A Century of Bond History and Acumen Sees Even Lower U.S. Yields

A Century of Bond History and Acumen Sees Even Lower U.S. Yields

(Bloomberg) -- Economist John Maynard Keynes famously said that markets can stay irrational longer than you or I can stay solvent. Yet for Hoisington Investment Management, sticking with what seemed irrational to many -- that Treasury yields were going lower -- has proved a winning wager.

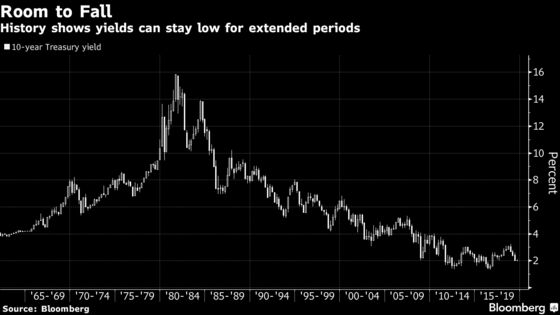

Van Hoisington and his chief economist, Lacy Hunt, didn’t waver in their decades-long view when their fund lost money in 2018 as yields rose, and they remain resolute that long-term rates are headed lower. They may take comfort in research from Capital Group’s Margaret Steinbach that uses data back to the 1870s to show 10-year Treasury yields can stay low for decades.

For Hoisington and Hunt, the ever-growing overhang of U.S. private and government debt will weigh on economic growth, which is already under pressure after the Federal Reserve tightened policy from 2015 through last year. They see Fed money-supply restraint more than canceling out fiscal stimulus from the U.S. administration.

“There are many measurements that suggest that the economy is slowing much more rapidly than general conversation suggests,” said Hoisington, who started the firm in 1980 and hired Hunt 16 years later. “The Fed is behind the curve and that would suggest that the funds rate is going to fall by 150 to 200 basis points in the next 12 months. We’ll probably take out the lows across the yield curve before this cycle is over.’’

The 10-year Treasury yield set an all-time low of 1.32% in July 2016, before rising to a seven-year high of 3.26% in October 2018. It traded at about 2.1% on Wednesday, and has averaged 6.12% since 1962, when Bloomberg data for the maturity begin.

Powell Signals

Investors are looking for fresh signals on monetary policy on Wednesday, first from Fed Chairman Jerome Powell and then through the minutes of last month’s rate-setting meeting. Economists expect the Fed chief will leave rate cuts firmly on the table when he testifies to Congress on Wednesday and Thursday.

Traders are pricing in a quarter-point of easing this month and a total of about 60 basis points of cuts for all of 2019.

“If easier policy on the part of the Fed results in stronger growth and stronger inflation expectations, I’m still not convinced that yields could rise super-meaningfully,” said Capital Group’s Steinbach, a fixed-income investment specialist. “Europe is so weak and China is slowing. Trade with China is also a big question mark.”

President Donald Trump and Chinese President Xi Jinping agreed last month to re-start trade talks and suspend new tariffs. Treasury Secretary Steven Mnuchin and U.S. Trade Representative Robert Lighthizer may head to to China “shortly,” according to White House aide Kellyanne Conway.

‘Headed Lower’

Any spike higher in yields -- as seen Friday after stronger-than-expected U.S. jobs data -- is just a short-term blip, in the eyes of Hunt and Hoisington.

“We try to keep our focus on these long-term secular forces,” Hunt said. “It’s hard to do because there is always a feeling that the latest data point has created a new trend. Yields are headed lower, and the about 22-year duration of our portfolio speaks for itself regarding our views.”

Not once since 1990 has the firm wavered on bets that yields would head lower. The fund’s holdings as of March 31 consisted mainly of Treasuries that come due from 2040 to 2048. That included standard Treasuries as well as zero-coupon debt created by dealers who break the cash flows into two different securities and sell them separately. Zero coupons have a higher duration than standard Treasuries, meaning they deliver bigger price gains as yields fall.

Key Equation

For Hunt, the key to understanding the bond market lies in the Fisher Equation, which says the long-run Treasury yield is equal to the real rate plus the expected rate of inflation. Hunt says those two variables are headed lower.

The Wasatch-Hoisington U.S. Treasury Fund has returned 12.6% this year, beating 99% of its peers, according to data compiled by Bloomberg. It has a similar outperformance on a five-year basis, though it took a hit last year -- dropping 3.8% and trailing its rivals as long-term yields climbed.

Adding to forces that point to even lower long-term yields is the record low level of term premium -- the extra compensation investors typically demand to hold longer-term Treasuries rather than rolling over short-dated obligations.

Capital Group, which manages $1.6 trillion through its American Funds, has turned more defensive in the face of the global risks they see building.

“We as investors need to get used to lower yields, globally,” Steinbach said. “When you look back at a 100- to 150-year yield chart, it shows that the higher rates in the 1970s and 1980s were the anomaly. Ten-year yields can actually stay low for a very long time.”

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Dave Liedtka

©2019 Bloomberg L.P.