Markets Will Dictate Timing of U.S.-China Trade Truce

Markets Will Dictate Timing of U.S.-China Trade Truce

(Bloomberg Opinion) -- The impasse in the U.S-China trade talks underscores a stark reality of the post-crisis era, which is that every major public policy decision is subject to a veto by the global financial markets. Markets have the ability to speed up, slow down, kill off or encourage deals that negotiators think they oversee. U.S. and Chinese trade negotiators will spin their wheels on more “constructive” talks and further scheduled meetings, accomplishing little until markets “motivate” them to reach a deal.

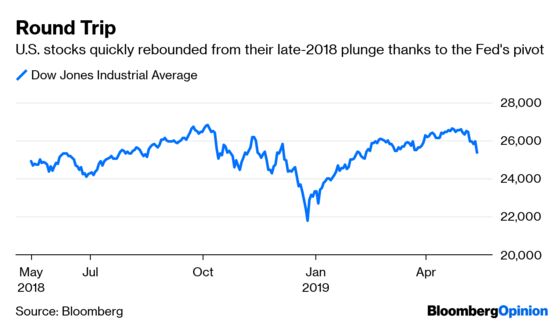

Think of what happened in the fourth quarter when the financial markets used their “veto” over monetary policy. As Federal Reserve officials talked more and more about raising interest rates and reducing central bank’s balance sheet assets, markets grew more and more uncomfortable. But the message from markets went unheeded until Fed Chairman Jerome Powell’s Dec. 19 press conference, where he detailed the central bank’s intention to reduce the balance sheet by $600 billion in 2019 and hike rates at least two times. The markets rioted, with the Dow Jones Industrial Average plunging some 600 points in a matter of hours. By Christmas, U.S. stocks were down 20 percent from their late September peaks, the largest correction in the post-crisis era.

The Fed finally got the message. Powell said on Jan. 4 that the central bank would instead be “patient and flexible” in what has become known as the Fed pivot. The Dow Jones shot up 900 points that day. U.S. stocks went on to set an all-time high in early May, seven months after its September peak. This was the fastest time from new high, down 20 percent, to another new high in history.

Many argue that the market was oversold at the late December low. That’s unlikely. The market declined as much as was needed to get the Fed to abandon its hawkish stance. Once the markets got what they wanted, they roared back to new highs.

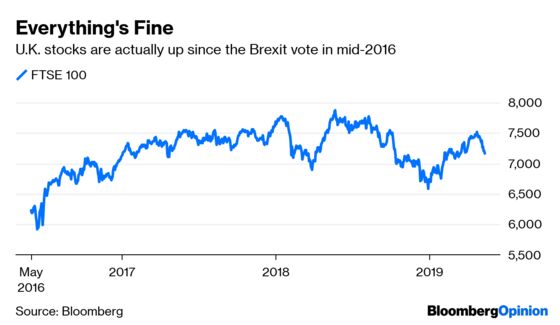

What happens when markets do not express an opinion? A good example is the U.K. and its futile efforts to leave the European Union in what is known as Brexit. The U.K. has descended into an endless, mind-numbing debate that has accomplished nothing, but U.K. shares have not exercised an opinion, with the benchmark FTSE 100 largely drifting since the vote in late June 2016 to leave the EU. So Brexit talks go on with no sense of urgency to conclude. Part of the reason markets are not opinionated about Brexit is they are fine with the status quo. If, or when, a real Brexit deal looks possible, we suspect markets will make their opinion known and they will either ratify the deal or kill it off.

For now, the U.S.-China trade talks are becoming the U.S. version of Brexit. They will go on and accomplish nothing. Although China announced on Monday that it will increase tariffs imposed on about $60 billion of U.S. goods in retaliation for the Trump administration’s latest escalation of the trade war, the Chinese signaled over the weekend that they are fine with nothing happening.

In a wide-ranging interview with Chinese media after talks in Washington ended Friday, Vice Premier Liu He said that in order to reach an agreement the U.S. must remove all extra tariffs, set targets for Chinese purchases of goods in line with real demand, and ensure that the text of the deal is “balanced” to ensure the “dignity” of both nations.

Markets will eventually signal to both sides that the status quo is not acceptable and force them to make a deal. But doesn’t everyone understand this? Apparently, the Fed does not. As Bloomberg Opinion columnist Mohamed El-Erian wrote earlier this month:

[T]he Fed needs to develop a better understanding of market technicals — or what some call a “feel” for the markets. Without that, an important part of its policy arsenal — that is, policy guidance which ensures that markets do some, if not all of the heavy lifting — will become less effective.

Do the Chinese know this? Many will say yes, but that’s doubtful after reading a report in The Wall Street Journal on Thursday noting that a primary reason why the Chinese thought they could back away from previous agreed upon details was they believed they had Trump in a tight spot. In particular, these people said, Mr. Trump’s hectoring of Powell to cut interest rates was seen in Beijing as evidence that the president thought the U.S. economy was more fragile than he claimed. If this is accurate it is a stunning misread of the situation, to the point of showing a lack of basic understanding of Western markets and politics.

In 1968, an unidentified American military officer in Vietnam famously said it became necessary to destroy a town to save it. So how much lower do financial markets have to decline to get a trade deal — a few percentage points, or something akin to a repeat of December’s plunge? One thing seems sure: A rally to new highs will not get a deal done.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jim Bianco is the President and founder of Bianco Research, a provider of data-driven insights into the global economy and financial markets. He may have a stake in the areas he writes about.

©2019 Bloomberg L.P.