A Greek Tragedy Made in Italy?: European Equity Pre-Market

A Greek Tragedy Made in Italy?: European Equity Pre-Market

(Bloomberg) -- Euro Stoxx 50 futures are down 0.7% despite a strong U.S. session, although not strong enough to break September highs. Italian stocks will keep the center stage after European finance ministers gave a frosty reception to the country’s new budget and the country’s bonds closed the day at their weakest level in more than four years, with the European Commission warning of a Greek-style crisis.

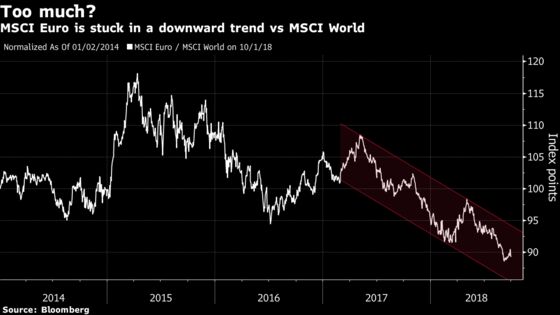

So maybe it’s no surprise that strategists from HSBC and JPMorgan agree that the U.S., and probably the world equity markets, will keep outperforming Europe for the time being. Political noise, sluggish growth and earnings momentum are cited as the main reasons. Nevertheless, looking at the chart below, Europe’s underperformance is still striking and appeals to contrarian traders considering that risks are on the upside.

What about the U.K.? The typically inverse correlation between the pound and the FTSE has not been working well in 3Q. Like JPMorgan strategists pointed out, the U.K. is a defensive, high-dividend yielding market and it may have further problems with bond yields rising. In case of a decent Brexit deal, a stronger GBP would probably limit the upside on U.K. equities, while further political uncertainty would likely weigh on both the market and the currency, the same way it has over the past few months.

Also in the U.K. today: house builders will be in focus as investors look towards Nationwide House price data and construction PMI.

Elsewhere, the optimism from the U.S. session failed to transfer over to Asian markets, as the weak Chinese PMI caught with the Hang Seng, sending it sharply down after a public holiday, while other markets are mixed. Oil is steady near four-year highs, while base metals are weaker, and the dollar is almost back to its September high.

Finally, European insurers outperformed all other industries in Europe in the third quarter and deal activity only partly explains the reasons. It seems they kept their appeal to asset managers because they are not banks.

COMMENT:

- “Credit has been resilient so far and even European equity volatility did not react much to the pick-up in political risk -- short-maturities of Euro Stoxx 50 implied vol have been range bound since May,” Goldman Sachs strategists write in a note about the Italian political crisis. “While our economists do not expect systemic implications for the global economy, contagion risks have risen. We think European risky assets remain vulnerable and there is potential for negative spillovers to the euro area given the high trade exposure to Italy.”

NOTES FROM THE SELL SIDE:

- Morgan Stanley is cutting Danske Bank to equalweight, as the troubled Danish bank has failed to bring some clarity and narrow down the penalty risk outcome options in the Estonian AML investigation. The target price is also cut to DKK203.

- Credit Agricole is appealing, Morgan Stanley says in a note upgrading stock to overweight from equal-weight. The bank sees ~30% upside to its new EU16.40 price target and adds the stock to preferred European banks list.

- European airport operator valuations look pricey and the travel retail business could provide more downside for the sector, according to RBC. With passenger growth decelerating, regulated tariffs are limiting pricing power for operators. Flughafen Zurich (outperform) is the only airport stock RBC would own at this point.

COMPANY NEWS AND M&A:

- Akzo Nobel plans to distribute another 5.5 billion euros to shareholders from the sale of its specialty-chemicals business, rewarding investors for a plan that the paint company used to fend off an unwanted takeover approach.

- Italian stocks will remain keenly in focus on Tuesday after European finance ministers gave a frosty reception to the country’s new budget and the country’s bonds closing the day at the weakest level in more than four years.

