The ’80s Are Thriving at Trump’s Fed

To understand the origin of New Keynesian theory, it helps to go back to 1980.

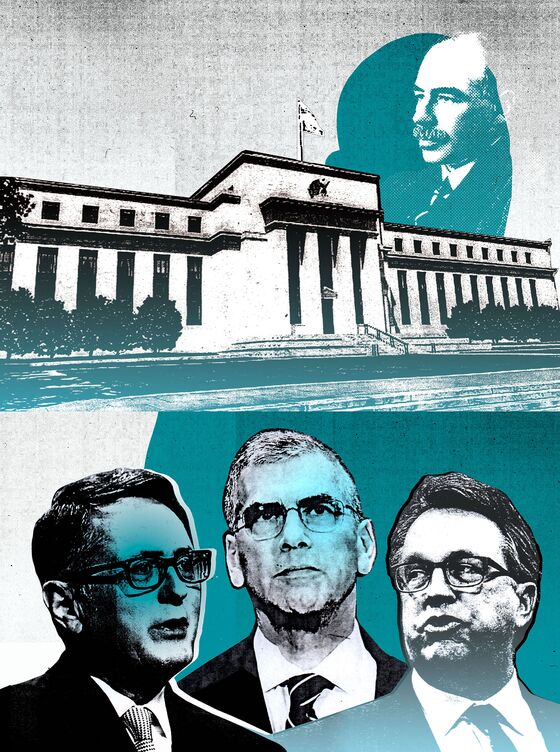

(Bloomberg Markets) -- About 18 months before U.S. President Donald Trump nominated him to the Federal Reserve’s Board of Governors, Marvin Goodfriend told an audience that his own family had been the victim of bad economic policy.

His father had accumulated most of his savings in the 1970s before retiring in 1984, the Carnegie Mellon economics professor recounted at the May 2016 panel discussion in Amelia Island, Fla. The savings dissipated so quickly, Goodfriend said, that his mother wondered if her husband had a secret family on the side.

“He had all his money in government bonds, and the nominal value of government bonds was such that his savings were wiped out by inflation over a decade,” he said. “The reason it’s so hard for savers to get protection is because governments have been irresponsible about either their monetary systems or other things, and I think we need to start there.”

Along with data, calculations, and theory, personal experiences can play a formative role in the worldview of policymakers. For Goodfriend, 67, and others in his generation, the double-digit inflation of the late 1970s and early 1980s—and the Federal Reserve’s war to tame it—had a profound impact on their vision of responsible government.

Goodfriend’s economic philosophy is, in large part, shared by fellow Federal Reserve Board nominee Richard Clarida, 61, Federal Reserve Bank of New York President John Williams, 56, and even Fed Chairman Jerome Powell, 65. One defining ethos of the “Trump Fed” so far may be the conservative, inflation-centric “New Keynesian” economics that Goodfriend, Clarida, and Williams helped formulate.

But not everyone at the central bank is on board with the New Keynesian prescriptions, and the assumption that there is a “natural rate of unemployment” the Fed is unable to affect increasingly is being called into question. Wages and inflation are failing to behave in ways that New Keynesian models would predict. Battle lines are being drawn around a debate that will probably come to a head next year.

In today’s post-financial-crisis world, boosting workers’ pay and tackling inequality seem more relevant than worrying about inflation, which has been mostly low and stable for the past 25 years. Indeed, Goodfriend’s appointment stalled after a rocky Senate Banking Committee hearing in January, in which he struggled to defend some of his past inflation predictions in questioning by Democrats.

To understand the origin of New Keynesian theory, it helps to go back to 1980. That’s the year Goodfriend received his Ph.D. in economics from Brown University and began a 25-year career at the Fed. Ronald Reagan was elected president, ushering in a 12-year run of Republican White House control and a decades-long rise in the share of wealth held by the richest Americans.

Then-Federal Reserve Chairman Paul Volcker was engineering a draconian tightening of monetary policy to tame U.S. inflation that peaked at an annual rate of almost 15 percent. While that policy contributed to two recessions, it also succeeded—eventually—in restoring price stability. An economic recovery followed.

The theory that Goodfriend, Clarida, and Williams developed held that if the central bank can convince the public that it will keep inflation low and stable, those expectations will be largely self-fulfilling. That in turn will stabilize other important aspects of the economy, such as unemployment.

The group was dubbed the “New Keynesians” because, unlike classical economists, they saw a role for central bankers to correct failures that occur in the free markets. The British economist John Maynard Keynes’s early 20th century writings gained enormous influence in the aftermath of the Great Depression. Traditional Keynesians believe that the government can stimulate employment by creating demand for goods and services and sometimes must do so when private-sector demand falls short.

In the eyes of the New Keynesians, traditional Keynesians took the “stimulus” too far in the late 1960s and early 1970s, allowing deficit spending and overly easy monetary policy to fuel the inflation that destroyed the Goodfriend family’s savings. In reaction, New Keynesian theory makes sacrosanct the central bank’s responsibility for controlling inflation, as Volcker did.

Since it was developed in the 1990s, the New Keynesian framework has won widespread acceptance. Clarida’s most influential work, a 1999 paper titled The Science of Monetary Policy: A New Keynesian Perspective, is a common reference in standard economics textbooks. Central banks around the world have adopted the doctrine’s principles.

