Fed May End Taper This Year Amid Regime Rethink, Pozsar Says

America’s growing debt pile may force the Federal Reserve to stop shrinking its balance sheet before the year is out.

(Bloomberg) -- America’s growing debt pile may force the Federal Reserve to stop shrinking its balance sheet before the year is out, according to Credit Suisse Group AG analyst Zoltan Pozsar.

With bank reserves at the Fed being pared, the U.S. central bank will soon have to make a choice between activating an overnight facility for repurchase agreements or halting its balance-sheet reduction earlier than many market participants expect, the former U.S. Treasury adviser wrote in a note Monday.

He indicates that policy makers are unlikely to pursue the option of a new facility until alternatives have been exhausted, meaning a premature end to the taper is the most likely outcome. Royal Bank of Canada analysts said last month the balance-sheet runoff could end as early as 2019, while Goldman Sachs strategists in May said they’re assuming an end around April 2020.

A dilemma facing the Fed at the moment is how to keep the overnight fed funds rate, the benchmark it uses to control monetary policy, within its target band as it tries to normalize policy. Its task has been complicated by the Treasury department’s need to finance the growing federal budget deficit and a deluge of bill issuance that’s helped push higher a whole swath of short-term funding rates, including the effective fed funds rate. The situation is spurring a debate among market observers about what potential changes the Fed might need to make to maintain effective control of monetary policy.

Adapting the Toolkit

“A rethink of the Fed’s operating regime will be necessary,” Pozsar wrote. “We are transitioning from an environment where reserves are excess to an environment where collateral is excess. The Fed’s monetary toolkit has to adapt.”

So far, the Fed’s response to the upward drift in the effective fed funds rate has been to lower its interest on excess reserves rate, or IOER, relative to the upper bound of its target range. But Pozsar says reductions in this rate won’t push overnight rates lower and there are “more effective and less disruptive ways of dealing with the glut of bills.”

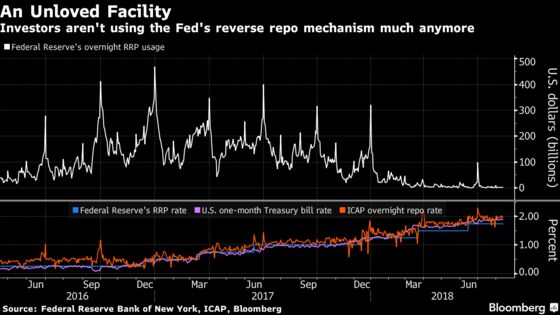

The flood of bills has created an excess of collateral in the repo market and given the constraints imposed by post-crisis regulation, Pozsar argues that bank reserves aren’t overly abundant and thus there isn’t a lot of room for the Fed to shrink its balance sheet. The lack of use of the Fed’s overnight reverse repurchase facility “tells us that every penny of reserves is bid and that balance sheet taper from here will cut right into the system’s liquidity bone.”

Of course there are other options to tame short-end rates. The Treasury could change its issuance strategy toward selling more notes rather than bills, or the Fed could announce a “reverse twist” in which the central bank sells coupon-bearing securities from its portfolio and buys bills instead, Pozsar said. Or the Fed could cut the rate on its foreign reverse repo facility, a program the central bank uncapped when there was a shortage of bills due to regulatory changes.

An overnight repo facility is “useful when collateral is in excess supply and reserves need to be added,” Pozsar said. This could exist in tandem with the overnight reverse repo program, which has been used to mop up excess reserves, as conditions could shift again in the future. But until all alternatives have been exhausted and benefits are clear, the central bank is unlikely to launch a new mechanism, in Pozsar’s view.

“If reserves are hard to add, they’ll have to be preserved by ending taper sooner than many market participants expect.”

--With assistance from Liz Capo McCormick.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.