If Trump Can Strong-Arm the Fed, U.S. Assets May Not Be So Great

Donald Trump may want to watch what he wishes for.

(Bloomberg) -- Donald Trump may want to watch what he wishes for. If Federal Reserve boss Jerome Powell does what the president wants, American assets could lose their appeal as a global haven.

Strategists warn that more than just the central bank’s credibility would be hurt if the Fed were to put the brakes on monetary policy tightening. Trump would get his desire for a weaker dollar, but rising inflation expectations would dent the perceived safety of U.S. assets and eventually boost longer-term financing costs for the government and American consumers. On the other hand, global liquidity and growth could receive a lift, at least initially, and emerging markets that have been maligned by Trump could benefit.

While few expect the Fed to acquiesce to the pressure, Trump’s policy jawboning has been persistent enough for investors to start factoring its effects into their trading calculus.

‘Playing With Fire’

“This is definitely playing with fire to open this door and begin to undermine the action and independence of the central bank, in this case the Federal Reserve,” said Torsten Slok, chief international economist at Deutsche Bank AG. “We don’t see that on the horizon, but the fact that we are debating this is indeed bringing this question up in many investors’ minds. It opens up questions among investors -- will Powell start listening to this? Is the Fed really independent?”

The Fed’s most recent projections are for another two interest-rate increases this year, following the two it has already implemented in 2018. A step back by the Fed could dent the U.S. currency and, if it was deemed to be more politically motivated, spur a steepening of the yield curve, according to Slok. That would stem from an increase in inflation fears and concern about the role of U.S. assets as a traditional haven.

Since taking office in January 2017, Trump has repeatedly signaled his preference for a weaker dollar and accused other countries over exchange rates. Even with its most recent retreat, the dollar is up more than 5 percent from its April low, buoyed by strong U.S. growth, rising interest rates and escalating trade tensions. In July, Trump blasted China and the European Union for manipulating their currencies, something he reiterated this week, according to Reuters.

The Bloomberg dollar index, which measures the U.S. currency against a basket of peers, has declined about 0.8 percent this week amid Trump’s latest comments. The yield curve, as measured by the gap between 2-year and 10-year yields, on Wednesday flattened to 21.9 basis points, a level unseen since 2007.

“If the Fed signaled a pause and the economy and markets were still in good shape, then almost by definition that would be very good for risk and negative for the dollar,” said Paul Lambert, London-based head of currencies at Insight Investment. “The yield curve would get steeper as you’d be pricing out some of the tightening. And if further down the road inflation does start to emerge, or the markets begin to price in the economy overheating and the Fed losing its credibility, that would be another matter.”

Trump just last week touted on Twitter how inflation was low in the U.S. and business optimism was higher than ever. And despite having previously indicated concern about the strength of America’s currency, he also took the opportunity to laud the “cherished” dollar. While he has amped up tensions with countries around the world on trade, any success in pressuring the Fed might actually help some developing nations.

Emerging Relief

“Emerging markets would obviously take it very positively if the Fed were to voice some concerns on the U.S. or world economic outlook that would lead to a revision of expectations of future rate hikes,” said Delphine Arrighi, a portfolio manager at Old Mutual Global Investors in London.

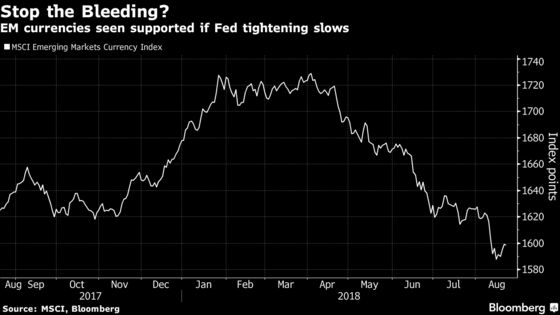

The past weeks have been chaotic for emerging markets as Turkey’s turmoil and sanctions against Russia soured investors’ mood with riskier assets, taking both emerging-market stocks and currencies near their lowest levels in more than a year. The MSCI Emerging Markets Currency index is down 1.7 percent so far in August, headed for its fifth consecutive month of losses, while a gauge of developing-economy stocks has fallen around 3.6 percent, resuming its decline after a brief recovery in July.

Of course, rather than persuading Powell, Trump’s attacks may well embolden the central bank chief to keep plowing ahead as planned with tightening.

“If the board would like to change their mind now after Trump’s comments, they will have to work hard to base their decision on new available data to justify the modification,” said Per Hammarlund, chief emerging-market strategist at SEB in Stockholm.

Keeping Up Appearances

The Federal Reserve will be so keen to avoid the appearance of yielding to White House complaints that it’s likely to further ensure that policy isn’t changed, Joachim Fels, global economic adviser at Pacific Investment Management Co., wrote in a note last month. He expects that will help widen the rate differentials between the U.S. and other developed economies and give a boost to the greenback. That’s so long as the yield curve doesn’t invert, Fels added, as several Fed officials have said they don’t want to see it flip.

Raphael Bostic, head of the Atlanta Fed, said on Monday that prospects for an inversion in the Treasury yield curve, which is viewed by some as a signal of a possible recession, would prompt him to dissent against further interest-rate hikes.

Upending Norms

Still, Trump’s attacks on the central bank do make the Fed’s job harder, and risk spurring more volatility in markets. Bank of America Corp.’s MOVE Index, which tracks the outlook for yield swings implied by Treasury options, has risen to about 50 basis points from around 45 just over a month ago, although it remains below its year-to-date average of 54 basis points.

Low inflation has helped keep yield swings in check and has justified the Fed’s already cautious approach toward increasing rates. Yet, Trump’s upending of presidential norms has certainly muddied waters for the central bank.

Any move by Powell that would be interpreted as ceding to Trump, would undermine the idea of Fed independence, according to Neil MacKinnon, London-based global macro strategist at VTB Capital and a former U.K. Treasury official. “The Treasury market would read it on the part of the Fed as adding to inflation pressures.”

--With assistance from Ben Bartenstein.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Rita Nazareth at rnazareth@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.