Economists Bullish on Global Growth Despite Emerging Market Turmoil

Wall Street Is Bullish on Global Economy Despite Emerging Markets

(Bloomberg) --

Wall Street economists are sticking with their forecasts for the global economy to enjoy its strongest growth since the start of the decade even as emerging markets wobble and trade wars escalate.

The reason? The U.S. is prospering from President Donald Trump’s tax cuts, while the euro area and Japan are shaking off their soft patches earlier in the year. China is, for now, also managing to mitigate a slowdown through a mix of targeted stimulus.

Solid growth may ease investor concern that has squashed emerging markets this year and stemmed increases in government bond yields. The MSCI Emerging Markets Index of shares is down more than 13 percent in 2018. The S&P 500 Index, by contrast, has risen about 8 percent, fueled in part by U.S. fiscal stimulus.

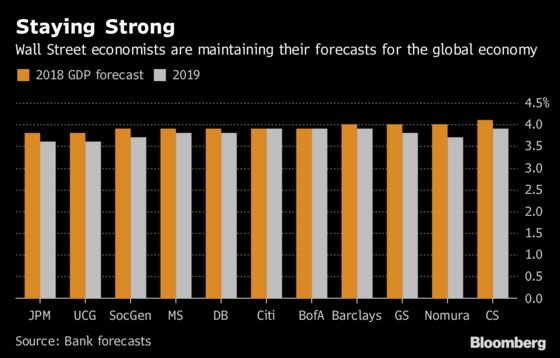

Here’s a rundown of what economists at major banks are saying in reports and interviews about the world economy in 2018 and 2019. While most acknowledge the risks to their estimates have grown, they still see expansions rates of just below 4 percent this year and next in what would be the best back-to-back performance since the turn of the decade.

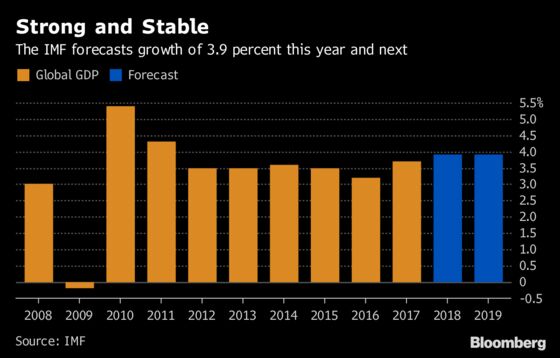

The predictions are mostly in terms of purchasing power parity, the metric favored by the International Monetary Fund which will next month reissue fresh forecasts after July’s prediction of 3.9 percent expansion this year and next.

JPMorgan Chase & Co. (2018: 3.8%, 2019: 3.6%)

The developed market economy “as a whole is on track to deliver growth a full percentage point above our estimate of potential. Despite our constructive outlook, risks remain skewed to the downside.”

--Bruce Kasman, chief economist, Sept. 8 report

Morgan Stanley (2018: 3.9%, 2019: 3.8%)

“While global growth is tracking above trend and in line with the forecasts in our mid-year outlook, the underlying tensions in the global economy have risen, adding to investors’ worries about the cycle. Our base case forecast remains that global growth will moderate, but stay above trend.”

--Sept. 10 report

Deutsche Bank Group AG (2018: 3.9%, 2019: 3.8%)

“The recent readings of both soft and hard data from the U.S. shows that growth momentum will continue and the European data has also been surprising to the upside more recently. The negative impact of tariffs will subside within a few quarters, which should limit the negative impact on global growth. There are some downside risks to the global economy mainly emanating from the current emerging market crisis and geopolitical tensions, but these risks seem manageable at this point.”

