.

For Gopikrishnan MS, the former head of foreign exchange, rates and credit for South Asia at Standard Chartered, the lesson for mutual funds is to always hold liquid paper on their books, and especially in times of crisis.

“There should be strict conditions for liquidity of underlying bonds they can invest in,” he said.

©2020 Bloomberg L.P.