Ditch the Playbook, Just Follow Buffett and Trump: Taking Stock

Ditch the Playbook, Just Follow Buffett and Trump: Taking Stock

(Bloomberg) -- All your trades (are) belong to the U.S. Presidency.

Whatever your game plan was to close out what became one of the busiest Augusts in recent memory was likely rendered moot late Thursday on a Bloomberg report that Trump is seeking to move ahead on tariffs on $200 billion worth of Chinese imports, subject to a public comment period that concludes Sept. 6. What was already a middling day hovering around the unchanged mark became markedly worse for the S&P 500, as this round of tariffs would be the largest thus far in the trade saga. Materials and the trade-sensitive industrial names like Caterpillar and Kansas City Southern were among stocks hit on the news, as money shifted to more defensive sectors like utilities and staples, with tobacco and food retailer sub-sectors the best performers on the day.

Worldwide markets are in the red early Friday as commerce and trade fears reemerge (Trump also threatened to pull out of the WTO), despite China PMI figures that were better than expected. S&P futures appear to be holding up rather well, poised to open below its newfound “support” at 2,900. Equity indexes have been resilient in the face of Trump shocks before, and today looks no different (on pace to post a weekly gain).

But What Happened Before the Bombshell?

It’s tempting to allow the Oval Office news to wipe away all of yesterday’s action, which featured Warren Buffett again singing the praises of equity markets. His commentary spurred a round of buying, especially in Apple (which also announced its next presumed iPhone unveiling for Sept. 12) as he admitted to buying more shares. This was timely as by the end of the day, the top four names pushing against losses in the S&P were, you guessed it, FAANG names (AAPL, AMZN, FB, NFLX). Rounding out the top five was Micron, mentioned in this column Thursday (its suppliers LRCX and AMAT were also higher, as the S5SEEQ index was among the top performing subsectors in an otherwise down-ish day).

AMZN and FB are now marginally lower in the pre-market (GOOGL ever so slightly post-market) after Trump singled the three out as a possible “antitrust situation.” China Internet names too (HUYA, BABA, IQ), are also down pre-market, likely on renewed tensions. Other parts of the interview touched on Trump’s rejection of the EU tariff offer on autos, leading all members of the EURO STOXX Automobiles & Parts index into the red. Watch U.S. names GM, F, GT and CTB for volatility.

There was also a bit of merger mania Thursday ahead of the long weekend in the U.S. (CPB asset sale plans, REXX, REIS/MCO, PARR, KTWO/SYK), which continued into this morning with Coca-Cola’s expansion into the coffee market in a $5.1 billion deal to buy U.K. coffee shop Costa from Whitbread Plc (watch KDP, DNKN, QSR, KKD, SBUX).

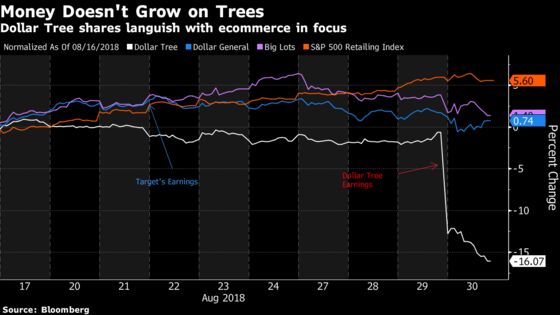

M&A led most of the names in the green, while discounters and dollar stores suffered (mainly DLTR). Closeout retailer Big Lots hit the tape with their earnings and early indications are for shares to open down 11 percent given a weaker-than-expected forecast.

And Wasn’t Today Supposed to Be NAFTA Day?

Friday was supposed to be about welcoming a deal from U.S. and Canadian officials on NAFTA, validating strength in equity indices earlier in the week while assisting the “melt-up.”