New Keynesian research “formalized this idea that people sort of knew, but we were precise about it,” says Mark Gertler, a New York University economics professor who co-authored a number of works with Clarida in the 1990s.

Clarida, a Columbia University economics professor who is also a managing director at Pacific Investment Management Co., is poised to win confirmation as the Fed’s vice chairman, filling one of four vacancies on the seven-member Federal Reserve Board. Williams moved this year from the San Francisco Fed, where he was president, to the same role at the New York Fed, gaining a permanent vote on the policy-setting Federal Open Market Committee as a result.

Fed Chairman Powell spent much of his career in private-sector finance roles, except for a stint at the U.S. Department of the Treasury in the early 1990s. As a Fed governor since 2012, he’s become familiar with the New Keynesian philosophy, and his strong support for Clarida and Williams stems in part from his desire for a disciplined policy approach.

The emphasis New Keynesian theory places on communication is creating a challenge as the Fed’s plans have become politically unpopular, attracting criticism even from Trump. Since September 2017 the FOMC has been signaling that because the unemployment rate has dropped so much, the Fed will have to raise interest rates to forestall inflation.

This conclusion stems from a key equation in the New Keynesian model on the relationship between unemployment and inflation. The equation posits that once unemployment falls below a certain hypothetical “natural rate”—a concept originated by the late University of Chicago economist Milton Friedman—prices will begin to rise. Once that happens, the only way for the central bank to control inflation is to clearly signal it will raise interest rates to levels that restrict economic growth until unemployment rises back to its natural rate.

According to projections published in mid-June, FOMC participants’ median estimate of the natural rate of unemployment was 4.5 percent. The actual rate fell below that in early 2017 and was 4 percent as of June 30. As the gap between the two numbers has widened, Fed officials have responded by increasing their estimates for how much they will need to raise interest rates. Most on the committee now predict the federal funds rate needs to be 2.5 percent to 3 percent to keep the economy “neutral.” That will be attained next year at the current pace of rate increases. Then the debate will be: Should rates keep rising to ensure unemployment returns to the “natural” rate and inflation remains contained, or can the Fed stop and see what happens?

New Keynesians believe that, before Volcker, the Fed’s failure to respond aggressively to inflation developments “left the door open for self-fulfilling, destabilizing expectations,” says Peter Ireland, an economics professor at Boston College who worked at the Richmond Fed in the 1990s, when Goodfriend was director of research there. “The Fed wouldn’t do enough to offset those, and as a consequence, actual inflation followed expected inflation up.”

If the expectations of businesses and consumers are as important and as malleable as New Keynesian theory indicates, central banks can—and should—manage them with statements, speeches, projections, and the like. Fed officials have now fully embraced that lesson.

But a younger generation of researchers is reassessing the earlier work. Emi Nakamura, an economics professor at the University of California at Berkeley who received her Ph.D. from Harvard in 2007, has been looking at the empirical evidence and is finding that it differs from some of the New Keynesian model’s assumptions.

In one recent paper, noting that actual unemployment is typically above estimates of the natural rate instead of fluctuating around the estimates, she and her co-authors find that allowing higher inflation may reduce average unemployment. In another, they suggest that some of the costs of higher inflation implied by the original New Keynesian models are overstated.

“We still have this New Keynesian model in our heads,” says Mark Wright, research director at the Minneapolis Fed. “The fact that we’re not maybe seeing it work the way we thought has led us to consider some alternatives.”

Increased attention to unequal wealth distribution is also challenging the conventional wisdom. The share of savings held by the poorest 90 percent of the population fell to 23 percent in 2016, from 33 percent in 1989, according to the latest results of the Fed’s triennial Survey of Consumer Finances, released last year.

As a result, the New Keynesian focus on inflation means protecting a far smaller and wealthier group of savers than it did in the 1970s.

During the summer of 2014, shortly after she became Fed chair, Janet Yellen suggested that tightening labor markets could spur wage growth without increasing inflation. Her argument was that the dramatic shift in income distribution toward shareholders and away from workers over the previous decades left room for workers to recoup some of the share before companies would be forced to raise prices. That meant the Fed wouldn’t have to raise interest rates so quickly to fend off inflation.

Clarida tweaked a government data set to reproduce the labor share of national income, the portion allocated to wages. Paul McCulley, then chief economist at Pimco, dubbed the number “Rich’s Ratio.”

“There is ample room for the Fed to let Rich’s Ratio climb for a long time, before fostering a breach of its inflationary mandate so egregious as to warrant immoderately high long-term interest rates,” McCulley wrote at the time. Since then, Rich’s Ratio hasn’t improved much and inflation remains dormant, leaving Yellen’s idea untested.

Yellen was replaced by Powell in February. In the Fed shaped by Trump, the New Keynesians taking the reins seem, so far, committed to maintaining their inflation-fighting credibility.

If central banks “try to exploit the nonresponsiveness of inflation to low unemployment and push resource utilization significantly and persistently past sustainable levels, the public might begin to question our commitment to low inflation, and expectations could come under upward pressure,” Powell said in a June 20 speech.

But as long as wages and inflation remain low, pressure will grow on the New Keynesians to test their own theory.

Boesler is an economics reporter at Bloomberg in New York.

To contact the editor responsible for this story: Christine Harper at charper@bloomberg.net

©2018 Bloomberg L.P.