Kashkari Says Worker Bargaining Power Should Inform Fed's Stance

He suggested faster wage growth and low unemployment may not be putting much upward pressure on inflation.

(Bloomberg) -- Federal Reserve officials are speaking out about rising inequality and the harm it does the U.S. economy, but most still hesitate to say monetary policy can do much to help.

Neel Kashkari is starting to sound like an exception. Since becoming president of the Minneapolis Fed in 2016, he’s been a consistent dove, arguing for keeping interest rates lower as the labor market heals.

In an interview on Friday, Kashkari said the Fed “has a very powerful role to play,” and that policy makers should take income distribution into account when assessing if they’ve achieved their goal of maximum employment.

Kashkari’s break from Fed tradition on inequality adds to the case for keeping interest rates low. He suggested faster wage growth and low unemployment may not be putting much upward pressure on inflation because workers have lost a lot of their bargaining power in recent decades, echoing a point Fed Vice Chairman Richard Clarida has made.

Other Fed officials are also paying more attention to rising inequality, which was an oft-cited factor behind Donald Trump’s 2016 presidential victory and is now shaping the 2020 election debate as well.

New York Fed President John Williams and Governor Lael Brainard both spoke about it Friday.

Williams told an audience in the Bronx that widening inequality “is undermining, I believe, much of what makes our country great in terms of economics,” while Brainard, speaking in Washington, said a decades-long decline in the portion of national income going to wage-earners “goes to the heart of the rising inequality of wealth and the unequal sharing of prosperity.”

Both, however, were careful to point to other parts of government for solutions. Williams said he doesn’t think the Fed, “by moving interest rates, is going to affect that very much,” while Brainard said “monetary policy aims to influence employment and inflation over the business cycle, as opposed to addressing these longer-run structural changes.”

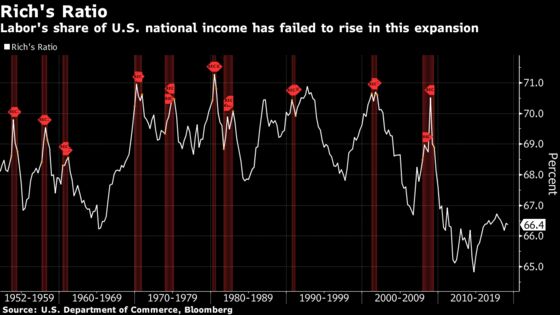

Wealth in the U.S. has become increasingly concentrated in the hands of the richest households in recent decades.

Fed data show the share of the top 1% of the wealth distribution increased to nearly 32% in 2018 from 23% in 1989. And a measure of labor’s share of income developed by Clarida has yet to rise much from the historic lows that have prevailed during the current expansion.

Kashkari said the decades-long slide in labor’s share of income -- and corresponding rise in corporate profit margins -- may help explain the puzzling lack of inflation despite rising wages.

It’s an idea that Clarida, who joined the Fed in September, has explored in recent years. His first big initiative on the job has been to organize a series of “Fed Listens” events hosted around the country. The goal is to gather input from the community that could help strengthen the central bank’s existing policy framework.

At one such event -- at the Minneapolis Fed in April -- Clarida, sitting next to Kashkari in the audience during a presentation on the distributional impacts of monetary policy, suggested to the panelists that in recent U.S. economic expansions, “you did see this late-cycle increase in labor’s share, but it didn’t really translate into price inflation, because profits took a hit.”

In other words, companies may be making so much money that they’re more prepared to give more of it to workers as tighter labor markets lead to faster wage growth, rather than offset the higher labor costs with higher prices. If so, that would have important implications for the Fed’s policy strategy.

For decades, the strategy has been to raise or reduce interest rates in a bid to keep the unemployment rate near a certain estimated “natural” level corresponding to full employment, which in turn is thought to stabilize inflation. But a dramatic shift in the distribution of income and wealth in recent years may have undercut its relevance.

“It’s something we talk about a lot here as we’re deliberating on the outlook for inflation,” Kashkari said. “My economists are very quick to point out that analysis is assuming a static view of labor’s share.”

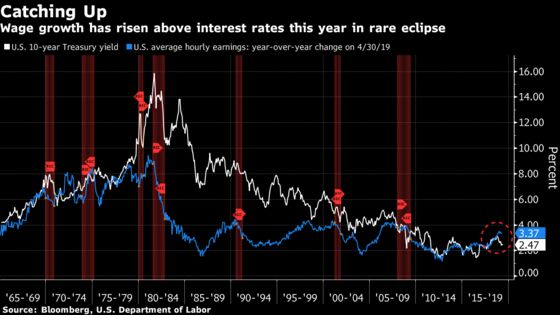

Growth in average hourly earnings has accelerated to about 3.4% on average so far in 2019, versus about 2.9% on average in 2018. Meanwhile, a measure of underlying price pressures Fed officials watch closely moderated to 1.6% in March from about 2% -- the Fed’s official target number -- in December.

Between 2015 and 2018, Fed officials raised rates from near zero to just under 2.5%. Throughout the current expansion, longer-term rates have mostly tracked wage growth, due in part to investors’ perceptions that Fed officials, watching the job market improve, would respond with rate hikes to ward off inflationary pressures.

More recently, longer-term rates have come down as Fed officials scaled back plans for additional hikes, despite accelerating wage growth. Passing concerns about global growth in late 2018, along with receding inflation since then, have outweighed a strengthening job market.

Kashkari said he’ll be keeping an eye on the labor share data going forward to assess whether wage growth can continue to rise without putting upward pressure on price inflation.

“If businesses are really struggling to find workers, a natural conclusion of that should be that workers have relatively more bargaining power than they had in the past,” Kashkari said. “It’s not unreasonable to then think that would have some effect, and workers as a whole would capture a larger share of income than they have been in recent years.”

To contact the reporter on this story: Matthew Boesler in New York at mboesler1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Ros Krasny

©2019 Bloomberg L.P.