China's Central Bank Has $1.3 Trillion Money-Fund Headache

The aggregate lending figure, including shadow banking, showed borrowers are increasingly having to turn to the debt market.

(Bloomberg) -- China’s ever-growing money market funds pose an increasing problem for the nation’s central bank as policy makers attempt to boost the flow of credit to cushion an economic slowdown.

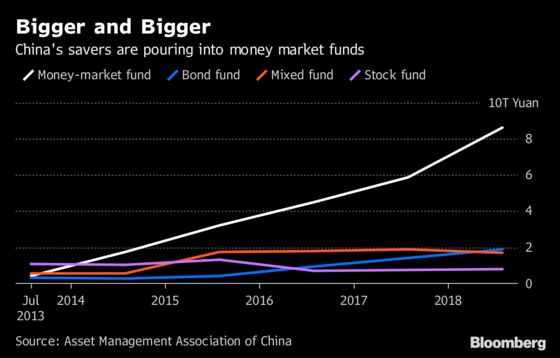

While the funds have offered savers a handy alternative to risky stocks and once high-flying wealth management products, they’re effectively raising borrowing costs. That’s because, with some 8.6 trillion yuan ($1.3 trillion) according to the Asset Management Association of China, they’re sapping the flow of savings to banks, which in turn are having to pay the funds higher rates when taking their cash as deposits.

Those higher costs are being passed along to borrowers, countering the efforts of the People’s Bank of China to reduce lending rates for small- and medium-sized companies in particular. And the bargaining power of money funds is growing -- the assets are close to the personal deposits at Industrial & Commercial Bank of China Ltd., the world’s largest lender by assets.

“Investors’ risk tolerance has been falling amid weak stock and bond market performances,” so they’ve been turning to money-market funds, said Nie Wen, a Shanghai-based economist at Huabao Trust Co. “The money market funds’ investments may not necessarily end up in the hands of medium and small enterprises.”

Financial Repression

It was a lot simpler years ago, when Chinese households had few options other than bank deposits and regulators set the rates on those savings pools. That allowed the PBOC to easily cut funding costs for banks; the central bank also set the lending rate.

“While policy makers only needed to focus on the banking system to boost lenders’ willingness to loan, they now face bigger challenges and need more measures to achieve the same goal, given the size of such funds,” said Xia Le, Hong Kong-based chief Asia economist at Banco Bilbao Vizcaya Argentaria SA.

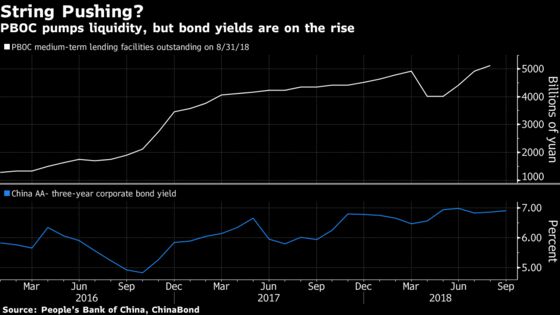

The pressure on banks’ loan-creation engine was evident in data last week. New yuan loans in August fell short of forecast. And the aggregate lending figure, including shadow banking, showed borrowers are increasingly having to turn to the debt market. Sales of short-term bills by nonfinancial companies surged to the highest since February 2009. With bond yields on the rise thanks in part to record default rates, borrowers are increasingly stuck.

One sign of the impact of tougher credit conditions came Friday, with data showing the smallest gain in investment spending on record. China could have a new round of supportive measures to stabilize investments, the Economic Information Daily reported on Tuesday, without saying where it got the information.

The People’s Bank of China offered no immediate response to a fax seeking comment about the funds’ growth affecting efforts to support loans.

Savers have plenty of reason to keep turning to money-market funds, after the Shanghai Composite Index of stocks tumbled into a bear market and bond defaults made credit a risky option. The market expanded 12 percent in July, up 28-fold from 2013, Asset Management Association of China data show.

The world’s biggest fund, Yu’EBao, illustrates the challenge for policy makers. It has 62 percent of its 1.45 trillion yuan in bank deposits and 9.4 percent in bonds -- mostly sovereign and policy-bank notes, according to the latest report posted on the website of Tianhong Asset Management Co., which manages Yu’EBao.

Limits Imposed

Authorities have appeared to recognize the issue, last year asking Alibaba Group Holding Ltd.’s Ant Financial affiliate, which holds a majority of the Yu’EBao manager, to cut the maximum amount individuals can invest in it. Other funds have taken action more recently, with Harvest Fund Management Co. starting to curb daily aggregate subscriptions for each account from August, after Penghua Fund Management Co. started doing so in July.

The main consideration is to ensure healthy development of fund performance and size so that investors’ interest can be protected, according to an emailed reply from Harvest Fund Management when asked about the reasons behind the change. Tianhong and Penghua declined to comment.

“While these products do bring convenience and become good investments for households, the economy hasn’t benefited, and it even brings risks to the financial system,” said BBVA’s Xia. “This has caught regulators’ attention,” and their guidance might be behind the recent curbing measures, he said.

--With assistance from Jun Luo.

To contact Bloomberg News staff for this story: Helen Sun in Shanghai at hsun30@bloomberg.net;Heng Xie in Beijing at hxie34@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, ;Richard Frost at rfrost4@bloomberg.net, Ron Harui

©2018 Bloomberg L.P.

With assistance from Editorial Board