China’s Debt Bomb

It’s been called a mountain, a horror movie, a treadmill to hell and a bomb.

(Bloomberg) -- It’s been called a mountain, a horror movie, a treadmill to hell and a bomb. To doomsayers, China's $34 trillion pile of public and private debt is an explosive threat to the global economy. Or maybe it's just a manageable byproduct of the boom that created the world’s second-biggest economy. Either way, the buildup has been breathtaking, with borrowing quadrupling in seven years by one estimate. (China doesn't give a complete tally). President Xi Jinping has taken note, pushing authorities to announce a slew of measures that target risks lurking in the financial system. The challenge is how to wean the country off its debt drip without intensifying an economic slowdown. Since China is a key driver of global growth, it's a matter of concern for everybody.

The Situation

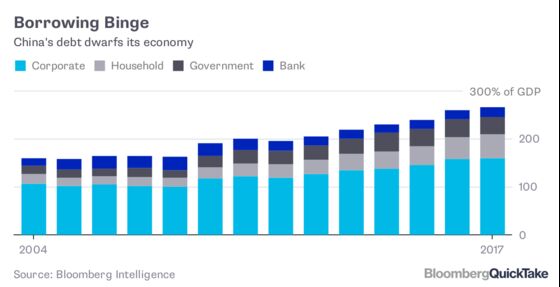

Even with the government focus on deleveraging, Chinese borrowing rose 14 percent in 2017, ballooning to 266 percent of gross domestic product, from 162 percent in 2008. That growth outpaced the U.K. and U.S. in the decade before the financial crisis. However, the de-risking campaign has begun to bite: Once-rare corporate debt defaults ran at a record pace in 2018; China’s huge conglomerates were reined in following debt-fueled acquisition sprees; the government targeted spending cuts in its budget; and sweeping rules were introduced to tackle shadow banking, a $10 trillion network of unregulated lending and risky investment products. There’s also been a focus on curbing loans to bloated state-owned enterprises, a task that Xi termed “the priority of priorities.” (More than half of China’s debt is held by state and private corporations.) The upshot is that the cycle of expanding credit that began in 2004 has ended, according to S&P Global Ratings. Nonetheless, former central bank governor Zhou Xiaochuan warned in late 2017 of a buildup of financial risks that are “hidden, complex, sudden, contagious and hazardous.”

The Background

During the 2008 financial crisis, Beijing ordered local governments to build roads, bridges and other public works to keep the economy pumping and workers in jobs. It set off a borrowing binge that’s invited comparisons with Japan’s debt bubble of the 1980s. That ended in a property and stock market crash which left banks saddled with bad debt for decades. China has seen busts before. In the late 1990s, after years of state-directed lending, at least a quarter of the nation’s credit soured, triggering a $650 billion bailout of state banks. The central government retains tight controls over banks, foreign exchange and capital flows, so it can manipulate the financial system to contain the debt burden and limit the risk of a blowup. At the same time, officials say they are keen to introduce more free-market discipline, which could further increase their tolerance for bankruptcies. China’s concerted shift toward an economy driven by domestic consumption, and less reliant on debt-intensive heavy industry and exports, is also contributing to the easing of the debt habit. Even so, the government remains willing to change tack when the economy is threatened: A brewing trade war with the U.S., coinciding with those moves to curb leverage and shadow banking, began to make it harder for companies to get funding in 2018. That prompted authorities to introduce monetary easing measures, such as freeing up banks to make more loans to smaller businesses.

The Argument

Optimists say concerns about China’s debt are overblown; companies and local governments can simply grow their way out of the problem as an expanding economy supports borrowers and creates inflation, which erodes the burden of debt repayments. China’s high savings rate helps, as does a long run of current-account surpluses, which makes the country a net lender to other nations rather than a net borrower. Pessimists say the problem is not self-correcting. They expect policy makers to tackle nonperforming loans and stave off defaults. Options include cutting interest rates, expanding programs where investors swap debt for equity, clamping down harder on shadow banking, pushing for asset sales and encouraging more companies to raise money through stock sales. There’s a risk that China’s debt could at best be a drag on global growth for decades or at worst trigger a new financial crisis. Such warnings have been sounded for years, however, all the while as China has continued an unprecedented economic expansion driven by mountains of credit.

The Reference Shelf

- A Bloomberg infographic digs into the growing pile that is China's debt.

- An IMF report on China's debt from 2016.

- McKinsey examined the size and complexity of China’s debt in a 2015 report.

- The International Center for Monetary and Banking Studies researched the expansion of global debt.

- QuickTake Q&As on wealth management products and another potential problem called entrusted bonds.

- Bloomberg QuickTakes on shadow banking, China’s managed markets, and the yuan.

- Bloomberg Intelligence's blog examined the buildup of local government debt and the overall debt problem.

- Charlene Chu, a banking analyst who made her name warning of the risks from China’s credit binge, details the case for a “massive bailout.”

To contact the editor responsible for this QuickTake: Grant Clark at gclark@bloomberg.net

©2018 Bloomberg L.P.