- Ghosn Sees No Need to Expand Renault’s 3-Partner Alliance: Echos

- Veolia to Sell 30% Transdev Stake to Rethmann for EU340m

- Round Hill to Sell Dutch Rental Homes for About EU1.4B: FD

- Shell Gives Green Light to Invest in LNG Canada

- Bakkafrost 3Q Salmon Harvest Volume Reached 7,200 Metric Tons

- BMW CFO Says Preparing for Hard, Complicated Brexit: Sky

- Natixis Eyes Stakes in Boutique Investment Banks: FT

- Thyssenkrupp Will Probably Exit DAX, CEO Kerkhoff Tells WAZ

- German Govt Coalition Reaches Car Emission, Energy Agreement

- Huhtamaki Sees EU30m Cost From Actions to Raise Profitability

- La Poste Wants to Buy SocGen Stake in Consumer Credit JV: Echos

- EU Parliament Asks Danske Whistle-Blower to Testify, Ritzau Says

- Citigroup’s Investor Guide for No-Deal Brexit, or a Corbyn Upset

- Victrex Races to Get Its Lightweight Plastic in Electric Cars

- Meggitt Gets $323M Contract From U.S. Defense Logistics Agency

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 384.2 (200-DMA); 392.7 (July high)

- Support at 383.7 (50-DMA); 379.9 (23.6% Fibo)

- RSI: 54.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,416 (50-DMA); 3,462 (200-DMA)

- Support at 3,315 (38.2% Fibo); 3,274 (Sept. low)

- RSI: 53.9

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Credit Agricole raised to overweight at Morgan Stanley

- Metso upgraded to overweight at JPMorgan; PT 34.50 Euros

- Nestle upgraded to buy at Jefferies

DOWNGRADES:

- Atlas Mara downgraded to hold at Renaissance Capital; PT $2.60

- Danske Bank cut to equal-weight at Morgan Stanley; PT 203 Kroner

- FLSmidth downgraded to neutral at JPMorgan; PT 430 Kroner

- Learning Technologies Group downgraded to add at Peel Hunt

- Royal Mail downgraded to underweight at JPMorgan; PT 3.41 Pounds

- Siemens downgraded to hold at HSBC; PT 123 Euros

- Unilever GDRs downgraded to hold at Jefferies

INITIATIONS:

- Fiat Chrysler rated new peer perform at Wolfe; PT 16 Euros

- Kitron rated new buy at SpareBank; PT 11.50 Kroner

- LondonMetric rated new overweight at Barclays; PT 2 Pounds

- Tritax Big Box rated new equal-weight at Barclays

MARKETS:

- MSCI Asia Pacific down 0.2%, Nikkei 225 little changed

- S&P 500 up 0.4%, Dow up 0.7%, Nasdaq down 0.1%

- Euro down 0.33% at $1.154

- Dollar Index up 0.16% at 95.45

- Yen up 0.11% at 113.8

- Brent up 0.1% at $85/bbl, WTI up 0.4% to $75.6/bbl

- LME 3m Copper down 0.9% at $6193.5/MT

- Gold spot up 0.3% at $1192/oz

- US 10Yr yield down 1bp at 3.07%

MAIN MACRO DATA all times CET:

- 9am: (SP) Sept. Unemployment MoM Net (’000s), est. 28.1, prior 47

- 10:30am: (UK) Sept. Markit/CIPS UK Construction PMI, est. 52.9, prior 52.9

- 11am: (EC) Aug. PPI MoM, est. 0.2%, prior 0.4%

- 11am: (EC) Aug. PPI YoY, est. 3.8%, prior 4.0%

- 4pm: (DE) Sept. Change in Currency Reserves, est. 0, prior -200m

- 4pm: (DE) Sept. Foreign Reserves, est. 467, prior 467.9

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2018 Bloomberg L.P.