Why This Woman Is Trump’s Latest Pick for the Fed

It’s a timely choice as some credit markets are showing signs of aggressive risk-taking.

(Bloomberg) -- The White House’s latest pick for the Federal Reserve Board was deliberately chosen for her financial stability expertise and knowledge of the Fed system to round out a board of monetary policy experts and Wall-Street savvy lawyers.

President Donald Trump plans to nominate Nellie Liang, a Ph.D. economist who ran the Fed’s financial stability unit until her retirement last year. It’s a timely choice as some credit markets are showing signs of aggressive risk-taking.

Liang’s long study of that topic was a key factor in the winning the nod, according to a person familiar with the matter. The news of her intended nomination broke Sept. 20.

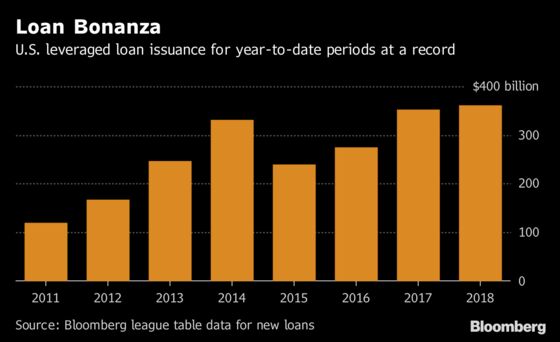

Financial conditions are heating up with some credit markets showing signs of overheating. The Fed’s gradual pace of interest rate increases, combined with low interest rates globally, has supported a reach for yield that has weakened standards among some lenders.

The market for leveraged loans, a higher-risk type of corporate lending, now tops $1 trillion, for example. With the last two recessions triggered by financial bubbles, the Trump administration saw Liang as the missing piece the Fed needed.

“She is calm, analytical, and reasoned, which is exactly what you would want in a regulator, should another crisis hit,” said Kevin Hassett, chairman of the White House Council of Economic Advisers, who didn’t oversee the research on Liang’s selection.

Crisis Fighter

The administration wanted somebody with direct experience in financial crises and knowledge of the inside workings of the Fed. Liang checked both boxes. She has an extensive research record on financial stability and risk monitoring. When the Fed stood up a new division to oversee financial stability, she was its first chief.

Liang respects the discipline of the market, which can punish investors for taking miscalculated risks. For her to support federal intervention in an institution, “it would have to be unequivocally systemic,” said her former colleague Seth Carpenter, who is now chief U.S. economist at UBS Securities in New York.

That should appeal to senators from both parties who will vote on her confirmation.

“The smartest of the big banks that I work with want someone who knows the issues and with whom they can work,” said Karen Shaw Petrou, managing partner at Federal Financial Analytics in Washington. “She really understands how complicated these issues are.”

If confirmed, Liang would step into the middle of a Fed financial stability debate.

Capital Buffers

At least four officials are calling for an increase in bank capital to build a buffer should markets break down, with Boston Fed President Eric Rosengren among the most vocal. Liang has pointed to the stabilizing potential of such a counter-cyclical capital cushion.

A few officials have made the case that the current pace of tightening needs to continue to avert a build up of financial risk. Liang’s research record suggests she might be willing to raise interest rates to cool down markets.

“The economy is doing quite well, and I can very easily imagine she is going to be a hawkish voice because that is what she sees credit conditions dictating,” said Stephen Stanley, chief economist at Amherst Pierpont Securities LLC in New York.

In 2016, Liang co-wrote in a paper that regulatory, or so-called macro-prudential policies, only affect a limited set of financial institutions due to shadow banking, have limited international reach, and can take too long to put in place.

‘Extremely Costly’

“Monetary policy, on the other hand, impacts funding conditions for all intermediaries, more immediately, and has some global reach,” according to the paper. “While these arguments may lead to a conclusion that is uncomfortable because of the higher burden on monetary policy, cleaning up after the bust has proven in the long wake of the Great Financial Crisis to be extremely costly.”

Liang’s resume lists at least nine papers or book chapters related to financial stability published between 2010 and 2016. She has supported Treasury Department proposals for community bank regulatory relief, though she’s leaned against changes that would reduce capital requirements for the largest and most complex firms.

She’s also been a strident defender of robust stress tests, saying fiscal policy has “much less space” now to help cushion a downturn and authorities have less firepower to put the financial system back on its feet than they had pre-crisis, making prevention crucial.

In her time as head of the Board’s financial stability office, Liang reported to Board vice chairs, not Daniel Tarullo, the former governor who oversaw the implementation of sweeping post-crisis bank reform. That distinction could matter for Republicans worried that she would share his regulatory views.

If the Trump administration has all of its nominees confirmed, she would be the fourth Ph.D. on the seven-person Fed Board: Vice Chairman Richard Clarida and Marvin Goodfriend, who is awaiting a Senate confirmation vote, both have doctorates. So does Governor Lael Brainard, an Obama administration appointee.

Chairman Jerome Powell and Vice Chairman of Supervision Randal Quarles are lawyers with business and management experience. Kansas banking commissioner Michelle Bowman, herself a lawyer, would bring community banking perspective to the board. She is also waiting for a confirmation vote.

--With assistance from Robert Schmidt.

To contact the reporters on this story: Craig Torres in Washington at ctorres3@bloomberg.net;Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.