Fed's Powell Has Several Options for Tweaking Communications

Fed's Powell Has Several Options for Tweaking Communications

(Bloomberg) -- Jerome Powell has already put his own stamp on Federal Reserve communications. If he wants to shake things up a little more, he’s got a number of options.

Since becoming chairman in February he’s trimmed the Fed’s all-important policy statement, declared a preference for “plain English” over the language of Ph.D. economics and doubled the number of his post-meeting press conferences starting next year.

Ways to further overhaul how the Fed gets its message out to the public could include adjusting the package of economic forecasts that Fed policy makers submit each quarter. The exercise has its critics, including Powell, who’s publicly thrown cold water over the value of its long-term projections.

Economists caution that changes carry potential pitfalls and are skeptical Powell would run those risks. The Fed’s policymaking panel, which meets next week in Washington, has a communications subcommittee tasked with keeping such matters under review. Here are some of the things that it could consider:

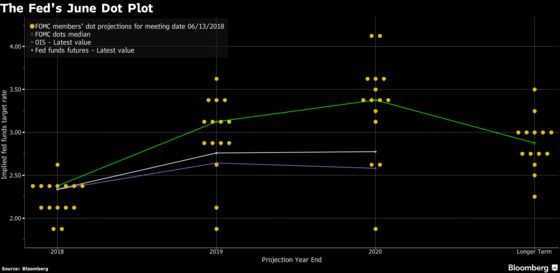

Drop the dots

In 2016 a group of Wall Street economists declared in a paper that the dots -- a graphic representation of interest-rate forecasts from each Federal Open Market Committee participant -- had “outlived their usefulness.”

Powell offered a defense of the dots at the time, but conceded that sometimes the dots and the FOMC’s policy statement “have seemed to send conflicting signals.” More recently, he stressed during his March press conference that “the committee doesn’t vote or agree upon the medians,” thereby downplaying any signal they might send.

Still, it’s hard to find anyone who thinks Powell will drop the dots altogether. While they may be flawed, scrapping them might be seen as reversing the Fed’s gradual march toward more transparency, according to Roberto Perli, a former Fed economist and now partner at Washington-based consultancy Cornerstone Macro LLC.

“If you drop them you have to replace them with something,” Perli said. “You don’t want to go back to the dark days when monetary policy was made in secrecy.”

Trimming the dots

An alternative would be to reduce the number of years included in the projections, not only for the path of rates but also for inflation, unemployment and economic growth. That would fit comfortably with Powell’s efforts to emphasize the limits of the Fed’s knowledge.

Asked about the median rate forecast for 2020 at his March press conference, Powell dismissed its importance almost entirely.

“That’s three years in the future,” he said. “We don’t have the ability to see that far into the future, so I really wouldn’t put a lot in that.”

Yet, if past practice is any guide, the Fed will release a new set of forecasts next week that will add a year, extending all the way to 2021. What, one might ask, is the point?

Economists agreed the new numbers will be almost entirely useless as forecasts. And yet, none favored cutting a year, preferring more information, however flawed, to less.

“That’s the most interesting thing for me next week,” said Omair Sharif, a senior U.S. economist at Societe Generale SA in New York, referring to the 2021 projections. “No, it’s not reliable, but I still think it’s a useful guidepost for what the Fed is thinking the economy’s going to look like, and how high they think the Fed funds rate is going to go.”

Who’s dot?

A much more popular change would be to identify the policy maker behind each dot. That would be helpful since some central bankers are considered more influential than others in the monetary policy debate, beginning with the chairman.

If that’s a step too far for Fed officials, there’s another option favored by economists that stops short of naming names: connecting each unnamed dot to the same author’s economic forecasts.

That would help explain the variations between projections, revealing, for example, whether one official’s higher rate forecast were due to a more optimistic view on growth, or perhaps a more pessimistic view on inflation.

“That would be an enhancement, a useful one without giving away too much,” said Peter Hooper, chief economist for Deutsche Bank Securities in New York and a former Fed staffer.

Long shots

Another favored idea, albeit viewed as a very long shot, would be for the Fed to abandon its individualist ways and to agree on a set of consensus forecasts each quarter, thereby providing a much more powerful signal of the committee’s intentions. The Fed has explored just that possibility in past years, but found it too difficult to coral the committee behind one outlook.

“It’s what they should do but probably won’t,” said Perli. “It’s hard to put together a consensus when you have that many people.”

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Randall Woods

©2018 Bloomberg L.P.