Inflation Slowdown Is Again Stalking Sweden's Central Bank

Inflation Slowdown Is Again Stalking Sweden's Central Bank

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

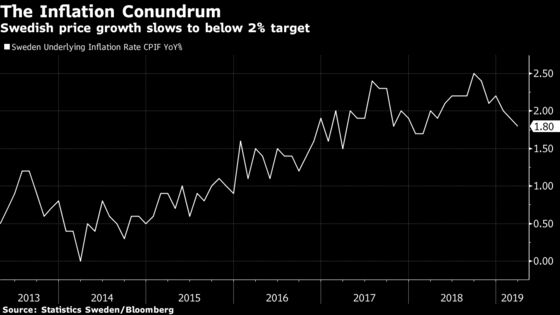

Central banks across the world are grappling with the mystery of how to bring back inflation and there are few places where the struggle has been as profound as in Sweden.

This week, policy makers in Stockholm are meeting as price growth has slipped far below their estimates and their 2 percent target. Just a few months ago, they raised rates for the first time in seven years, plotting a path out of negative rates this year amid growing confidence they had managed to restore credibility in their inflation regime.

But on Thursday they will likely be forced to again lower their rate outlook, potentially pushing back an increase signaled for September and prolonging an era of negative rates. Led by Governor Stefan Ingves, the bank is also expected to extend its bond purchases (by pre-reinvesting bond maturities) beyond June, while keeping the benchmark at minus 0.25 percent.

Inflation pressure has “definitely been lower than the Riksbank counted on” said Torbjorn Isaksson, chief analyst at Nordea Bank Abp. “There are fewer and fewer economic arguments for the Riksbank to raise rates.”

As global and European growth loses momentum, Sweden’s economy is cooling and unemployment is forecast to rise. A global reassessment of monetary policy, led by the Federal Reserve halting its hiking cycle, is weighing on the Riksbank’s plans to tighten. The European Central Bank is planning more stimulus as it expects its key rate to be unchanged at least through 2019.

Nevertheless, policy makers in Sweden have a lot invested in their exit out of so many years of negative rates and they surprised markets in February by sticking to their plans. The krona has tumbled this year, giving the Riksbank more room to raise rates. Some on the board, including Deputy Governors Cecilia Skingsley and Martin Floden, have also flagged that they are willing to live with inflation that holds just below the target, as long as expectations stay anchored around 2 percent.

According to SEB AB, the main scenario is that the rate path will indicate a slightly later hike but that the Riksbank will maintain that an increase will come “during the second half of the year.”

But unemployment surprised negatively in March and the number of jobless seems to have bottomed, according to Svenska Handelsbanken AB’s Chief Economist Christina Nyman.

“Unless there’s considerable inflation pressure, it’s going to be a challenge if you are at about to raise rates and you at the same time have rising unemployment numbers,” she said.

QE Extended

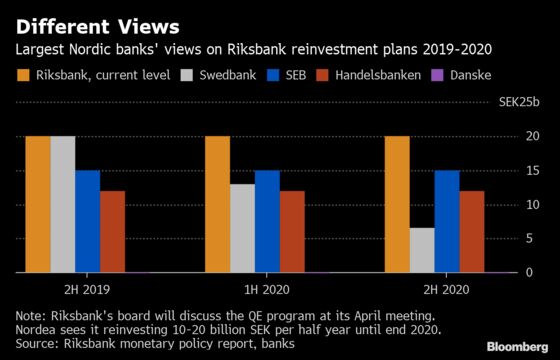

Policy makers have also said they will provide the next step forward on what to do with their bond purchasing program. Opinion is divided, but the main outcome could be continued purchases at a slower pace than the recent 20 billion kronor per year.

Here’s what the economists say:

| Danske Bank The inflation forecast will be lowered, but the Riksbank will probably hold off on adjusting the rate path and continue to signal an increase in the autumn, said Stefan Mellin. But it will stop reinvestments since the bond portfolio would otherwise become too large as a share of total government bonds. |

| Swedbank: The rate path will be lowered, indicating about 1 1/2 hikes a year rather than the 2 a year signaled now, according to Cathrine Danin. Bond reinvestments will continue, but will be phased out gradually. The bank will reinvest about 50 percent of the 40 billion kronor in bonds that mature by the end of 2020. |

| SEB: The rate path will be lowered slightly while reinvestments will be lowered to 15 billion kronor per half year, economist Olle Holmgren said. That means that the share of bonds that the central bank owns would remain around the current level in terms of total share of the stock. |

| Handelsbanken: The rate path will see a marginal revision to indicate a slightly later increase and the pace of bond reinvestments is expected to be lowered to 12 billion kronor per half year. As the situation is uncertain, there’s no reason for the Riksbank to commit to exactly how much to reinvest, but they will probably want to find a plan that doesn’t disturb the market presence too much, while leaving room for a slightly decreasing balance sheet. |

| Nordea: The indicated next rate hike will be moved forward one meeting, still indicating a rate hike during the second half of the year. Reinvestments will be between 10 and 20 billion per half year in the second half of 2019 and in 2020. Nordea believes that the next hike won’t come until mid-2020 and that there’s a risk that it’s delayed even further. |

--With assistance from Harumi Ichikura.

To contact the reporter on this story: Amanda Billner in Stockholm at abillner@bloomberg.net

To contact the editor responsible for this story: Jonas Bergman at jbergman@bloomberg.net

©2019 Bloomberg L.P.