Corner of Bond Market Defies Virus to Cling to Reflation Bet

A Corner of the Bond Market Defies Virus to Cling to Growth Bet

(Bloomberg) -- It has hammered raw material prices, derailed activity for tens of millions and stopped the world’s second-biggest economy in its tracks. But for optimists in one corner of the fixed-income community, the coronavirus isn’t disrupting bets for a brighter economic outlook in the months ahead.

BlackRock Inc., Nordea Bank and wealth manager Arbuthnot Latham & Co. Ltd. are among names citing everything from central bank support to the enduring health of the global labor market to reaffirm their call that markets are under-pricing the chance of a rebound in inflation. That’s even as the extent of virus damage remains unknown.

Just weeks ago their view was looking prescient as the trade war eased and economic indicators showed signs of life. Now it faces a new test from an illness that’s killed more than 1,300 and infected almost 60,000.

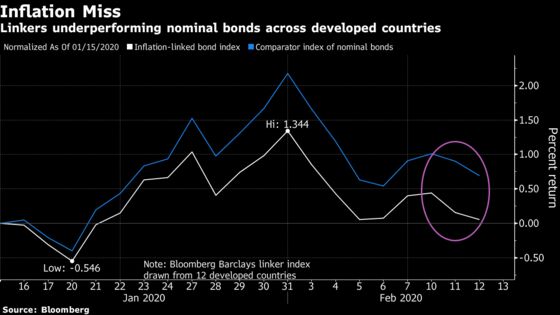

Factors like a double-digit drop in the oil price over the past month already have the market recalibrating price expectations. A Bloomberg gauge of $3.3 trillion inflation-linked bonds from developed nations has significantly lagged a measure of comparable nominal notes in recent weeks.

For Andreas Steno Larsen, that’s merely setting the scene for an even bigger turnaround.

“I would be patiently looking to bet on higher inflation, probably via inflation swaps, once we get past the peak negativity in April,” said the Nordea strategist. “It’s clear from the communication from China that they really want us to trust that the worst part of this is already behind us, and the market is softly buying into it.”

Fed Alert

Quantifying the effect on inflation of a viral outbreak like the one spreading from China is a challenging task.

On the one hand, supply disruptions and stockpiling can stoke consumer price growth, as demonstrated by a surge in China’s January reading. On the other, slumping input costs can drive down producer prices and widespread disruption can hit overall spending and investment.

Goldman Sachs Group Inc., UBS Group AG and Macquarie Group Ltd. are among a slew of major names cutting their growth forecasts for China. The Federal Reserve has made clear it is alert to the danger of a spillover effect, even as Chinese President Xi Jinping moves to reassure the world that the Asian nation will meet its economic goals.

Bonds in the developed world are certainly signaling concern. A key slice of the U.S. yield curve inverted two weeks ago for the first time in months, a sign of near-term fear and mounting doubt among investors that policy makers in the world’s largest economy will succeed in reviving inflation.

Nonetheless, the optimists see a market that’s too gloomy on the macro outlook.

BlackRock is maintaining a bullish call on inflation-protected Treasuries, known as TIPS. Alongside investment heavyweights such as Pacific Investment Management Co. and State Street Corp., the firm has long argued inflation risks are under-estimated by the market in general.

Expectations as proxied by five-year, five-year forward inflation swaps have been stuck in a range for months in both the U.S. and euro region, with those in Europe not far from a record low. Another bond market gauge of expectations, the U.S. 10-year breakeven rate, was showing signs of life at the end of 2019. It’s down about 10 basis points this year to 1.65%, below both its one- and five-year averages.

It’s all understandable given that even policy makers are hinting at doubts about reaching their goals. With core PCE inflation below the median Fed projection for 2020, the central bank’s January statement said its policy stance was appropriate to get inflation “returning to” the 2% target, rather than “near” that pace. Data Thursday showed a key measure of U.S. consumer prices remained subdued last month.

‘Corona Contagion’

The outlook is mixed, however. A Chinese gauge of inflation is surging partly for seasonal reasons and partly as a result of the virus, which has curtailed supplies and stoked demand for certain products. The country’s key role in the supply chain could also mean its domestic disruption pushes up prices globally.

Mark Nash, head of fixed income at Merian Global Investors, says the growth shock from the coronavirus may turn out to be worse than the market is pricing because the Chinese economy was already weak. But he thinks that impact could prompt the Fed to cut rates, so he’s staying neutral on inflation bonds rather than outright bearish.

Robeco has also stopped short of going underweight inflation bonds for a similar reason, though its logic is rooted as much in the American business cycle as that of China.

“The U.S. economy is facing a late cycle risk, evident in the yield curve,” said Jamie Stuttard, co-head of global macro fixed income at the firm. “There’s a scenario that the Fed may have to take rates down to zero over the next couple of years. The market is probably right to think about increased probability of a Fed rate cut this year with the shock coming from the coronavirus part of the backdrop.”

Morgan Stanley is neutral on TIPS and breakevens. In a note it said it doesn’t see demand-driven pressures in the U.S. economy, nor does it project higher import prices spurred by the virus.

For now, American growth looks relatively robust. Data released last week showed employers added a better-than-expected 225,000 new jobs in January. Personal income growth remains well above headline inflation, even as it moderates.

That has Gregory Perdon, the co-chief investment officer at Arbuthnot Latham, choosing to look through the virus noise and focus instead on wage growth and the dovish stance of central banks. Perdon said he expects a V-shape recovery and is looking to allocate capital to pro-inflation assets once there’s a sign the outbreak has peaked.

“The ingredients you need for the greenshoots in the inflation landscape are actually there, but the corona contagion has thrown a wrench in the spokes,” said Perdon. “Once the contagion starts to withdraw, there won’t be a lot of reasons why inflation-related assets can’t deliver attractive returns.”

--With assistance from Todd White and Laura Cooper.

To contact the reporter on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma

©2020 Bloomberg L.P.