A Spectacular 1986 Goal Still Inspires Debate on BOE Policy

A Spectacular 1986 Goal Still Inspires Debate About BOE Policy

(Bloomberg) -- The Bank of England talks so much about negative interest rates that it might avoid having to actually use them.

The institution’s public soul-searching ever since Governor Andrew Bailey first softened his opposition to subzero monetary policy in May is convincing some investors that officials aren’t bluffing about embracing it. Then again, creating that anticipation without enacting the measure could be just what they want.

“They’re flagging it to the market very prominently, but it doesn’t mean that they’ll do it,” said Thomas Costerg, senior economist at Pictet Wealth Management in Geneva. “I’m still not fully convinced they will go there.”

Holding fire would be consistent with the BOE’s long-running wariness about a policy that eats into bank profitability in the neighboring euro zone. A strategy of threatening action without necessarily following through would also be straight out of the playbook of the current chief’s old boss, Mervyn King.

In a speech in 2005 -- 15 years to the week before Bailey’s initial comment in May -- the former governor cited a spectacular goal by Diego Maradona to show how a central bank can reach its aim by simply guiding expectations.

King showcased the Argentinian’s 60-yard (55-meter) dash before scoring against England at the quarter-final of the soccer World Cup in 1986, when the celebrated forward kept plowing ahead, confounding opposition defenders who expected him to swerve along the way.

“Monetary policy works in a similar way,” King declared. “Market interest rates react to what the central bank is expected to do.”

Gertjan Vlieghe -- a member of the current rate-setting panel -- was a junior BOE official at the time, and one of four that the-then governor cited as “effectively co-authors” of the speech.

If policy makers wanted investors to bet on negative rates without actually cutting them that far to keep a lid on the pound at a time of dollar weakness, Maradona tactics could explain the past five-month saga of BOE comments on the matter. The latest remark was on Thursday by Chief Economist Andy Haldane.

“We at the bank are doing work to ensure that the tool is in the toolbox,” he told a conference. “That is not remotely the same as saying that we are about to deploy that tool.”

Twists and Turns |

|---|

| Some of Bailey’s footwork on negative rates |

|

One vulnerability with such an approach, if mishandled, could be future credibility.

“The Maradona effect was used quite successfully in the past, but you have to be careful with this, because it’s the little boy who cries wolf,” Steven Major, global head of fixed income at HSBC Holdings Plc, told Bloomberg Television. “Do it too many times, and no-one’s going to listen.”

Major doesn’t reckon that’s what the BOE is up to. He sees a serious possibility that the central bank will end up following through with its rhetoric and cutting below zero.

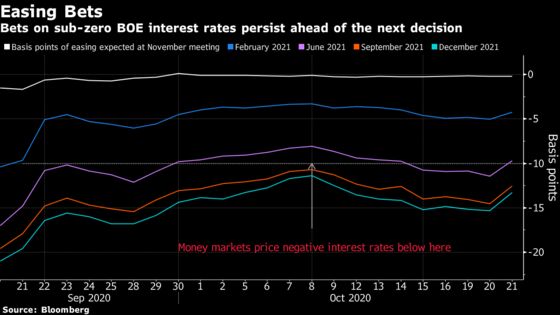

The BOE has also managed to persuade investors that its change of heart on subzero policy isn’t just posturing. Money markets are betting that it will lower interest rates to 0% by June and pricing a further 4 basis points of sub-zero easing by the end of next year.

Even so, it would be no surprise if officials didn’t really want to do that right now, preferring quantitative easing as their primary stimulus tool. Until May, officials had shut down any speculation that they might follow counterparts in Europe and Japan by going negative, citing the harm the policy can inflict on lenders’ margins.

Hand of God

An alternative analysis of the BOE’s ambiguity could be that it simply reflects different communication by a new governor, or varying views among policy makers.

“It seems a bit ill-rehearsed” as a Maradona tactic, said Tony Yates, an economics lecturer and former BOE official who also helped draft the 2005 speech. Yates added that he had misgivings about King’s remarks.

“I never thought that was such a great analogy,” Yates said. The soccer legend “was tricking everybody. Central banks should try to do the opposite, explaining what you’re trying to do in a clear way.”

If the BOE really has been bluffing, then King’s speech might have another apt observation.

The former governor, who now writes columns for Bloomberg Opinion, also referred to Maradona’s more-notorious goal of the match, when officials failed to see he had illegally hit the ball into the net with his hand. The footballer later described the maneuver as “the hand of God,” and Argentina went on to win the tournament.

“He was lucky to get away with it,” King said.

| Read More... |

|

©2020 Bloomberg L.P.