Sanctions Risk May Prompt First Russian Rate Hike Since 2014

Sanctions Risk May Prompt First Russian Rate Hike Since 2014

(Bloomberg) -- Russia’s central bank, one of a handful in Europe to cut interest rates this year, could increasingly consider a hike after the ruble slumped following the latest U.S. sanctions and the risk of more to come.

The currency’s worst week since the 2015 oil crash and the price pressures it threatens to unleash are adding to the Bank of Russia’s long worry list after it already delayed plans to shift to a looser stance this year. With Governor Elvira Nabiullina previously indicating that all options will be on the table in case of “a sharp strengthening in pro-inflationary risks,” an increase in borrowing costs may be in play in the months ahead, according to economists including Credit Suisse Group AG’s Alexey Pogorelov.

Only months after it stepped off the fast track to monetary easing with a pause at three consecutive meetings, the prospect of a hike underscores a change wrought in recent weeks by the fallout from U.S. sanctions and tremors rattling emerging markets from Turkey to Argentina. With inflation already on the rise, a weaker ruble could tip the balance by adding to risks that range from expectations for a weak harvest to an increase in value-added tax in 2019.

“The Bank of Russia can easily return the option of a rate hike, given the combination of factors of a weak ruble, an increase in inflation expectations and the VAT increase,” Pogorelov said.

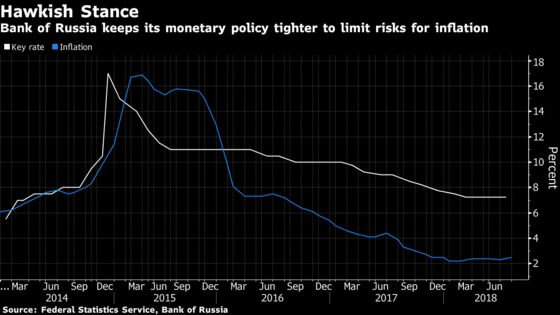

Russia’s currency has come under heavy selling pressure amid tensions with the U.S., compounded by contagion from the crisis in Turkey. Ruble weakness after the last round of American penalties in April already forced the central bank to halt its monetary easing, with its benchmark remaining at 7.25 percent since then.

Last week, the ruble suffered an even bigger decline, retreating more than 6 percent before recouping some losses on Tuesday. It traded 0.8 percent weaker at 66.9 versus the dollar in Moscow on Wednesday.

Even before the latest bout of depreciation, the central bank was warning that inflation may temporarily overshoot its target of 4 percent. It predicts that price growth will speed up to 3.5 percent to 4 percent by year-end from 2.5 percent in July as a result of the government’s plan to raise the VAT rate to 20 percent from 18 percent.

Only a step separates Russian borrowing costs from a level deemed “neutral” - which the central bank previously described as a nominal key rate of 6 percent to 7 percent -- when monetary policy doesn’t contribute to a slowdown or acceleration of inflation relative to the target. The bank’s latest guidance is that that it’s “highly likely” to reach a neutral stance in 2019, a year later than planned.

Policy makers have three rate decisions remaining this year, starting with a meeting on Sept. 14. A Bloomberg survey conducted in late July found that most economists see the benchmark unchanged through the rest of the year before easing resumes in 2019.

RUSSIA INSIGHT: Novichok to Sanctions Shock, Watch the Ruble

At the present exchange rate, the ruble’s losses will contribute about half a percentage point to inflation, Finance Minister Anton Siluanov said in an interview broadcast on state television late on Sunday. The central bank has estimated that each 10 percent decline in the currency’s value could add a percentage point to price growth.

What’s harder to assess is the impact on inflation expectations, which policy makers call a “pillar” of their rate decisions. Following the VAT announcement, the outlook for price growth among households for a year ahead has surged to 9.7 percent in July from 7.8 percent in April.

If the tax increase and the ruble’s depreciation lead to a “stable increase in inflation expectations and a decline in the ability to keep inflation near the target of 4 percent,” then the option of raising the key rate may return to the central bank’s “broad menu of possible decisions,” according to Dmitry Polevoy, chief economist at the Russian Direct Investment Fund. “It’s also possible if risks for financial stability intensify,” he said.

RUSSIA REACT: Soft Inflation Liftoff, But Watch the Ascent

One argument against moving to raise borrowing costs is that the Bank of Russia’s benchmark adjusted for inflation remains among Europe’s largest. The high level of real rates “leaves the central bank some room,” according to Michail Poddubsky, an analyst at Promsvyazbank PJSC.

But even those who see rates staying unchanged warn that a hike may now be a bigger risk.

“The Russian central bank’s stance will depend crucially on the move in inflation expectations,” Deutsche Bank AG analysts including Peter Sidorov said in a report. “The risks are now tilted towards a rate hike for the next three to six months, but we are maintaining our baseline call of rates on hold, followed by a rate cut towards mid-2019.”

To contact the reporter on this story: Olga Tanas in Moscow at otanas@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, Paul Abelsky, Tony Halpin

©2018 Bloomberg L.P.