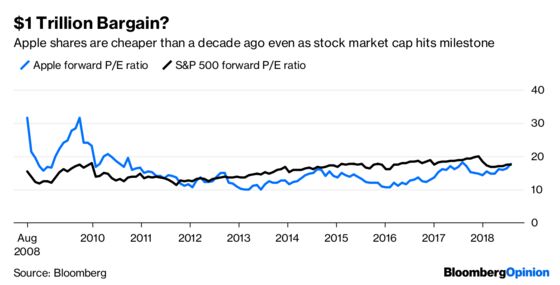

(Bloomberg Opinion) -- Can something worth $1 trillion be cheap? Apple Inc. on Thursday became the first U.S. company to reach the hard-to-conceptualize milestone, which is sure to spark a debate about whether the stock market is just one big bubble waiting to burst. After all, Apple’s market capitalization is bigger than the economies of all but 17 countries in the world.

Plus, Amazon.com Inc., Google parent Alphabet Inc. and Microsoft Corp. are not far behind; all have stock market values that comfortably exceed $800 billion. But as DataTrek Research co-founder Nicholas Colas pointed out in a note to clients, Apple has accomplished this feat in the absence of a sky-high multiple. Its shares trade at about 17.6 times forecasted earnings, compared with 17.5 times for the S&P 500 Index, which is about in line with the average going back to 1990 and far below the peak during that time of more than 25 times in the late 1990s. While it’s true that stocks face a lot of headwinds — the potential for a trade war, a hawkish Federal Reserve, rising federal debt and deficits — valuations are not exactly one of them. Apple’s breakthrough does expose, however, a highly lopsided market for equities.

On one side sits a handful of highflying technology-related shares; everything else is on the other. Bianco Research President Jim Bianco compared it to a zero sum situation in a Bloomberg Opinion commentary last month. He found that Facebook Inc., Apple, Amazon, Netflix Inc., Microsoft and Google — collectively known as the FAANMGs — had pushed the S&P 500 up by 2.66 percent since November, while the other 494 stocks in the benchmark pushed it down by a collective 0.4 percent. Adding Twitter Inc., Tesla Inc., Alibaba Group Holding Ltd., Baidu Inc., Nvidia Corp. and Tencent Holdings Ltd. to the FAANMGs group caused the MSCI World Stock Index to rise by 1.61 percent. Every other stock on the planet was collectively down 1.07 percent.

POUND POUNDED

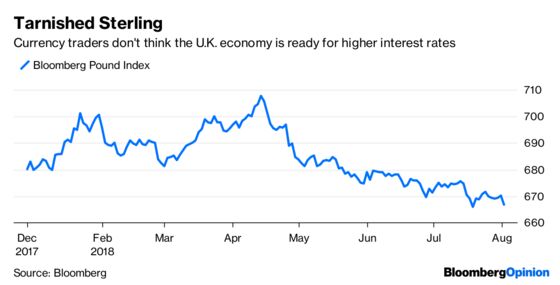

The Bank of England is hastening the demise of the U.K. economy. That’s one conclusion to draw from the sterling’s reaction to the central bank’s decision on Thursday to raise interest rates. The Bloomberg Pound Index slid as much as 0.63 percent, keeping it at its lowest levels since October and bringing its decline since mid-April to 5.76 percent. The move is surprising because 1) higher rates tend to bolster a currency because they attract foreign capital, and 2) the decision by policy makers was unexpectedly unanimous, suggesting another boost may be in the works before long. What’s puzzling to currency traders is why the BOE felt the need to raise rates when the U.K.’s exit from the European Union is still mired in uncertainty. The U.K. economy is expected to grow just 1.3 percent this year, and 1.5 percent in 2019, Bloomberg data show. “Some fairly optimistic assessments in there — but this is all with rose-tinted glasses of a smooth Brexit adjustment,” said Viraj Patel, a strategist at ING Groep NV, according to Bloomberg News. “That is currently not a view that everyone in the market shares — so expect limited follow-through. The short-term political troubles for the pound remain.”

BREWING DEBT CRISIS?

