(Bloomberg Opinion) -- At first glance, investors in China’s big banks should be breaking out the champagne.

Tighter liquidity has boosted margins at three of the big four, with a crackdown on shadow banking forcing borrowers into the hands of Industrial & Commercial Bank of China Ltd., China Construction Bank Corp., Bank of China Ltd. and Agricultural Bank of China Ltd.

The snag is that a retreat from deleveraging is causing the specter of bad loans to return.

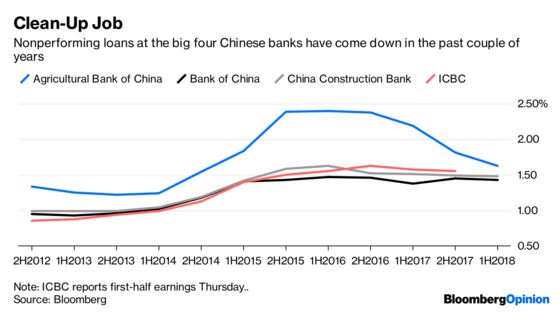

Construction Bank, Bank of China and Agricultural Bank reported gains in second-quarter net income of between 5.2 percent and 7.9 percent on Tuesday. Bank of Communications Co., the fifth-largest by assets, posted a 5.2 percent profit increase last week. ICBC looks certain to extend the trend on Thursday. Notably, bad debt levels fell at all of the four reporting so far.

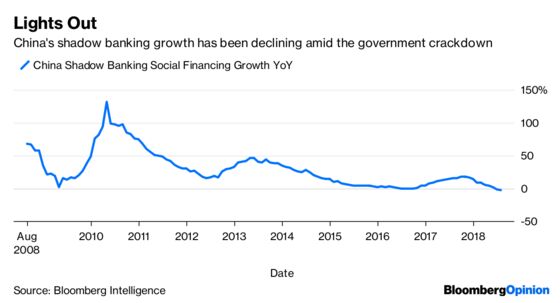

Meanwhile, the chance of a revived threat from shadow banking appears remote: China's campaign to restrain that $10 trillion industry remains firmly in place.

At issue instead is an age-old pattern: Confronted with a slowing economy and a worsening trade war, Beijing is opening the credit taps once again. History shows that when the money flows, prudent loan guidelines go out of the window and capital is inevitably misdirected.

After the central bank loosened liquidity in April, Beijing is now allowing debt-burdened local governments to spend on infrastructure again and encouraging loans for agriculture. Vice Premier Liu He is exhorting banks to lend to smaller businesses, especially those hit by U.S tariffs.

Top that with the credit splurge on President Xi Jinping’s Belt and Road Initiative, and bad news awaits. Belt-and-Road projects don’t always have commercial value, even without factoring in political risks such as the scrapping of agreements by Malaysian Prime Minister Mahathir Mohamad.

The big banks are caught up in this drive: On Tuesday, Bank of China, which has the largest international franchise, said it has so far provided $115.9 billion in “credit support” for more than 600 Belt-and-Road projects.

Now that Beijing has switched its emphasis to stimulus, pressure to lend is bound to fall hardest on the big banks, which are the world’s largest by assets. After all, they’re in a better place to lend than their regulation-bound fintech rivals or smaller counterparts.

Construction Bank and its ilk have been the primary beneficiaries of the deleveraging campaign: As their bad debt fell, system-wide nonperforming loans increased by a record last quarter. China Banking and Insurance Regulatory Commission data show 80 percent of the rise in second-quarter bad debt was from rural commercial banks, Bloomberg Intelligence analyst Francis Chan said.

To be sure, no one expects a repeat of the vast credit binge that followed the 2008 crisis, which saw China’s debt-to-GDP ratio balloon to 266 percent at the end of last year from 164 percent a decade earlier, according to Bloomberg Intelligence data. Having struggled so hard to bring debt under control in the past year, authorities will be reluctant to open the spigots fully.

But it’s telling that share valuations of the big lenders are now flagging, after a strong start to the year when efforts to control debt were at their height and China’s economy looked resilient. They’re trading below one-time book, a sign of investors’ lack of faith in their numbers.

That’s bad news for lenders seeking to replenish capital. Agricultural Bank sold 100 billion yuan ($15 billion) of shares last month, but the buyers were state-linked entities. Moreover, state-owned banks aren’t allowed to sell stock publicly for less than book.

We’ve seen the China stimulus movie before, and there’s little reason to expect a different ending this time. Keep that champagne on ice.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.