Time to Buy Indian Bonds as RBI Seen on Hold, HDFC Standard Says

The worst may be over for India’s benchmark bond.

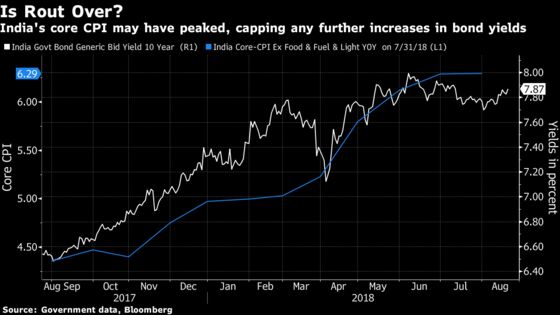

(Bloomberg) -- The worst may be over for India’s benchmark bond as the nation’s inflation rate has probably peaked, HDFC Standard Life Insurance Co. said in a call against market consensus.

The 10-year bond yield may drop to 7.50 percent by end-2018, a decline of 37 basis points from current levels, said Badrish Kulhalli, head of fixed income at the insurer, which has 1.1 trillion rupees ($15.7 billion) under management. Investors will return as confidence grows that the Reserve Bank of India is probably done with further rate increases, he said.

Kulhalli joins a small group of investors betting that a rout in Indian bonds that started last August is coming to an end. Consumer inflation eased in July, while the RBI has adopted a neutral monetary stance after raising rates twice since June. HDFC’s bet is also dependent on the central bank stepping up debt purchases to provide support.

“Our view is that RBI will maintain status quo on interest rates for an extended period, ” Kulhalli said in an interview. The 10-year bond is “the segment where you will see very strong demand coming in the moment there is any turn in sentiment.”

While the median analyst forecast is for the 10-year yield to rise to 7.90 percent by the end of the year, some investors see signs of improvement. Nomura Asset Management Co. said last month that Indian bonds stand out in emerging markets, while Standard Chartered Plc raised its three-month outlook to positive after the latest RBI meeting.

India isn’t in a situation where policy rates need to go much higher than the two-year high of 6.5 percent, given that they are “significantly higher than inflation,” Kulhalli said. Consumer inflation came in at 4.17 percent in July.

Another turning point for the bond market will come if the RBI steps up open-market operations, said Kulhalli, who expects the central bank to buy as much as 1.5 trillion rupees of bonds for the fiscal year ending March. It has purchased 300 billion rupees as of July.

“A big factor which had led bond yields higher right from October last year was the mismatch between demand and supply,” he said. RBI purchases “will shore up the demand side of the balance meaningfully and act as a cap on yields.”

Following are more comments from HDFC Life:

- Along with softening core inflation, if food prices don’t pick up as expected, then overall CPI could undershoot the March forecasts made by RBI

- The Turkey contagion is more of a sentimental impact on emerging markets, rather than a direct hit. It will blow over quickly, and given India’s fundamentals, expects to see inflows into debt and equity pick up

- Risks for Indian fixed-income markets will come from oil prices and potential fiscal slippage

To contact the reporter on this story: Subhadip Sircar in Mumbai at ssircar3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar

©2018 Bloomberg L.P.