Fed's Rate-Hike Path Under Powell Is in Focus With Minutes Today

The last published record of internal deliberations at the Federal Reserve ended on a cliffhanger.

(Bloomberg) -- The last published record of internal deliberations at the Federal Reserve ended on a cliffhanger. An update this week may illuminate U.S. central bankers’ thinking on what is becoming an increasingly controversial topic: the outlook for interest rates next year.

That conversation, along with any hints about how they are judging progress as they unwind part of the Fed’s $4.2 trillion balance sheet, will be the main focus for investors when minutes of the policy-setting Federal Open Market Committee’s July 31-Aug. 1 meeting are released Wednesday at 2 p.m. in Washington. Chairman Jerome Powell may provide more color when he speaks Friday at the Kansas City Fed’s annual gathering in Jackson Hole, Wyoming.

Minutes of the FOMC’s previous meeting, published in early July, revealed that committee participants in June “offered their views about how much additional policy firming would likely be required,” but the account didn’t provide a summary of what those views were.

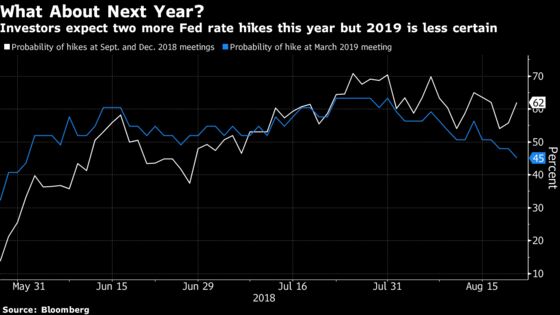

The benchmark federal funds rate is currently fluctuating in a range between 1.75 percent and 2 percent, and investors expect the FOMC to authorize two more quarter-point increases before the year is out, according to futures contracts.

Such a path would put the committee on track to reach a “neutral” level for rates -- the theoretical level which would neither stimulate nor restrict growth -- sometime next year. Most on the FOMC believe that level is somewhere between 2.5 percent and 3 percent, according to estimates published in June.

The question hinted at toward the end of the June meeting minutes is what to do once the committee gets to neutral. Does it keep raising rates in order to preempt inflation, or does it stop there, while taking comfort in signs that inflationary pressures are contained?

So far, the interest-rate projections suggest the FOMC is leaning toward the first option. The median estimate in June was for rates of 3 percent to 3.25 percent by the end of 2019, and between 3.25 percent and 3.5 percent the following year.

Those projections reflect policy makers’ expectations that unemployment, currently at 3.9 percent, will stay below their estimate of the so-called “natural rate” of unemployment that would keep inflation stable, which in June they believed to be at 4.5 percent.

But some Fed officials have been critical of the plan, and Powell has not revealed which way he is leaning -- though he said during congressional testimony in July that “for now,” gradual rate hikes continued to be appropriate.

Political Interference

President Donald Trump is also complicating matters. He reportedly told Republican donors at an Aug. 17 fundraiser that he did not appreciate rate hikes, building on comments he offered last month.

The debate about what to do with interest rates next year “will definitely be part of the conversation” in the minutes, but references to Trump probably won’t be, said Tom Porcelli, chief U.S. economist at RBC Capital Markets in New York.

“What the president wants in this instance is directly contrary to what is the governing principle for the Fed, and so I think the Fed will be true to its foundational elements,” Porcelli said. “The Fed is supposed to raise rates north of neutral if economic activity is accelerating and they are worried about the potential for overheating. That’s the job.”

June’s minutes also said a few officials advocated a more in-depth conversation “before too long” about the game plan for the Fed’s balance sheet, which they began unwinding earlier this year. That may not have taken place at the last meeting, but the minutes could preview how that discussion will go.

Fed officials say they still don’t know how far they will be able to shrink the balance sheet. It ballooned to $4.5 trillion after years of bond purchases in the wake of the financial crisis, which created a pile of cash reserves held by banks on deposit at the Fed.

But policy makers are watching the federal funds rate for clues -- as reserves become increasingly scarce it should rise -- and the recent upward drift of the rate within the quarter-point target range the FOMC sets for it has some analysts predicting there may not be much further to go.

“That’s a big shift,” said Blake Gwinn, a strategist at NatWest Markets in Stamford, Connecticut, who previously worked at the New York Fed. “At some point they are going to have to come out and talk about this, and sooner probably is better than later.”

To contact the reporter on this story: Matthew Boesler in New York at mboesler1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.