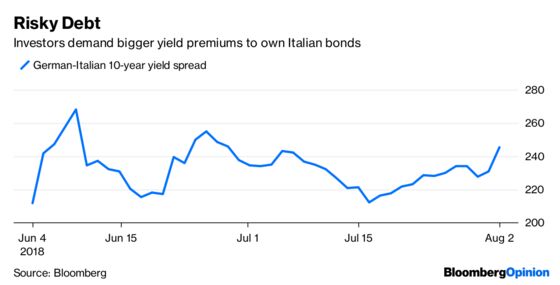

It’s way too soon to say the euro zone faces another debt crisis, but a couple of developments in two bond markets Thursday are causing some concern. First, Italy’s bonds tumbled ahead of a budget meeting between populist political leaders and Financial Minister Giovanni Tria. The meeting is to consider demands by the populists for a flat tax and income support for the poor, Il Sole 24 Ore reported, without saying where it obtained the information. Italy’s finances are already on shaky ground, and any policies that add to its $2.28 trillion debt load are sure to be looked upon unfavorably by bond investors. In a sign that debt investors perceive heightened risks, Italy’s 10-year bonds yield 2.44 percentage points more than German bunds, more than doubling from 1.13 percentage points in April. In France, investors submitted bids for just 1.31 times the amount of 20-year bonds offered by the government, down from 2.14 times at the prior sale of those maturities and marking the lowest so-called bid-to-cover ratio since at least 2007. Some strategists speculated the drop in demand may have been due to Japanese investors, who are big owners of French bonds, choosing to take advantage of suddenly higher yields back home. And how did the currency market react? The Bloomberg Euro Index was headed for its lowest close in almost a month in late trading.

TRADE WAR LOSERS

In the great debate about whether the U.S., China or the European Union will come out ahead as trade war rhetoric heats up, it’s becoming clear that the biggest loser will be emerging markets. The MSCI Emerging Markets Index of equities fell as much as 1.99 percent Thursday at one points in the biggest drop since March, while the broader MSCI All-Country World Index declined just 0.91 percent. The sell-off followed reports that the U.S. is weighing whether to impose a 25 percent duty on $200 billion worth of Chinese goods, up from an initial 10 percent rate, and China responded by saying it’s ready to retaliate. Of course, China is part of the EM index, and plenty of its constituents have their own problems unrelated to trade, such as Turkey and South Africa. The Institute of International Finance in Washington calculates that net capital flows to EM slowed to about $11 billion last quarter from $118 billion in the first three months of the year. Outside of China, EM counties sold more than $8 billion of their foreign-exchange reserves to bolster their currencies, the IIF noted in a report Thursday. India’s central bank governor raised the prospect of global currency wars as he led policy makers in raising interest rates to the highest in two years to shore up the rupee and tackle inflation pressures. “The trade skirmishes evolved into tariff wars and now we are possibly at the beginning of currency wars,” Reserve Bank of India Governor Urjit Patel told reporters.

FOOD PRICES TUMBLE

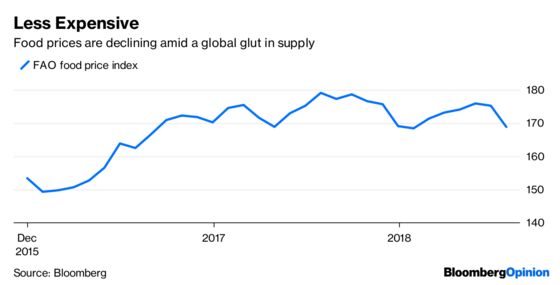

With all the volatility in commodities markets these days stemming from escalating trade tensions, it’s hard to keep track of what’s up, what’s down and what the impact on consumers will be. Although it may not have much to do with global trade, one key part of the commodities market is proving friendly to consumers. Food costs are starting to buckle under the weight of too much supply, with a gauge of global prices slumping by the most this year, according to Bloomberg News’s Nicholas Larkin. The United Nations’ food price index dropped 3.7 percent in July, a month after trade war tensions helped push prices down for the first time since January. Dairy-product and sugar prices fell the most last month amid better production prospects or ample export supplies. Even concern about wheat output on the back of drought in major growers wasn’t enough to stop grain costs from slipping, Larkin reports. Prices fell across all food groups, with vegetable-oil costs hitting a 2 1/2-year low and a gauge of sugar sliding on improving crop outlooks in key producers such as India and Thailand. That’s good news for consumers who’ve faced higher bills in recent years, as well as central bankers trying to curb inflation.

TEA LEAVES

The U.S. Labor Department will release the monthly jobs report on Friday, and it should be average. Not average in a bad way, just that the median estimate among economists surveyed by Bloomberg show some 192,000 jobs were added in July. That’s in line with the monthly average of 213,000 since the economy started recovering in 2010. The real action happens in the part of the report that provides the data on wages. Investors have come to immediately zero in on this data point because of its implications for inflation. The thinking goes that faster wage gains should translate into faster inflation. But despite a low unemployment rate of about 4 percent, wage gains have been muted, stuck in a band of 2.5 percent to 2.8 percent on a year-over-year basis since mid-2016. The July jobs report is likely to be no different, with the year-over-year increase forecast to be 2.7 percent.

DON'T MISS

Bill Gross Is Ahead of the Pack in Losing Money: Brian Chappatta

BOE Brexit Groupthink Risks a Rate-Rise Reversal: Mark Gilbert

End-of-Days Metals Rout Overstates Trade Risks: David Fickling

How Economics Went From Philosophy to Science: Noah Smith

U.S. Consumers Broadly Are About to Feel the Pinch: Conor Sen

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.