(Bloomberg Opinion) -- As the American stock market stages its longest bull run in history, investors in China can only look on with envy.

In preparation for a lengthy trade war with the U.S., Beijing has shifted back to a pro-growth stance. The People’s Bank of China revived a measure to support the weakening yuan, while the Ministry of Finance is ready to build infrastructure again. An income-tax cut for the middle class is back on the table.

Yet nothing seems to lift investors’ mood. China’s stock market remains Asia’s worst, with the benchmark Shanghai Shenzhen CSI 300 Index under-performing the S&P 500 Index by close to 30 percentage points for the year.

China’s bear market went through two phases this year. Until the end of May, when the U.S. raised tariffs by an additional 25 percent on a range of products, investors sold out for fear that they’d be caught in Beijing’s intensified deleveraging campaign, with companies in which they hold stakes unable to refinance despite solid fundamentals. After all, shareholders have very few rights when a company defaults on its borrowings.

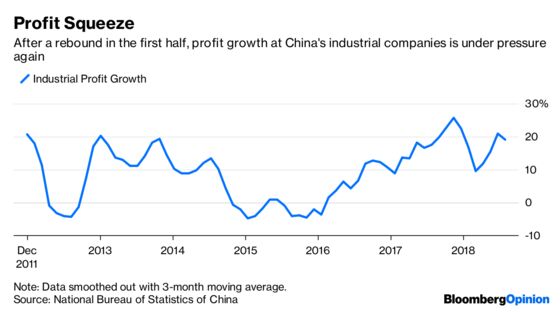

Now, the issue is fragile Chinese earnings. After a nice rebound in the first half, profit margins narrowed in July. Companies are once again feeling pinched.

Blame a variety of headwinds, starting with soaring raw-material costs. Steel prices have climbed from just 1,910 yuan ($280) per ton at the end of 2015 to 4,735 per ton now, while oil recovered from an early 2016 low of $26 per barrel to $68. Of the 41 sub-sectors tracked by China’s National Bureau of Statistics, only 17 saw margin expansion last month.

Tough luck, too, for those that don’t own office or warehouse space. China’s rental market is starting to catch up to soaring home prices, with rentals in Beijing jumping by one-quarter so far this year. Ground-level warehouse rents rose 6 percent from a year ago.

To make things worse, entrepreneurs must shoulder onerous social contributions. They must cough up 19 percent of an employee’s wages to the government’s pension system, and 12 percent of a worker’s salary to the state housing provident fund. Meanwhile, demand is softening. Consumer confidence has turned out to be less resilient than thought, with the anxious middle class worrying over issues from consumer safety to soaring apartment rents.

How can the national team rescue China’s stock market, as it has in the past? Doubling down on infrastructure will just pile yet more debt on already distressed financial companies, which constitute about one-third of the market’s value.

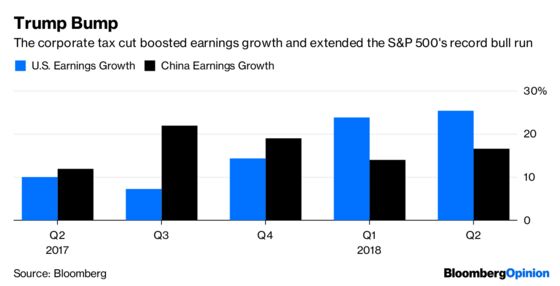

Perhaps Beijing should take a page from President Donald Trump’s playbook and cut corporate taxes. The Trump handout managed to supercharge and protect – however temporarily – the U.S. economy from any trade war fallout. As a result, American companies are reporting stellar earnings this year, underpinning the bull run.

China could do with a lower burden. Counting social safety net contributions, the effective corporate tax rate in China is 67.3 percent, the 12th highest among 190 economies surveyed by the World Bank.

But even those arguing for lower taxes realize how little the nation’s ponderous bureaucracy can do right now. Beijing is in a state of policy paralysis, unsure how long the trade war will last and torn by the dual mandate of fostering economic growth and preventing any Minsky moment. The Ministry of Finance does its budget calculations at the end of the year, so any sweeping tax change is unlikely until early 2019.

Until then, China’s stock market may be doomed to oscillate in bear territory.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.