The Time Is Ripe to Buy China Sovereign Debt, Analysts Say

It’s time to start buying Chinese sovereign bonds again.

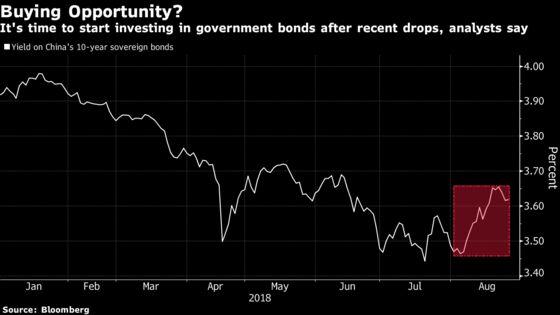

(Bloomberg) -- It’s time to start buying Chinese sovereign bonds, analysts say.

The recent selloff in government bonds has made them attractive as the central bank is about to pour more liquidity into the financial system, while the worsening U.S.-China trade frictions will boost the appeal of safer assets, according to China watchers. The benchmark 10-year yield in August climbed to a two-month high as borrowing costs jumped and as a flood of new local government debt drew in cash from lenders.

"It’s a good time to buy sovereign debt," said Ji Tianhe, a China rates and foreign-exchange strategist at BNP Paribas SA in Beijing. More liquidity will be added "through reserve-requirement ratio cuts and open-market operations, as the proactive fiscal policy may not end up effectively supporting the economy very quickly," he said.

Chinese bonds have bucked analysts’ forecasts to advance for most of this year, becoming the best performing sovereign notes in Asia year-to-date as officials paused their deleveraging campaign in a bid to boost the economy amid rising trade tensions. That rally took an about-turn this month, as local authorities -- being encouraged by the central government -- stepped up bond sales to seek funding for infrastructure projects.

There are signs that sovereign bonds have bottomed. The 10-year yield halted its two-week rising streak last week, with the cost falling 2 basis points to 3.63 percent. The People’s Bank of China on Friday injected a net 59 billion yuan ($8.57 billion) of funds into the banking system -- a move that reflects the authorities’ willingness to keep ample liquidity to offset the drainage resulting from local government’s bond sales, according to China Merchants Bank Co.

The U.S.- China trade war may escalate as the closely watched U.S.-China negotiations last week yielded no major progress. Further trade talks aren’t scheduled, and economists say any new tariffs are set to hurt China’s growth.

"China will keep its policy loose before we see strong signs that the economy has recovered," Citic Securities Co. analysts led by Ming Ming wrote in a note on Friday, adding the 10-year yield could drop to as low as 3.4 percent. "There will be a buying opportunity for government bonds with longer tenors, whenever there’s an overshooting selloff."

Read: PBOC to Offer MLF as Local Bond Supply Increases: Street Wrap

While analysts expect further easing, the PBOC may be prompted to boost interbank interest rates to maintain the yield gap with the U.S. if the Federal Reserve raises borrowing costs next month as expected. The yuan’s weakness is also tying the hands of Chinese policy makers, as aggressively easing the monetary policy would further drive down the currency, which hit a 19-month low this month.

The onshore yuan edged 0.03 percent lower to 6.8210 per dollar as of 5:01 p.m. in Shanghai on Monday, while the 10-year yield rose 1 basis point to 3.64 percent. The offshore yuan fell 0.07 percent to 6.8102 after jumping on Friday following the PBOC’s signal that it’s taking action to support the currency through its daily fixing.

The 10-year yield could drop to as low as 3.3 percent this year, China Securities Co. analysts led by Huang Wentao wrote in a note last week. "Chinese bonds are still enjoying a bull market."

--With assistance from Yuling Yang.

To contact the reporter on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net

To contact the editors responsible for this story: Will Davies at wdavies13@bloomberg.net, Kana Nishizawa, Ron Harui

©2018 Bloomberg L.P.