Standing Pat, Central Bank Says Rand Drop Is Blip Due to Turkey

South Africa Is No Turkey: It's Not Going to Prop Up the Rand

(Bloomberg) -- A jump in South Africa’s interest-rate bets may be little more than a reflection of the turmoil in Turkey.

Forward-rate agreements, used to speculate on interest rates, increased on Monday after the rand sagged -- at one point dropping the most since the 2008 financial crisis -- as Turkey’s crisis sapped demand for emerging-market assets.

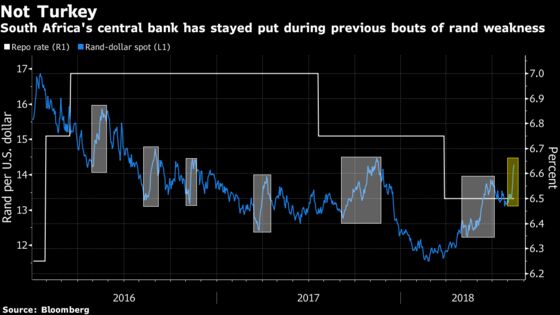

But the South African Reserve Bank has ignored bouts of rand weakness in the past, holding or even cutting its policy rate as it focused on its inflation-targeting mandate without government interference. That’s in contrast to Turkey, where the central bank’s credibility is in question at a time when investors are pleading for dramatic action to prop up the lira.

“The rand’s weakness will be inflationary, but it is unlikely to force the Reserve Bank to hike,” John Cairns and Kim Silberman, analysts at Rand Merchant Bank in Johannesburg, said in a client note. “Unlike the Central Bank of Turkey, the Reserve Bank has hard-won credibility, which limits the extent to which sell-offs in the currency are sustained -- unless they are fundamentally driven.”

Pass-through from currency weakness into South African consumer prices has weakened in recent years, a study by economists from the World Bank and International Monetary Fund has shown, making it even less likely that the central bank will raise interest rates any time soon. The consumer-inflation rate has been inside the target range for more than a year, and is forecast to remain there through 2020.

The South African Reserve Bank won’t intervene to prop up the rand unless the orderly functioning of markets is threatened, Deputy Governor Daniel Mminele said Monday. The rand’s drop was “an overshoot” due to contagion from Turkey’s crisis, he said.

‘Market Forces’

“Our preference is for the exchange rate to be determined by market forces,” Mminele said by phone. “We are clearly watching and monitoring the situation very carefully, but we would not become involved with a view of influencing the exchange rate in a particular direction or wishing to stem the depreciating pressure in a very targeted way. We are not an exchange-rate targeter.”

Forward-rate agreements starting after the next policy meeting on Sept. 20 rose six basis points on Monday to 7.11 percent as traders added bets on a rate increase. Even so, they’re only pricing in 11 basis points of rate increases, or a 44 percent probability of a 25 basis point hike. Contracts kicking in after the last policy meeting of the year in November are pricing in a full 25 basis points.

The currency weakened as much as 9.4 percent in thin trading during Asian hours on Monday before paring the loss to trade 1.6 percent weaker at 14.3248 per dollar by 5:13 p.m. in Johannesburg, bringing its decline in the past four trading sessions to 6.9 percent.

Asian Crisis

Since nothing has changed fundamentally globally or locally to spark the sell-off, the rand will probably retrace its losses, said Cairns and Silberman at Rand Merchant Bank. The currency will probably return to a range between 13 and 14 per dollar for the rest of the year, they said.

The Reserve Bank last actively intervened in the market during and after the Asian crisis in 1997, squandering its foreign reserves and running up large debts in an ultimately unsuccessful attempt to defend the rand.

Since the adoption of the inflation-targeting framework in 2000, the bank has repeatedly said that it doesn’t target a level for the rand and won’t use interest rates to support the currency. It has also built up a war chest of $50.5 billion in foreign-currency and gold reserves.

--With assistance from Colleen Goko.

To contact the reporters on this story: Robert Brand in Cape Town at rbrand9@bloomberg.net;Ntando Thukwana in Johannesburg at nthukwana@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Rene Vollgraaff

©2018 Bloomberg L.P.