A Peek at the ECB Stimulus Toolkit as Inflation Pessimism Mounts

A Peek at the ECB Stimulus Toolkit as Inflation Pessimism Mounts

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

European Central Bank policy makers are gathering in Lithuania on Wednesday with stimulus on their minds.

President Mario Draghi’s final few months before his term ends are being scarred by plunging inflation expectations as escalating global trade tensions whack confidence and stoke recession fears. Updated economic projections, to be presented by Executive Board newcomer Philip Lane, will signal whether the bloc needs yet another central-bank boost.

When the decision is announced on Thursday, most economists expect officials will have agreed on generous terms for long-term loans to banks. A few analysts believe the euro zone needs something more. Here’s a look at the tools at hand.

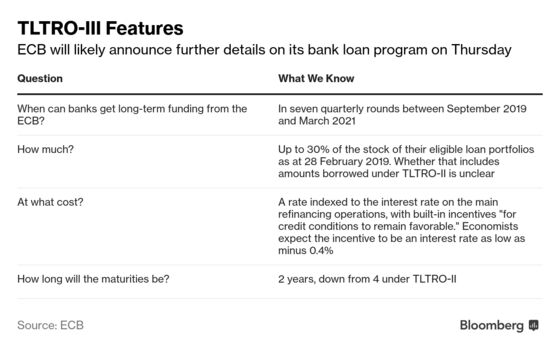

Bank Loans

The ECB has already announced that it’ll revive its so-called TLTRO program of cheap long-term loans to banks, aimed at encouraging them to lend to companies and households. The open question is how generous the terms will be. They could be almost as lavish as the last round, carrying an interest rate as low as minus 0.4% -- lenders would be paid to lend.

Interest-Rate Guidance

Oxford Economics predicts the ECB will turn to a verbal policy tool. The central bank already says it expects interest rates to stay on hold “at least through the end of 2019.” Economist Oliver Rakau said in a note this week that he expects the language will be changed to indicate no hikes until at least the first quarter of 2020. That’s only a slight adjustment, and still out of line with market expectations for a small increase in 2022.

Another option, advocated by Evercore ISI’s Krishna Guha, could be a switch from calendar-based guidance to an inflation threshold -- saying what price-growth criteria would warrant a rate rise. Guha considers this a “wild-card possibility.”

Interest-Rate Cut

Unlike the U.S. Federal Reserve and the Bank of England, the ECB hasn’t started tightening policy. Its key rate, the deposit rate, is at a record-low minus 0.4%. Another cut would draw howls from nations such as Germany, where squeezed retirement income is a political issue, and from banks, which can’t easily pass negative rates on to their customers.

Draghi has promised to review the impact on bank profitability to see if the transmission of monetary policy is being impeded. While his colleagues are unenthusiastic about measures such as exempting some bank deposits from the charge, that could change if another rate cut is deemed necessary.

Quantitative Easing

The central bank bought 2.6 trillion euros ($2.9 trillion) of sovereign debt, covered bonds, corporate bonds and asset-backed securities from 2015 until the end of last year. ABN Amro has made a bold call that it will be restarted in 2020, with 70 billion euros ($79 billion) of bonds a month from January and continue through September.

Resuming QE so soon would be awkward, but the ECB has repeatedly said all options are on the table. There are hurdles though. The central bank has self-imposed limits on how much of any issuer’s debt it can buy -- 33% in most cases -- to avoid crushing the market and becoming a dominant creditor of European governments. It might have to break through those guardrails.

QE Reinvestments

There may be scope to tweak the rules on reinvesting the proceeds of QE bond holdings as they mature. Self-imposed restrictions include reinvesting only in the country where the debt matured, and allowing national central banks to buy only their own government’s sovereign debt. Still, it would be hard to convince investors that the impact of any changes would be significant.

Something New

Draghi has consistently come up with dramatic maneuvers over his eight-year term, from a rate cut at his first meeting through innovations such as the “whatever it takes” pledge during the sovereign debt crisis, negative rates, TLTROs and QE.

If he’s to deliver another surprise with less than five months left in the job, investors need to believe his successor will follow through. That race is wide open, with contenders such as QE-critic Jens Weidmann, QE-architect Benoit Coeure, centrist Francois Villeroy de Galhau and candidates with relatively short central-banking history such as Olli Rehn.

The ECB could also reiterate that it’s done a lot and the impact hasn’t finished feeding through to the real economy. The news isn’t all bad -- unemployment is at the lowest since 2008, supporting nascent wage pressures, and economic confidence might be starting to turn up. U.S. President Donald Trump could even pull back from his protectionist threats.

“There’s an idea in the markets that global central banks are just about to throw in the towel and start cutting rates left, right and center -- the ECB will probably want to tiptoe their way around that,” said Claus Vistesen, chief eurozone economist at Pantheon Macroeconomics. “They’ll probably repeat that the stance is already very accommodative, that generous TLTRO terms support that, and the rest is to watch, wait and stand ready to adjust.”

To contact the reporters on this story: Paul Gordon in Frankfurt at pgordon6@bloomberg.net;Carolynn Look in Frankfurt at clook4@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint, Andrew Atkinson

©2019 Bloomberg L.P.