We were also supposed to be wary of contagion from emerging markets. The Turkish lira had resumed its downward move after a brief respite, giving up 11 percent of its value over the past four days (keep the ETF TUR in mind), while Argentina’s peso lost a third of its value in the two days since the government requested the IMF speed disbursements from a credit line (ETF ARGT had its worst day on Thursday in three years, and counts cult-ish name MercadoLibre as a top holding at 31 percent). This appears to be spreading with weakness in the Indonesian rupiah (weakest in 20 years) and the Indian rupee early (touched record lows).

We also wanted to take solace in knowing athleisure is alive and well, with Lululemon stock up 11 percent pre-market market with results. The COO said the demand in recent quarters was not slowing down. In a similar apparel vein we were to be curious if Abercrombie could recover from its worst day in more than a year after sales missed expectations.

And surely, cannabis was to be a topic of conversation as the news bombs keep driving this segment. Trump met his match with Citron Research’s Andrew Left, who waded into Cronos (previously unscathed from Wednesday’s report that the Administration was waging a "secret war" on marijuana), by cautioning on its valuation and placing a price target 70 percent below where it had then traded. Cronos extended its losses in the post-market after closing down 28 percent. It remains up 58 percent on the month despite the move. Fellow cannabis names TLRY, CGC fell in sympathy. Citron’s prior cannabis target, CV Sciences, staged a 27 percent recovery Thursday after it attempted to refute short seller allegations (and Citron claimed to have covered its short a day earlier).

Cloud software developer and new IPO Zuora is also due for an interesting day. Its lockup expiry today coincides with its second earnings report, which disappointed investors post market (-12 percent), as 3Q loss views came in worse than expected. This follows its last earnings report where it spiked 19 percent. In other earnings, American Outdoor Brands (formerly Smith and Wesson) spiked 29 percent post-market after its better than expected results -- now poised to erase much of its underperforming year (down 24 percent YTD).

On Tap for Next Week

A re-categorization of investor favorites will unfold with the heralded (?) creation of the Communication Services sector, which will include FAANG components FB, GOOGL and NFLX that were lumped into the Info Tech segment previously. These mega caps will now be part of a larger space that is comprised of other telecoms and media names and amount to ~10 percent of the S&P 500, according to Goldman Sachs.

Conference season is upon us. B Riley FBR Healthcare conference kicks off Tuesday in this abreviated holiday week, and the energy sector will be focus as the Barclays Energy Power conference gets underway Wednesday with crude up 16% year to date. Barclays is also running a Consumer Staples conference where we can hear from CAG, TUP, among others. Buckingham has its banking, cards and payments conference (any crypto commentary?). Citi is featuring Biotechs and Technology in conferences this week (two of some of the best performing sectors on the year).

Earnings is light, with earnings from Broadcom, furniture retailer RH, Gamestop and some tech names WDAY, PANW, MRVL and the deal-exposed Dell Technologies. Economic data will feature some key catalysts including monthly auto sales on Tuesday, ADP Employment data on Thursday (a day later than normal due to the Holiday week), and the much awaited Nonfarm Payrolls data Friday.

Notes From the Sell Side

Electronic Arts is getting a slight defense from one its largest bulls. Wedbush (has EA on its Best Ideas list) saw the surprise decision to delay its Battlefield V release date as the right decision in efforts to add extra polish to the game. Analyst Michael Pachter lowers units ests. for FY19, but keeps FY20 estimates for revenue and PT at $158 (implies 36% upside after Thursday’s near 10% downdraft).

Nutanix is getting multiple defenses after shares fell 6% post market. RBC’s Matthew Hedberg is a buyer on the weakness as the results were "strong". He sees the push towards a software-only model as a key highlight with high FCF margins. Piper’s Andrew J. Nowinski reiterates his overweight rating. Nowinski sees the cloud platform and storage provider’s new term-based subscription offering as outweighing the higher operating expense guidance.

Tick by Tick Guide to Today’s Actionable Events

- Today -- IPO lockup expiry: ZUO

- 8:00am -- BIG earnings call

- 8:51am -- Tiger Woods tees off in the Dell Technologies Championship

- 9:45am -- Chicago PMI

- 10:00am -- University of Michigan Sentiment

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Brad Olesen

©2018 Bloomberg L.P.