FAANG Lovefest Rolls On, But Who Timed It Right?: Taking Stock

FAANG Lovefest Rolls On, But Who Timed It Right?: Taking Stock

(Bloomberg) -- S&P futures are retracing most of Monday’s losses as a relative sense of calm was restored among Turkish financial assets (lira appreciated ~5% against the dollar, Borsa Istanbul 100 index +1.3%) while the Europe and China stock markets traded in unspectacular fashion.

Interesting must-know moves, or non-moves if going by the first entry here, include:

- Tesla initially higher after Musk goes to Twitter again, this time to promote that he’s working with Goldman Sachs and Silver Lake on the go-private proposal; the stock is now back to the flat-line, perhaps thanks to a Reuters source noting that Silver Lake was offering assistance to Musk without compensation and wasn’t hired as a financial adviser "in an official capacity"

- Home Depot is up, but well off highs after a beat and raise quarter; Goldman expects an in-line reaction given elevated expectations and the fact that the company guided to a notable second-half deceleration against tougher storm-driven comps

- Switch Inc., a ~$3.3 billion market cap data center REIT whose shares are heavily owned by hedge funds (nearly one-fifth of outstanding), is tanking ~25% in the pre-market after a revenue forecast cut and three sell-side downgrades

- Chinese ADRs are getting whacked every which way after a slew of earnings: Live-streaming companies YY and HUYA are both sliding more than 9% while e-commerce name Vipshop is almost down by the same amount; note that ~$50 billion market cap hedge fund hotel JD.com reports Thursday

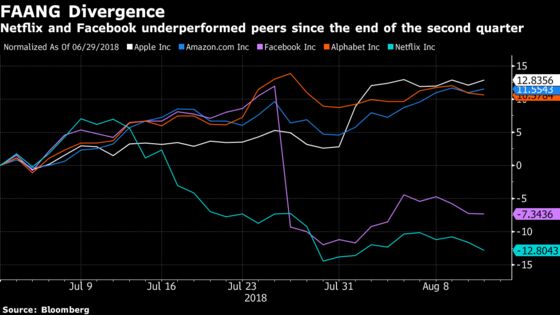

FAANG Lovefest Continues

BofAML’s fund manager survey for August is out, and it’s pretty clear that investors are loving the U.S. lately (allocation to U.S. stocks up 10ppt to net 19% overweight, the largest percentage since Jan. 2015, and first time in five years it gets designated as most favorable region) and still loving tech ("Long FAANG+BAT" trade remains most crowded for seventh straight month and most crowded outright since "Long USD" in Dec. 2015).

"August rotation shows survey participants are buying banks and continue to flock to perceived safe havens like US equities and cash; they are selling commodity sectors and defensive sectors/regions like materials, energy and UK equities," according to the note; in fact, allocation to U.K. equities fell 10ppt to net 28% underweight, it’s largest one-month drop since May 2016 on rising concerns of a "no deal" Brexit.

Happy 13F Day!

Today is the deadline for money managers who oversee more than $100 million in the U.S. to disclose their positions at the end of the second quarter (and notably what they added, exited, boosted, or reduced) in a Form 13F.

Some have already released their filings, for example Third Point and Baupost, but plenty more will hit throughout the day followed by an avalanche after the bell. We’ll be hosting a TOPLive starting at 3:30pm to talk 13Fs as they cross the wire (click here for the event page) and we’ll also publish a wrap of stake changes from the biggest hedge funds and activists tonight once we’ve dissected a giant chunk of the position shifts (click here to see last quarter’s rundown).

Things I’m looking for this go-around include which funds did what with the FAANGs (e.g. bought into Facebook after the Cambridge Analytical scandal only to get knee-capped by the earnings disappointment, got big in Apple before it smashed the $1 trillion milestone, kept riding Amazon as it notched a new record seemingly every day), who held Tesla prior to the "funding secured" melodrama, and who got caught up in NXP Semi before the collapse of the $44 billion Qualcomm deal.