--Torsten Slok, chief international economist, Sept. 6

Citigroup Inc. (2018: 3.9%, 2019: 3.9%)

“We expect second half global growth to be relatively solid, but risks are clearly tilted to the downside, including as capex momentum has stalling. We expect the rest of the world to catch up somewhat with the U.S. In addition to bottoming growth in China, that also requires euro zone growth to remain solid. The emerging market outlook is a major concern: Growth effects have so far been limited to the most vulnerable economies.”

--Pernille Bomholdt Henneberg, economist, Sept. 9 report

Goldman Sachs Group Inc. (2018: 4.0%, 2019: 3.8%)

“A number of downside risks still linger. Trade tensions have become more concentrated on U.S.-China trade, with other trade disputes taking a somewhat more constructive direction (including NAFTA and auto tariffs). The road to an agreement on the Italian budget is likely to remain quite bumpy and we expect significant volatility in Italian asset prices in coming weeks. And while we still see a Brexit deal as the most likely scenario, the risk of a disorderly exit has increased in recent months. On a more encouraging note, the risk of a systemic financial crisis still looks low.”

--Jan Hatzius, chief economist, Aug. 24 report

Bank of America Corp. (2018: 3.9%, 2019: 3.9%)

“The strong growth reflects a combination of improving confidence and continued super easy monetary policy. Consumers and firms have learned to look through the political and geopolitical news. U.S. tax cuts and spending increases are an additional double dose of caffeine.”

--Ethan Harris, chief economist, Sept. 12

Barclays Plc (2018: 4.0%, 2019: 3.9%)

“While global growth has slowed, momentum in developed market economies and stimulus in China led us to conclude that growth was likely to remain balanced. We expect a sizeable upward revision in second quarter growth in Japan, on account of capex, to provide further evidence in support of this view. That said, purchasing managers data globally point to a slowing in new export orders which we believe is related to fears of protectionism.”

--Sept. 7 report

UniCredit Group (2018: 3.8%, 2019: 3.6%)

“A lot of what we have seen, particularly in emerging markets, was rather predictable because of the state of the global business cycle and the policy responses, including Fed tightening, as well as the long-identified vulnerabilities to external financial shocks in places like Turkey and Argentina. This force is unlikely to end until the U.S. slows down and the Fed stops hiking.”

--Erik Nielsen, global chief economist, Sept. 9 report

Credit Suisse Group AG (2018: 4.1%, 2019: 3.9%)

“Global growth slowed in the first half of the year but remains at a healthy level. It is likely to accelerate gradually in the fourth quarter. Demand fundamentals among the major economies are robust. Short-term growth in China has weakened recently, but we expect it to pick up in the coming months as policy easing measures start to gain traction. U.S. growth remains supported by fiscal stimulus.”

--Investment Committee Report, Sept. 6

Societe Generale SA (2018: 3.9%, 2019: 3.7%)

“For now prospects for global growth look about as solid as they did three, six, or nine months ago, but downside risks are becoming increasingly pronounced. These risks are rooted in cyclical and financial factors, but more importantly in policymaking.”

--Sept. 11 report

Nomura Holdings Inc. (2018: 4.0%, 2019: 3.7%)

“Global growth appears to have been holding up relatively well in recent weeks despite a steady flow of negative news about protectionism and emerging economies. Labor markets, for example, have continued to strengthen in most developed economies, particularly in the U.S. And, while forward looking sentiment surveys suggest manufacturing activity and world trade have slowed, this is being offset by strong growth in services. Meanwhile, on the inflation front, while headline rates have been drifting up in most advanced economies, this has largely been due to higher energy prices. Underlying price pressures are still fairly subdued, particularly outside of the U.S.”

--Sept. 11 report

Read more:

- Summer Scorches Green From Global Growth Traffic Lights

- How Far Is Too Far? Analyzing the Emerging Market Overshoot

- Global Economy Still Feeling Lehman Fallout 10 Years On

--With assistance from Paul Dobson.

To contact the editor responsible for this story: Zoe Schneeweiss at zschneeweiss@bloomberg.net

©2018 Bloomberg L.P.