BOJ Threat to Global Bonds Fizzles as Japan Lifers Stay Put

BOJ's Threat to Global Bonds Fizzles as Japan Insurers Stay Put

(Bloomberg) -- For all the frenzy over the Bank of Japan’s first policy tweak in almost two years, little seems to have changed for the nation’s life insurers.

That’s because the rise in long-end government bond yields seen after the central bank’s July 31 decision has proved to be fleeting, giving no incentive to the likes of Meiji Yasuda Life Insurance Co., Nippon Life Insurance Co. and Fukoku Mutual Life Insurance Co. to bring home some of the funds locked overseas.

Global markets have been riveted by how high yields on Japanese bonds may climb after Governor Haruhiko Kuroda doubled the trading range allowed for the benchmark 10-year yield. Insurers are clearly signaling that a tidal change in the Asian nation’s money flow won’t come until the central bank lowers purchases of super-long debt.

“There are more things that the BOJ could do before changing the 10-year yield,” Motohiko Sato, general manager for investment planning and research at Meiji Yasuda, said in an interview in Tokyo. “It would be helpful if super-long bond purchases are reduced further.”

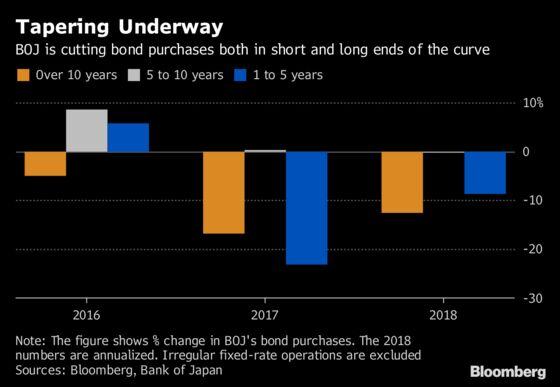

The BOJ on its part has been tapering its debt purchases at a moderate pace amid criticism that its operations have distorted the market. It has trimmed buying of bonds maturing in more than 10 years at an annualized pace of 13 percent this year, after slashing it by 17 percent in 2017, according to Bloomberg calculations.

However, that isn’t enough for life insurers, given how the BOJ stuck to its target of expanding bond holdings by 80 trillion yen ($725 billion) annually at its end-July policy decision, and gave no indication of further cuts in super-long JGBs.

The BOJ maintained purchases of securities in the five-to-10 and 10-to-25 year maturity zones and also those due in more than 25 years at its regular operation on Wednesday.

The 30-year yield is now just two basis points higher than its close on July 30, the day before the BOJ announced its rate decision. Insurers watch this tenor closely to match their long-term liabilities, making BOJ’s actions at the longer-end of the curve more relevant for them than what it does at the short end. Japanese investors have about $2.4 trillion invested in overseas debt.

No Promise

At 0.845 percent on Wednesday, the 30-year yield has climbed from the 0.665 percent level seen in early July, which was its lowest since December 2016. However, it is still below the more than 1 percent level that Nippon Life -- Japan’s largest private life insurer -- said in April was needed to make it easier for it to buy these bonds as against investing overseas.

"We are glad to see some gains in bond yields, but there isn’t any promise for a full-fledged rise,” Toshinori Kurisu, deputy general manager at Nippon Life’s finance and investment planning department, said in an interview. While the 20-year and 30-year yields have climbed, the “yield curve could have been steeper if super-long bond purchases had been cut further.”

The 1-percent level on 30-year debt hasn’t been seen since January 2016, when the BOJ introduced negative interest-rate policy to boost stimulus.

Why Not Stop?

The BOJ should allow longer-maturity yields to rise as insurers will be there to buy once they reach attractive levels, Takehiko Watabe, executive officer at Fukoku, said in a recent interview.

Meiji’s Sato points to the BOJ’s own admission back in September 2016 -- when it first introduced yield-curve control -- that declines in super-long yields have smaller impact on monetary easing compared with changes in the short-end.

“My question is why doesn’t the BOJ stop buying in the long-end if it knows that it won’t have much policy effect?" Sato said. Asked about Meiji Yasuda’s investment plans, Sato pivoted to talk about the company’s decision to buy U.S. mortgage bonds in the last quarter.

Contrasting them with JGBs, yields on U.S. securities are high enough to be attractive, he said.

--With assistance from Masaki Kondo.

To contact the reporters on this story: Chikafumi Hodo in Tokyo at chodo@bloomberg.net;Komaki Ito in Tokyo at kito@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Hiroyuki Nakagawa at hnakagawa11@bloomberg.net, Shikhar Balwani

©2018 Bloomberg L.P.