And, as always, we’ll scour the filings to detect who the new "hedge fund hotels" are that fast money has piled into of late -- like Camping World Holdings, which bounced as much as 5.9% yesterday after Third Point reported a whopping new stake (see a breakdown of this in Monday’s Taking Stock) to become the second-largest holder in the name.

Also of interest are those stocks that have heavy hedge fund ownership and showcased large swings since the end of the second quarter, such as:

- TMT: Alteryx +44%, Intelsat +37%, Roku +30, GrubHub +24%, Yelp +20%, Sinclair Broadcast -13%, Shutterfly -18%, Twitter -25%, Diebold Nixdorf -62%

- Health care: Mallinckrodt +70%, Endo International +61%, Iqvia +21%

- Consumer: Carvana +29%, Hertz +26%, New York Times -12%, Sotheby’s -15%, Mohawk Industries -15%, Papa John’s -18%, Newell Brands -21%, Weight Watchers -25%, Scientific Games -35%

- Industrials & Materials: Arconic +20%, Tronox -24%

Notes From the Sell Side

Goldman is positive on Deere ahead of Friday earnings after a meeting with the president of a major U.S. ag machinery dealer, which revealed an outlook for modest improvement in Deere’s early order program and a further tightening of used equipment inventories, which is the analyst’s favorite lead indicator.

Morgan Stanley boosts its price target on overweight-rated Salesforce.com to a Street-high $178 on optimism over the Mulesoft integration: "Unlocking data trapped in legacy systems via MuleSoft brings SFDC to the forefront of driving digital transformation for its customers. Consensus expectations likely underestimate this growth potential and SFDC’s improved M&A track record."

JPMorgan rebalances ratings in the payments sector, upgrading Alliance Data to an overweight as sentiment nears an inflection point (delinquency trends stabilize, expanded buyback and potential for divestitures provide support) and downgrading both Fiserv and Paychex to an underweight ("below-average growers with below-average earnings upside risk").

Deutsche Bank slashes insurer Chubb to a sell with a Street-low price target $126: "We believe that the past several quarters have shown post-merger Chubb to be unable to grow its business at levels in-line with the peers group." Meanwhile, BTIG downgrades On Deck Capital to sell (only its second sell rating out of 13 total analysts covering the stock) on uncertain growth prospects and overextended valuation.

Lastly, there are a couple takes on Elliott’s activist stake in Nielsen. 1) Macquarie sees potential for a "rapid sale process" to ensue with private equity leading the way and estimating a breakup value of $26 to $47, which compares to Monday’s close at $24.62, and 2) Morgan Stanley sees shares rising ~20% on a sale of the entire business, noting that strategic buyers could include WPP plc and Ipsos, or potentially plunging ~23% if the company fails to sell itself.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- Deadline for 13-F fund filings for the second quarter

- 7:00am -- EAT earnings

- 7:30am -- CDK earnings

- 8:00am -- GDS earnings call

- 8:30am -- Import/Export Price Index

- 8:30am -- TPR, CHRA earnings calls

- 9:00am -- HD earnings call

- 9:45am -- IBM at Keybank Technology Leadership Forum

- 10:30am -- LRCX, CTXS at Keybank Technology Leadership Forum

- 11:00am -- New York Fed releases 2Q Household Debt and Credit Report

- 12:00pm -- CWH investor open house

- 2:05pm -- TXN at Keybank Technology Leadership Forum

- 3:00pm -- Ethereum co-founder Joseph Lubin on Bloomberg TV

- 4:01pm -- CREE, VIAV earnings

- 4:05pm -- A, MYGN, WYY earnings

- 4:30pm -- API oil inventories

- 5:00pm -- HOLI earnings

- 9:30pm -- China New Home Prices

- 10:00pm -- Tencent earnings (roughly)

- Tonight -- Congressional primary elections in Minn., Conn., Vt., and Wis.

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.