ECB Endgame Has Governments Thinking About Rate-Hike Damage

ECB Endgame Has Governments Debating Possible Rate-Hike Damage

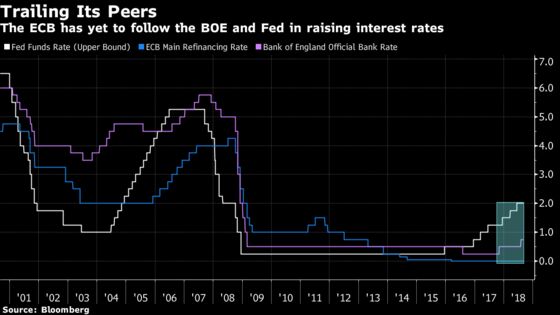

(Bloomberg) -- European finance ministers and central bankers will gather in Vienna this week to discuss a key test for the euro zone’s expanding economy -- whether it can cope with interest-rate hikes.

The debate reflects the currency bloc’s relatively solid economic health after a decade of crises and recessions, but also marks a new challenge. The European Central Bank’s plan to gradually unwind years of extraordinary monetary stimulus comes with the risk of destabilizing asset markets such as stocks and real estate if they’re bloated by cheap money.

Higher interest rates could also cause problems for national governments, which have increased borrowing in the past decade. Total debt in the euro area stands at about 84 percent of gross domestic product this year, compared with 65 percent in 2007, according to the International Monetary Fund.

Some countries have already sounded the alarm. The Bundesbank reckons that German homes are overvalued by as much as 35 percent in major cities. France is concerned about high levels of corporate debt. Italy’s populist government worries that the nation’s bond market could be hit by speculators when the ECB pulls back.

“Our experience is that once there is a bubble it’s very often resistant to small interest-rate increases,” said Daniel Gros, director of the Centre for European Policy Studies, who will present a paper at the twice-yearly policy forum. “They’re right they should start thinking about it as a clear and present danger.”

Gros’s paper concludes that higher interest rates “do not need to be the harbingers of wider financial-market instability.” In fact, continuing the policy of keeping rates low for a long period “might, over time, lead to a build-up of vulnerabilities.”

For ECB policy makers, the question is what’s in their remit and what should be left to governments. Chief economist Peter Praet acknowledged last month that the central bank must monitor markets because stable consumer prices alone can’t ensure financial stability. Bundesbank President Jens Weidmann said officials may need to tackle imbalances to prevent them from snowballing into a financial crisis.

But both men pushed back against the idea that the central bank should make financial stability part of its primary mandate alongside inflation, with Weidmann saying that might do more harm than good.

“There is no way in which monetary policy alone is capable of ensuring financial stability,” said Claudio Borio, head of the Monetary and Economic Department at the Bank for International Settlements, who has urged policy makers to accept that the exit from easy money will be bumpy. “What you require is moving toward a macrofinancial stability framework, which includes not just monetary policy but also regulation and supervision, fiscal policy and even structural policies. You really need a package.”

Recession Predictor

The debate echoes discussions in the U.S. and U.K. where the Federal Reserve and Bank of England have already started tightening. At last month’s Jackson Hole symposium, Fed Chairman Jerome Powell signaled the need to link financial stability to interest-rate policy, saying “destabilizing excesses” appeared in the run-up to the last two recessions.

The Bank of England has separate committees for monetary policy and financial stability, with some members including Governor Mark Carney sitting on both panels. Deputy Governor Ben Broadbent defended that setup in April, saying a single committee might pay too much attention to its “more verifiable objectives” of price stability, potentially at the expense of financial stability.

The ECB’s most-recent Financial Stability Review in May called the macroeconomic environment “favorable,” while noting “vulnerabilities” in some housing markets. It also cited high indebtedness and the risk of looser fiscal policy as potential flashpoints, reflecting concerns about the impact of higher rates on national finances.

“The only reason why one really cares about financial instability at the end of the day is because it can have big macroeconomic costs,” said Borio. “What’s really essential is that you have sufficient room for maneuver to be able to reconcile any financial-stability considerations with your inflation objective, which is clearly the bread and butter of a central bank.”

--With assistance from Birgit Jennen, Ruben Munsterman, Boris Groendahl, Alexander Weber, Nikos Chrysoloras and John Glover.

To contact the reporter on this story: Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint

©2018 Bloomberg L.P.