China Bond Traders Boost Leverage With PBOC Watching Closely

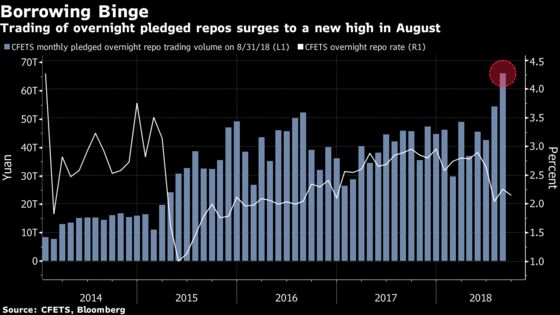

The turnover of Chinese overnight repurchase contracts increased $9.6 trillion.

(Bloomberg) -- Chinese bond traders ramped up their leverage to a record high in August, and that could be catching the central bank’s attention.

The turnover of overnight repurchase contracts, a tool traders use to seek financing to fund their bond purchases, increased for a second straight month to hit 66.1 trillion yuan ($9.6 trillion), official data showed. In August, the People’s Bank of China conducted repo agreements -- an instrument that hadn’t been used in about three years -- to mop up about 300 billion yuan of liquidity from the banking system, according to people familiar with the matter.

“The PBOC’s move was likely aimed at slowing the buildup of leverage and reducing short-term liquidity,” said David Qu, Shanghai-based economist at Australia & New Zealand Banking Group Ltd. “But it won’t damp traders’ motivation to borrow cheap funding and buy bonds -- they’d keep doing that as long as they expect money market rates to remain stable.”

The surge in leveraged buying of debt is a double-edged sword. On one hand, it could mean the central bank’s monetary easing will finally feed into China’s real economy as banks increase lending to companies via corporate bond purchases. On the other hand, it could signal a setback in the government’s efforts to reduce financial leverage. China will keep liquidity reasonably ample, without “flooding” the banking system through abundant cash supply, PBOC Deputy Governor Zhu Hexin said in late August.

The PBOC drained short-term funds last month in an unannounced repo operation, people familiar with the matter said last Wednesday. The central bank said the report is not true, declining to give further details.

The reported cash withdrawal came as interbank rates tumbled to multi-year lows in August. That has spurred some traders to use their money borrowed via short-term repos to purchase bonds, said Julia Ho, the head of Asian Macro at the Asian fixed-income team at Schroder Investment Management Ltd. in Singapore. Most of the leveraged-related trading is aimed at policy banks’ bonds as well as investment-grade state-owned enterprises’ debt and local government financing vehicles, she said.

“The carry trade will remain profitable until at least next year,” said Meng Xiangjuan, an analyst at SWS Research Co. in Shanghai. “Officials won’t put limitations on the trade, as long as the level of borrowing remains normal. That said, the room for significant spikes in leverage is limited, as officials have placed plenty of restrictions in the past years already.”

The benchmark seven-day repo rate was little changed at 2.67 percent on Tuesday, after spiking amid tighter liquidity late last week. The overnight cost rose 1 basis point to 2.58 percent. That brings the gap between the overnight rate and the yield of six-month AA+ rated NCDs to about 99 basis points, a spread that makes the carry trade still attractive, according to ANZ’s Qu.

That doesn’t mean the PBOC will keep its hands tied and watch leverage expand indefinitely. For Xu Hanfei, chief fixed-income analyst at Industrial Economics Research & Consulting Co. in Shanghai, the central bank may boost the overnight repo rate as it follows the Federal Reserve in an expected increase in borrowing costs this month.

To contact the reporter on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net

To contact the editors responsible for this story: Will Davies at wdavies13@bloomberg.net, Ron Harui, David Watkins

©2018 Bloomberg L.P.