San Francisco Fed Pick’s Research, From Wages to Growth

San Francisco Fed Pick’s Research, From Wages to Growth

(Bloomberg) -- Mary Daly will become Federal Reserve Bank of San Francisco President on Oct. 1, bringing with her decades of experience researching job markets and public policy.

That could make Daly, whose promotion was announced Friday, an important voice as the Federal Open Market Committee assesses how hot today’s labor market is running and what risks that might pose. Daly’s research has influenced policy makers before (former Chair Janet Yellen used to quote her wage studies), and her CV hosts papers that zero in on workforce-relevant issues including inequality, education and economic mobility.

Here’s a primer to get you up-to-speed on her work.

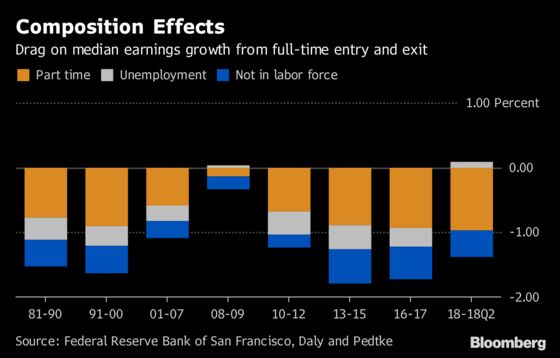

Wage Optimist

Revisiting Wage Growth

Published August 2018

Daly and her co-authors say that pay is better than it looks: it’s just being held down as new and returning workers jump into full-time jobs, because they typically earn less than their more consistently experienced counterparts. That, together with a large-scale exit of high-paid baby boomers from the labor force, could be holding down median weekly earnings by 1.5 percentage points to 2 percentage points, she wrote in a recent blog post. “The real question going forward is what should wage growth be in an economy that is sustainably running at full employment.”

Growth Outlook

Raising the Speed Limit on Future Growth

Published April 2018

Daly pointed to slow growth in the labor force as a “restraining factor on the U.S. economic speed limit” in this post, which was adapted from a speech she delivered earlier this year. She noted that the drop in U.S. prime-age labor force participation looks different from other countries, citing a combination of work-life decisions, middle-skill job loss, and insufficient job training as reasons. “Investing on this front is a lever we can pull that changes the fundamentals of economic growth and gives us an opportunity to raise the speed limit.”

Natural Changes?

The Recent Evolution of the Natural Rate of Unemployment

Published January 2011

In the wake of the crisis, Daly and her colleagues and frequent co-authors Bart Hobijn and Rob Valletta raised an eyebrow at the idea that the unemployment rate under which inflation would start picking up -- often called NAIRU or the natural rate -- had jumped higher. Their exercise suggested that while that natural rate had risen by 0.6 to 0.9 percentage point, it was unlikely to stay up there for long: the pop was driven by extended unemployment insurance and productivity gains, not mismatch between workers and available jobs.

Daly’s work here proved prescient, and even too cautious: while it took unemployment a while to come down from its above-9 percent 2011 levels, it’s now clocking in at 3.9 percent and the Fed has consistently revised down its long-run unemployment estimate.

Pay Restraints

Downward Nominal Wage Rigidities Bend the Phillips Curve

Published January 2014

In a paper that Janet Yellen cited, Daly and Hobijn found that pent-up wage deflation could be holding down wages in a post-crisis world. The idea goes like this: it’s hard for companies to cut worker’s pay, even if the economy is souring and they’d like to do so. Instead, they fire some employees and keep wages steady for those they retain. Then, when the economy bounces back, there’s “pent-up wage deflation” that “leads to a simultaneous deceleration of wage inflation and a decline in the unemployment rate during the ensuing recovery period.”

“This bending of the Phillips curve is especially pronounced in a low inflationary environment,” they wrote.

Daly has also written papers and posts on inequality and mortality, the paradox of why people in the happiest places are also most likely to commit suicide, on racial wage gaps, and economic mobility. We don’t have room for all of them here, but if it’s a slow day, they’re worth a read.

To contact the reporter on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Randall Woods

©2018 Bloomberg L.P.