Only Economist to Call Russia Rate Hike Was Also in for Jolt

The surprise pivot to rate increases was one part of a response by Governor Elvira Nabiullina to threats of U.S. sanctions

(Bloomberg) -- The sole economist to correctly predict the Russian central bank’s first interest-rate increase since 2014 felt a jolt at seeing the outlook that accompanied Friday’s decision.

For Region Investment Co.’s Valery Vaisberg, whose forecast was the only one on target in a Bloomberg survey of 42 analysts, the upswing in inflation assumed by policy makers is, “of course, pessimistic.”

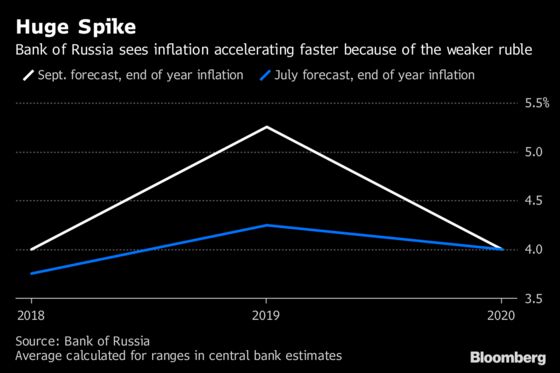

After a selloff in the ruble over recent weeks, the Bank of Russia now sees price growth surging past its goal of 4 percent, reaching 5 percent to 5.5 percent by the end of 2019 from 3.1 percent last month. That’s an upward adjustment of one percentage point in the path for inflation it laid out earlier.

“I didn’t expect a serious change in the central bank’s forecasts,” said Vaisberg, head of research at Region, an investment company in Moscow that manages 479 billion rubles ($7 billion) in assets. “Now it’s clear that we are really shifting to a tightening cycle.”

The surprise pivot to rate increases was one part of a response by Governor Elvira Nabiullina to threats of U.S. sanctions that are stalking the market and putting pressure on the ruble.

Besides lifting the benchmark to 7.5 percent from 7.25 percent on Friday, the central bank also announced it’s extending a pause in foreign-currency purchases for reserves until the end of December. In August, it initially suspended the program -- conducted on behalf of the Finance Ministry under the so-called budget rule -- until the end of this month.

Risks Abound

Speaking after the decision, Nabiullina explained the central bank’s rationale as driven by the need to rein in risks of faster price growth and inflation expectations caused by ruble volatility. Similarly, the central bank will refrain from purchases of foreign currency on the market to avoid adding to instability, she said.

A decline of about 9 percent so far this year in the nominal effective exchange rate will contribute nearly one percentage point to annual inflation, according to Nabiullina. A value-added tax increase will also boost price growth by one percentage point in 2019, the central bank estimates.

Inflation might even touch 6 percent at its peak in the first half of 2019, the governor said. Only two economists polled by Bloomberg see inflation around that level or higher in the first and second quarters of next year.

Under the so-called risk scenario, based on an oil price of $35 a barrel in 2019, the economy may shrink and will probably face inflation risks that will require even tighter monetary policy, according to the central bank.

What Now?

There’s little consensus about what course the central bank will take now. The governor said further tightening isn’t inevitable but can’t be ruled out. Rate cuts may not resume for more than a year, she said.

With inflation still forecast around the target this year, the Bank of Russia may wait past next month’s meeting to see if it needs to lift borrowing costs again, said Vaisberg. Although the chance of rate increases is higher in the first and second quarters of 2019, the central bank could refrain from tightening policy further in 2018 if inflation ends this year near 4 percent, he said.

“The risks are clear, sanctions pressure remains,” Vaisberg said.

--With assistance from Zoya Shilova.

To contact the reporters on this story: Artyom Danielyan in Moscow at adanielyan@bloomberg.net;Olga Tanas in Moscow at otanas@bloomberg.net;Anna Andrianova in Moscow at aandrianova@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, Paul Abelsky, Robert Jameson

©2018 Bloomberg L.P.