Chinese Property Developers Tap Onshore Bonds at the Cheapest Price Tag Ever

Chinese Property Developers Tap Onshore Bonds at the Cheapest Price Tag Ever

(Bloomberg) -- China’s property developers are selling more bonds in the domestic market -- and at the cheapest rates, helping to ease refinancing pressures at the cash-strapped sector.

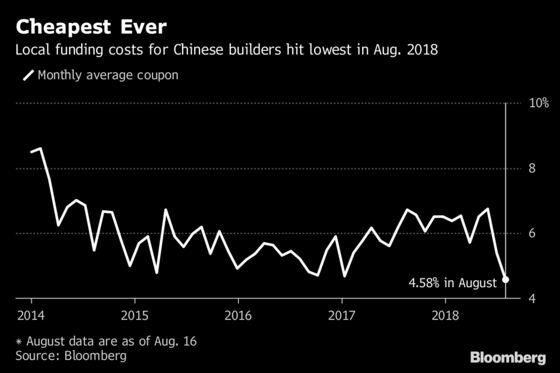

Builders managed to issue 42 billion yuan ($6 billion) of local notes in July, the most in three months, Bloomberg-compiled data show. August is also off to a strong start, with 25.9 billion yuan of notes sold so far. The average coupon they paid this month fell to a record low of 4.58 percent, more than 2 percentage points lower than levels just two months ago, the data show.

It’s a turnaround from almost two years ago when the country’s developers struggled to access the local debt market as Beijing attempted to curb home prices. While the stance hasn’t yet changed, China’s recent measures to ease funding for smaller companies have bolstered investor confidence, thereby attracting demand for their debt.

“Fear of mass defaults in the onshore market seem to have subsided,” said Fredric Teng, head of high yield product group at debt capital market for Greater China and North Asia at Standard Chartered Plc. “With abundant liquidity in the onshore market, names with approval to issue can take advantage of this and issue with a lower coupon.”

CIFI Holdings Group Co. was able to sell 2.5 billion yuan of three-year bonds last week at a coupon of 5.46 percent, lower than the 6.8 percent rate it paid on a local deal sold in March. The level is also more than 1 percentage point lower than the one on CIFI’s three-year dollar debenture sold in April.

Greentown Real Estate Group Co. issued 1.65 billion yuan of five-year notes at 4.73 percent last Friday, lower than its securities sold in May at 6 percent. Other builders that have issued local bonds this month include Sino-Ocean Land Ltd., Gemdale Corp. and China Vanke Co., Bloomberg-compiled data show.

The fact that more property developers are able to tap the onshore bond market recently indicates a loosening of control over their bond issuance approval, said Liu Yuan, a Shanghai-based senior researcher at Centaline Group.

To be sure, the domestic market probably won’t open up to all property issuers and only the larger players are more likely to get regulatory approvals, market participants say.

“So far it’s only the big guys who are getting approved, we haven’t seen the smaller guys getting approved for onshore bonds,” said Ivy Thung, head of credit research at Nikko Asset Management Asia Ltd. in Singapore. “The government has also definitely learned their lessons from 2015 where they opened up the onshore market and gave quotas to everybody.”

The easier access to the local funding market is coming at a critical time as builders have to repay a record amount of debt in the coming months. Combined bond maturities in onshore and offshore markets for the sector amount to $76.5 billion through the end of 2019, according to data compiled by Bloomberg. Builders are expected to tap both markets to meet the refinancing needs.

"We expect onshore issuance will remain strong after a pick-up in recent months," said Franco Leung, property analyst at Moody’s Investors Service. "Offshore issuance slowed recently, but we expect issuers will continue to tap the offshore bond market given the maturity walls in the coming 6 to 12 months.”

--With assistance from Gregor Stuart Hunter.

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net;Narae Kim in Hong Kong at nkim132@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Lianting Tu, Chan Tien Hin

©2018 Bloomberg L.P.

With assistance from Editorial Board