(Bloomberg Opinion) -- It makes sense for investment banks to cut businesses where they’re too small to be competitive and staying in is costly. So Deutsche Bank AG’s exit from equities trading is overdue. That doesn’t mean life is going to get any easier, in Asia at least.

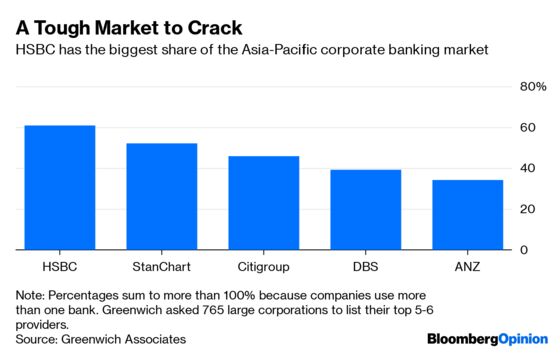

The German lender is counting on its strength in fixed-income and currencies trading to pivot into becoming primarily a corporate bank that serves multinationals’ needs for transactions and cash management. That will put it head to head with the dominant players in Asia: HSBC Holdings Plc, Citigroup Inc. and Standard Chartered Plc. They won’t be an easy nut to crack.

At least this approach has a better chance of succeeding than building up Deutsche Bank’s private-banking business, where leaders UBS Group AG and Credit Suisse AG are trying to beat back the challenge of Chinese and Singaporean firms. No bank has exited the equities business on this scale before, as my colleague Elisa Martinuzzi has noted, and it’s unclear what effect this may have on private-banking customers.

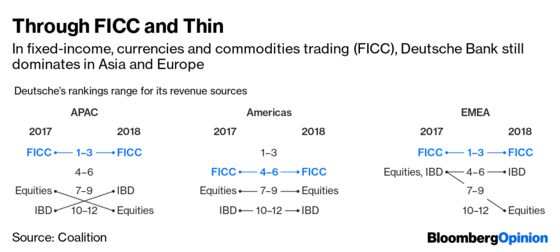

Deutsche Bank’s stronghold in fixed income and currencies will count for something. It was the region's fourth biggest fixed-income bank by revenue last year, according to Coalition Development Ltd., a London-based analytics company. Within that business, the German lender ranked first in credit, which includes trading corporate bonds and structured products, while it was second in foreign exchange. That’s a crucial calling card for any firm that wants to make it as a corporate bank in Asia.

Contrast that with equities trading, where Deutsche Bank ranked 11th by revenue last year, down from sixth in 2015, according to Coalition. In cash equities (which comprises research, sales and trading), it was 10th. Equities increasingly is a business requiring scale, and high salaries for bankers and traders have become harder to support at a time of shrinking commissions and rising automation. Stiffer competition from Indian and Chinese banks has compounded the difficulties.

Job cuts in Asia will fall disproportionately on the Hong Kong operation, which is focused on equities, while Singapore should be more resilient, as the bank’s primary fixed-income hub. The question is whether Deutsche Bank’s edge in bonds and foreign exchange will be enough to attract local corporate customers or U.S. multinationals away from the likes of HSBC and Citigroup.

Deutsche Bank will also need to keep European corporate clients loyal and manage the high technology costs that come with a push into transaction banking. Luckily, transaction banking and cash management is a humdrum business that tends to have sticky clients in the shape of industrial corporations, unlike institutional investors and hedge funds, which are quick to switch banks. The reason the German government was keen on the since-abandoned merger between Deutsche Bank and Commerzbank AG was that it didn’t want local companies to be left without a national bank overseas at a time when Wall Street firms already dominate European banking.

A bigger challenge may be maintaining its heft in fixed income. Morale is far from high, and star traders can be expected to defect as they worry that this restructuring – the bank’s third in four years – won’t be the last. Deutsche Bank plans to cut its 91,000-person workforce by a fifth. At the end of 2018, Asia accounted for 19,700 out of 92,000 global employees, of which more than 10,000 were support staff.

The pressure isn’t going away.

Deutsche Bank largely exited commodities in 2013, prompted by the high capital requirements of the business and low margins.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.