The Flat Yield Curve Is Flagging a Strong U.S. Economy

Amidst fears of a repeat of the 2008 global crisis, the U.S economy’s flat yield curve is a sign of strength than failure.

(Bloomberg Opinion) -- Given all the attention it has gotten in recent months, most everyone seems to know that the bond market’s yield curve is dangerously close to inverting, an event that has reliably predicted U.S. recessions in the past. The recent firming of economic growth, however, is a reminder that the shrinking difference between short- and long-term Treasury yields by itself does not indicate economic weakness ahead.

Quite the contrary. The economy tends to grow and stocks advance even as the curve shrinks toward zero. In fact, a yield curve holding at the current levels would suggest a bright outlook for the economy and equities.

The fretting over the yield curve stems from the reality that a flattening must precede inversion; hence the flattening is every bit an indicator of economic weakness as inversions. While this is arguably true, the fact that flattenings precede inversions is not a particularly useful relationship from a forecasting perspective, because of the long and variable lags between flattening and inversion and then inversion and recession.

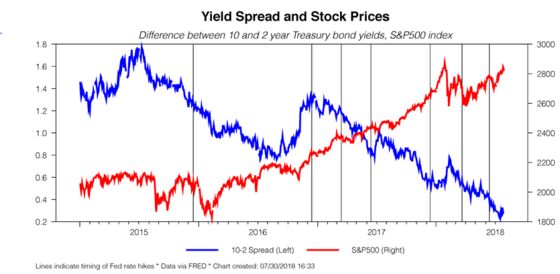

The second-quarter gross domestic product report illustrates this point. The yield curve has been narrowing relentlessly since 2015, with the spread between two- and 10-year Treasury note yields first slipping below 100 basis points in mid-2016 and again a year later. It has subsequently contracted to around 30 basis points.

Despite the decline, the economy grew at a 4.1 percent rate last quarter. Although that number likely overstates the strength of the economy, the year-over-year rate was 2.8 percent, continuing a steady acceleration from 1.3 percent in the second quarter of 2016. Also, the flatter yield curve has not yet undermined the bull market in stocks.

The general economic strength should have been anticipated. As the business cycle moves from an early stage to one that is more mature, the economy moves closer to full employment. That shift toward full employment induces the Federal Reserve to boost policy rates, which flattens the yield curve. A fairly flat yield curve is then consistent with an economy nearing its long-run equilibrium. The current environment of ongoing strong job growth and low unemployment and inflation is an arguably Goldilocks macroeconomic scenario.

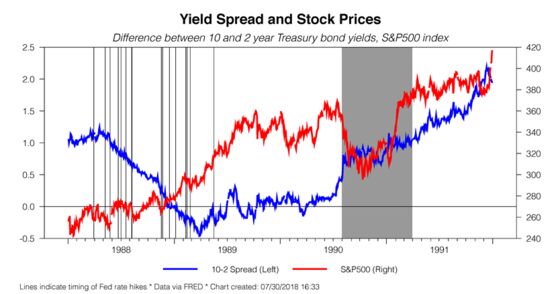

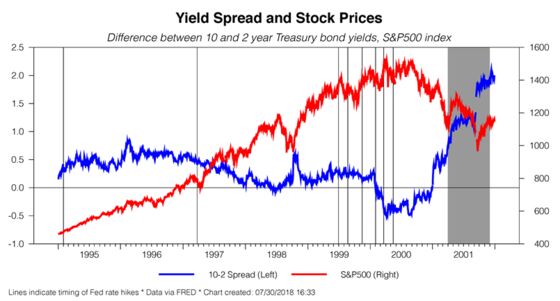

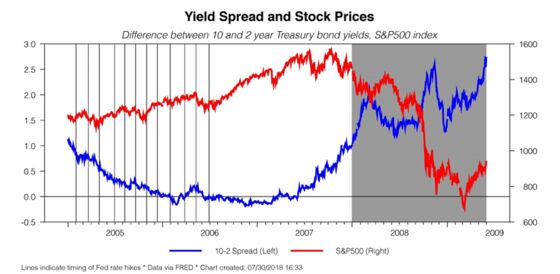

The economy followed a similar pattern in the last three cycles. Even as the yield curve flattened, the economy maintained growth and stocks continued to rise. And the pattern continued even after the yield curve inverted. The inversion is a long leading indicator. In the past, selling equities at the first hint of inversion on the expectation of an impending recession meant foregoing further gains.

What’s the takeaway now? First, the economy might not continue to accelerate and might even moderate, but it isn’t set for a recession. And absent a recession, the general trend for equities is likely to be up.

Second, while the yield curve could invert this year, it may instead remain flat just like in the late 1990s. The recent gains in the long-term yields amid speculation that major central banks will pull further back from their extraordinary bond buying measures supports the hypothesis that term-premiums are set to rise and keep the yield curve from inverting even as the Fed continues to boost short-term rates. Or, the Fed could decide to slow or even put the hiking cycle into an extended pause after it pushes policy rates toward closer to neutral. Either situation would delay an inversion of the yield curve and thus delay any signal that the economy is about to turn the corner.

But the ultimate implication is that the flat yield curve isn’t a sign of economic weakness. It is a sign of economic strength. The thing to fear is when inflationary concerns induce the Fed to invert the yield curve or failure to respond to an inverted curve. That’s when the recessionary signal intensifies. Until then, the flat yield curve is the equivalent of an “all’s clear” signal.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.